China’s Ghost Cities Are a Problem for Europe’s Luxury Brands, Too

Chinese consumers watching the value of their homes fall are losing the confidence to spend on designer goods

3 min

3 min")

How closely is demand for $3,000 handbags tied to home prices in China? Quite closely, it turns out, which is unfortunate for luxury brands.

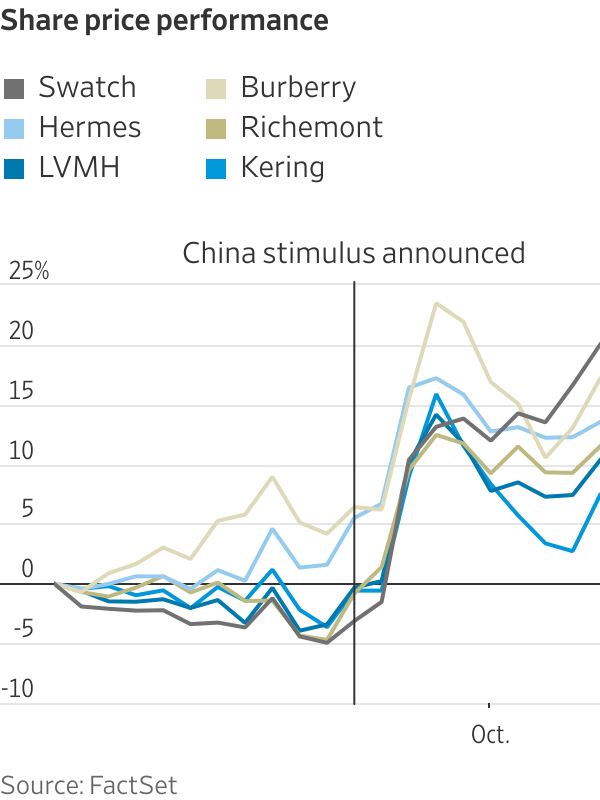

Europe’s luxury stocks fell in early trading Tuesday after China’s economic planning agency failed to announce additional measures to kickstart growth that some investors had hoped for. The sector is still up 10% on average since Beijing launched its initial stimulus plans late last month.

Beijing hopes a cut to mortgage rates, and lower down-payment requirements for buyers of second homes, will jump-start the country’s troubled housing market. A package of loans to brokers and insurers to buy Chinese shares has had initial success at lifting the stock market.

Luxury spending in China has traditionally been more correlated with its home prices than with the financial markets or overall economic growth. Around 60% of net household wealth was tied up in property before prices peaked in 2021. Barclays estimates that falling home prices have destroyed about $18 trillion in household wealth since then, which is equivalent to roughly $60,000 per family.

This, along with worries about the wider economy, is hurting consumer confidence. Retail sales rose just 2.1% in August compared with the same month last year, according to data from China’s National Bureau of Statistics. When global luxury brands start to report their third-quarter results next week, Chinese demand is expected to have slowed since they last updated investors.

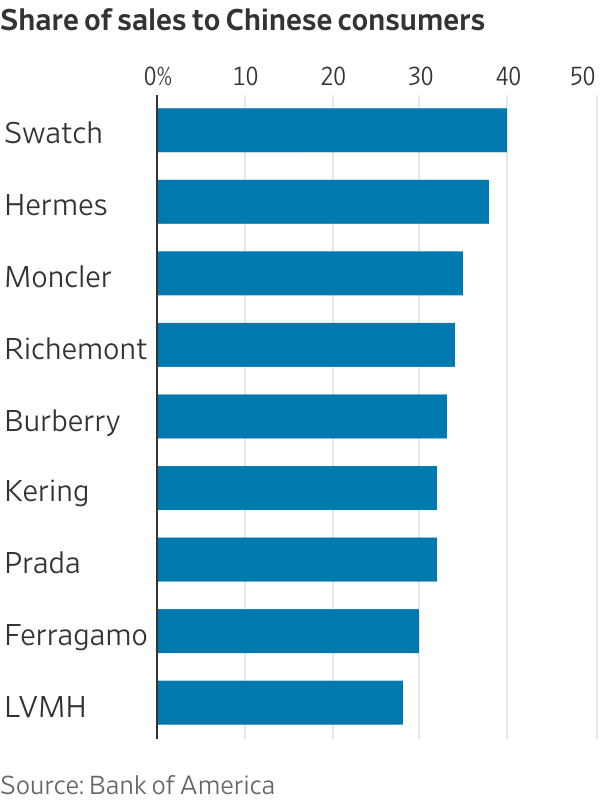

Flagging sales come at an unhelpful time for Europe’s luxury companies, which rely on Chinese consumers for a third of global luxury spending. After several bumpy years during the pandemic, luxury brands and their investors hoped that a comeback in Chinese spending would compensate for a slowdown among Europeans and Americans.

This looks increasingly unlikely. Luxury sales to Chinese shoppers are expected to shrink 7% in 2024 and by 3% next year, according to UBS estimates. As luxury brands have high fixed costs, including the most expensive retail rents in the world, a slowdown with such key customers could have an outsize impact on profit margins.

The last time the luxury industry went through such a rocky patch in China, barring the pandemic, was between 2014 and 2016 when Beijing was cracking down on corruption, including officials who were gifting Louis Vuitton handbags and Rolex watches in exchange for political favours. The global luxury industry barely grew for two years during China’s anticorruption drive, which also coincided with a property-market correction in the country. It didn’t help that shoppers in other markets were also tiring of logos back then.

Europe’s luxury stocks look expensive today compared with that time. As a multiple of expected earnings, listed brands’ shares now trade at a roughly 40% premium to their 2014 to 2016 average.

To justify the higher price tag, Beijing’s housing and wider economic stimulus would need to indirectly lift luxury demand. Measures rolled out so far may not be enough to slow the slide in home prices. China’s housing market is oversupplied by around 60 million units, according to Bloomberg Economics estimates.

New incentives to kick-start consumption are expected soon but will probably target mass-market products like white goods. China already rolled out trade-in subsidies for home appliances earlier this year and a range of consumption coupons.

None of this is very helpful for sellers of expensive luxury goods. For brands to see a recovery, Chinese consumers that spend anywhere from $7,000 to $43,000 a year on luxury products would need to feel much better about their finances than they currently do. Spending by this group has fallen 17% so far this year compared with the same period of 2023, according to a report by Boston Consulting Group.

Half-finished, abandoned housing estates are a big headache for China’s government, and are also on the mind of executives in Paris and Milan. Though the fortunes of luxury bosses likely isn’t high on Chinese officials’ priority list, their fates may be intertwined.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

From warmer neutrals to tactile finishes, Australian homes are moving away from stark minimalism and towards spaces that feel more human.

A cluster of century-old warehouses beneath the Harbour Bridge has been transformed into a modern workplace hub, now home to more than 100 businesses.