The New Math on Inheriting Your Parents’ House

Rising costs are prompting more adult children to sell the homes they inherit from their parents

3 min

3 min

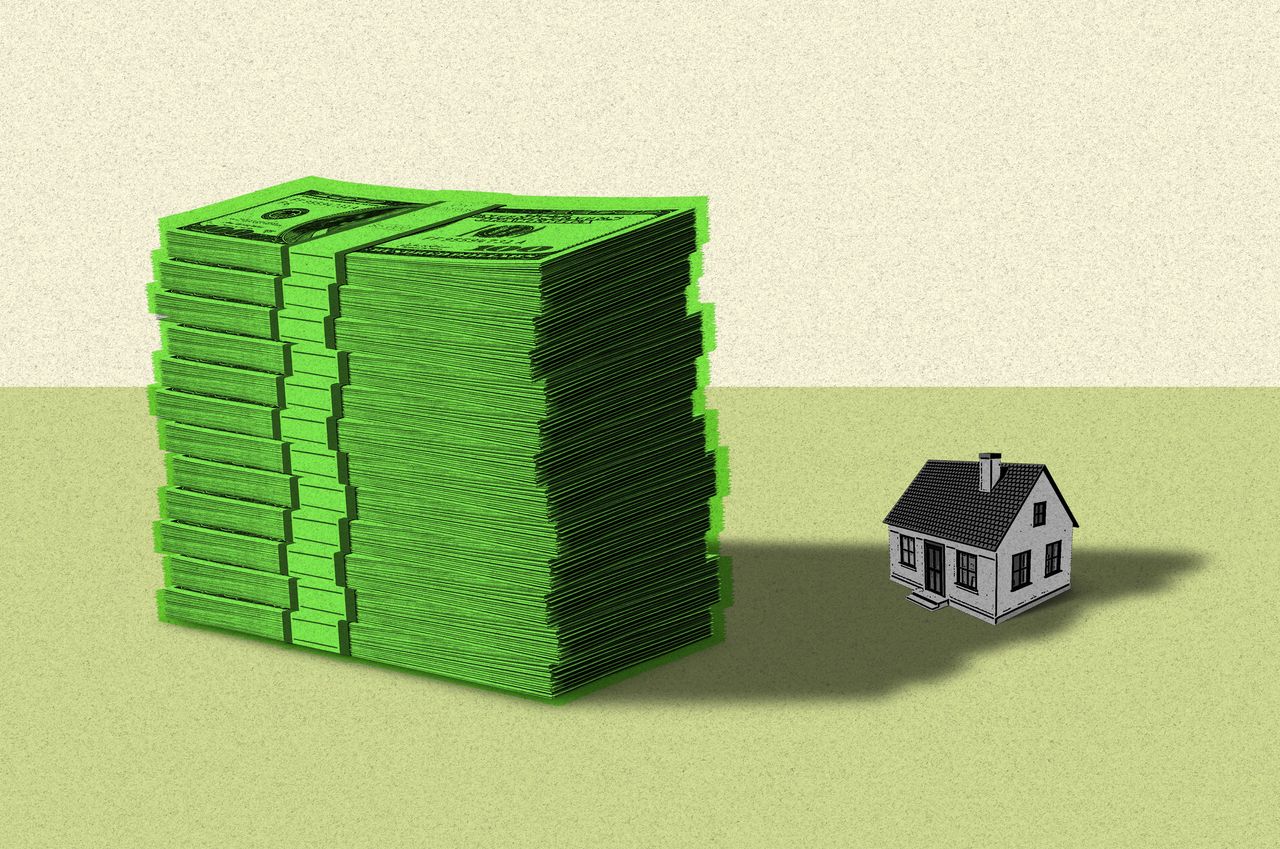

One of the first things many people do when they inherit their parents’ home these days is put up a for-sale sign.

Deciding what to do with a family property is often both an emotional and financial decision, but the rising costs of renovations, property taxes and utilities are making it harder for adult children to hold on to the real estate, financial advisers say. Higher home prices and mortgage rates have often also made it impractical for heirs to buy out their siblings, said Dick Stoner, a Realtor in Rockville, Md.

The high home prices of the past few years have made the decision to sell even more attractive. If inheritors can unload a house in a hot location for a high price, the proceeds from the home’s sale can help secure their finances and fund goals such as retirement, advisers say.

“For inheritors, cash is king,” said Paige Wilbur, Wells Fargo’s head of estate services.

Cash over sentimental value

Leaving a home to children remains a common way to transfer wealth, according to financial advisers and estate planners. There is no recent data that tracks home inheritance nationally.

More than three-quarters of parents plan to leave a home to their children when they die, according to a 2023 Charles Schwab survey of more than 700 American investors between the ages of 27 and 95. Some children may be reluctant to sell for sentimental reasons, but finances and simplicity of unloading a property often win out. Nearly 70% of those who expect to inherit a home from their parents plan to sell it, the survey found.

When Heidi Whaley and her sister, Melissa Mills, inherited their parents’ home, they chose to put it on the market. They recently listed the Charleston home for just below $3.5 million. The sisters, both retired, felt some sadness letting go of the home they grew up in and where their parents hosted many waterfront parties.

“My father wanted to build a house that would be strong, one which would be passed from generation to generation,” said Whaley.

Both sisters are empty-nesters with their own nearby homes, and said they couldn’t justify the expense of maintaining a nearly 4,000-square-foot house for the sake of fond memories.

Rising costs are a bigger part of the calculus these days when heirs decide whether or not to keep an inherited house, real-estate agents say. For instance, the higher cost to insure coastal homes in the Southeast is pushing more heirs in the area to sell, said Ruthie Ravenel, a Realtor in Charleston.

Inflation has also made repairs and upkeep on older properties more expensive, leading some to favour newer properties that may be cheaper to maintain and insure, she said.

I’ll keep the vacation home, though

The declining interest in keeping Mom and Dad’s home is part of a broader generational trend among inheritors, estate planners say.

Some tangible assets aren’t considered as valuable as they were in the past, thanks partly to changing tastes, said Wilbur with Wells Fargo’s estate services.

Renovation is expensive and what one generation sees as on-trend, the other may not. For example, the younger generation of beneficiaries mostly don’t want older traditional furniture. Instead, they prefer the modern, farm-style chic look, said Wilbur.

“While Mom and Dad’s home might be nice, the children may not want to live in it and would consider it too costly to renovate to their style,” she said.

Vacation homes and secondary properties, however, are more likely to be kept by heirs, at least for a few years, especially if it is in an appealing location, financial planners say. If multiple family members are inheriting a vacation house, there needs to be a way to split maintenance costs fairly and create a usage schedule that is to everyone’s liking, said Jeff Fishman, a financial adviser in Los Angeles.

Consider the taxes

Taxes remain a key reason many heirs sell relatively soon, financial advisers say.

Aaron Buchbinder, a real-estate agent in Boca Raton, Fla., is working with three brothers who inherited their grandmother’s condominium this year in Boca Raton and none of them live in Florida. They discussed keeping it and renting it out, but none of them wanted to keep it long term and preferred to sell because of the carrying cost of the homeowners association fees and taxes, said Buchbinder.

Heirs who wish to buy out their other siblings will want to use a reasonable method for valuing the home, said John Voltaggio, a managing director at Morgan Stanley Private Wealth Management. The family may decide to use the value reported on the estate tax return if it is recent, or they may want to obtain a few appraisals and use an average, he said.

The family members inheriting the property will also want to make sure they aren’t getting in over their head financially, with mortgage rates hovering around 7%.

“Many financial decisions today are very rate-dependent, so remove emotions or risk doing something you may later regret,” said Fishman, the financial adviser in Los Angeles.

A home’s cost basis—which is the starting point for measuring a future taxable gain—resets to market value, typically its value at the date of death, said Eric Smith, a spokesman for the Internal Revenue Service.

Any increase in value after death is taxed as long-term capital gains, and those rates are lower than the rates on short-term gain. But if a home is sold quickly, there is likely to be little gain if any and little to no tax, said Smith.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Sydney Children’s Hospitals Foundation CEO Kristina Keneally says Australia’s culture of large-scale philanthropy is becoming more sophisticated as Gold Dinner raises $75.5 million for children’s health, research and innovation.

The Federal Budget has created a supply freeze that could push rents higher, reduce investment and hand more of Australia’s housing stock to offshore institutions.

4 min

For months, I have been one of the few commentators openly stating what the data was already showing: property prices had begun to fall.

The latest figures confirm it. Cotality’s June 1 Home Value Index showed Sydney values down 0.9 per cent in May and Melbourne down 0.8 per cent. ANZ has cut its national capital city forecast to 2.8 per cent growth this year, down from 4.8 per cent in April. CBA has also downgraded its outlook.

So the Federal Budget arrived at the worst possible time, with the wrong prescription, to treat a problem it fundamentally misunderstands.

Treasurer Jim Chalmers has suggested that making it easier for first-home buyers to get a fair crack at auctions is a good thing. The reality is more complicated.

Driving property prices down does not simply hand a discount to first-home buyers. It affects the 1.4 million Australians employed by the property sector, the 67 per cent of household wealth tied to housing, and the state government revenues that fund schools, hospitals and roads.

The government had a choice: tackle supply constraints, link migration growth to housing completions and reduce spending, or increase taxes on property investors. It chose the latter.

Property is an economic pillar

Property is not simply another investment class. It contributes about 10.6 per cent of GDP directly, up to 15 per cent when flow-on effects are included, and employs more than 1.4 million Australians. It also generates more tax revenue than mining and underpins consumer confidence through the wealth effect.

Against that backdrop, the Budget removed negative gearing from established residential properties purchased after Budget night and replaced the 50 per cent capital gains tax discount with cost-base indexation and a 30 per cent minimum tax from July 1, 2027.

The government calls this fairness. I call it a misdiagnosis.

The grandfathering trap

The policy is also internally contradictory.

Properties purchased before Budget night are grandfathered, allowing existing investors to retain full negative gearing and capital gains tax benefits until they sell. The logical response is simple: hold.

That means fewer properties coming onto the market, fewer rental listings and reduced transaction volumes.

The result is likely to be higher rents, reduced stamp duty revenue and further inflationary pressure at a time when the Reserve Bank remains focused on bringing inflation under control.

The government is attempting to fight inflation with one hand while fuelling it with the other.

Who really owns investment properties?

What is often lost in this debate is who Australia’s property investors actually are.

According to ATO data, 71 per cent of investors own just one investment property. They are not wealthy property moguls.

They are teachers, nurses, police officers and small business owners who have purchased an investment property as part of their retirement strategy.

For many Australians, property remains the most tangible and trusted pathway to building long-term wealth.

Removing the incentives that supported that investment does not hurt a billionaire developer. It hurts ordinary Australians trying to secure their financial future.

Investors aren’t the affordability problem

It is true that housing affordability has deteriorated significantly over the past two decades. However, negative gearing is not the primary cause.

Research by economists Ross Kendall and Peter Tulip found planning and zoning restrictions significantly increase housing costs.

Their work showed zoning lifted detached house prices well above marginal construction costs in Sydney, Melbourne, Brisbane and Perth.

Low interest rates, strong population growth, chronic under-supply and restricted access to development-ready land have all played a much larger role in pushing prices higher.

Punishing private investors does nothing to address these structural issues.

The Build-to-Rent advantage

At the same time the government is reducing incentives for Australian investors, it has created a more attractive tax environment for foreign institutional capital through Build-to-Rent projects.

Under current arrangements, foreign institutional investors can access a 15 per cent withholding tax rate through Managed Investment Trusts, accelerated depreciation benefits and exemptions from the new negative gearing restrictions.

State governments have added further concessions, including land tax reductions and exemptions from foreign investor surcharges.

Australian mum-and-dad investors receive none of these advantages.

The cumulative effect is striking. Foreign institutions can access a range of tax benefits unavailable to Australian private investors, while local investors lose concessions they have relied upon for decades.

This is not solving the housing crisis. It risks transferring ownership of Australia’s rental housing stock from local investors to offshore institutions.

Why state governments should worry

There are already signs these changes are affecting the credit cycle.

Major banks are removing negative gearing benefits from serviceability calculations for investment loans.

As market conditions soften, lenders become more cautious and investors find it harder to secure finance.

That matters because property transactions are a major source of state government revenue.

In NSW alone, transfer duty generates more than $12 billion annually. If transaction volumes fall significantly, the impact on state budgets will be substantial.

The consequences extend beyond stamp duty to GST collections, payroll tax receipts and land tax revenue.

The 95 per cent loan trap

There is another aspect of the Budget that concerns me.

The government has expanded first-home buyer deposit guarantee schemes, allowing eligible purchasers to buy with a five per cent deposit backed by the Commonwealth.

The intention is admirable. The timing may not be.

If prices in Sydney and Melbourne fall further, buyers entering the market with 95 per cent loan-to-value mortgages could quickly find themselves in negative equity.

They become trapped. They cannot sell without crystallising a loss, while the taxpayer guarantees the loan and the bank remains protected.

That is not wealth creation. It is a debt obligation.

After three decades working with debt and investment, I would never encourage my own children to borrow at a 95 per cent loan-to-value ratio.

A policy built on politics

The government had an opportunity to address the housing crisis by encouraging supply, reforming planning systems and reducing development costs.

Instead, it chose Robin Hood politics.

The optics may be appealing, but the economics are not.

Australians may ultimately pay the price through higher rents, weaker investment and a future in which an increasing share of the nation’s housing stock is owned by offshore institutions rather than local investors.

Paul Miron is the Co-Founder & Fund Manager of Msquared Capital.

Chinese carmaker GAC will expand its Australian electric vehicle line-up with the city-focused AION UT hatchback.

As the season turns, Handpicked Wines’ latest Pinot Noir and Chardonnay releases reveal how subtle shifts in place shape what ends up in the glass.