Japan Long Looked Down at Luxury Penthouses. Now Things Are Looking Up.

Once considered an ostentatious display of wealth, extravagant top-floor spaces are suddenly in demand

6 min

6 min

Ken Akao, a 35-year-old cosmetic surgeon, was a little concerned when he bought a multimillion-dollar Tokyo apartment in October 2023. It wasn’t about the property itself, a three-bedroom, 39th- floor penthouse with a spiral staircase, Jacuzzi and infinity pool. It was about what his father, a frugal Japanese diplomat of the old school, would think after seeing a property so grand—and so un-Japanese.

After some time, Akao summoned the courage to invite his dad for a visit. To his relief, he says, the elder Akao enjoyed the tour and pronounced the pad “wonderful.”

A century after the Park Avenue penthouse became established as the height of residential luxury for New Yorkers, the concept has finally made it across the Pacific to Tokyo. Part of the credit goes to people with foreign experience such as the younger Akao, who grew up largely overseas, as well as the influence of Chinese buyers flooding into Japan these days.

It also reflects changing values about what constitutes the ideal property in Tokyo.

Japan’s capital first flourished in the 17th century as the seat of the shogun, or generalissimo, who reigned as Japan’s de facto ruler. The Tokugawa family of shoguns, having subjugated feudal lords across the land, insisted that the lords spend half their time in the capital. Soon the city then known as Edo was dotted with spacious compounds where grandees lived in sprawling low-slung wooden homes watched by the shogun’s spies.

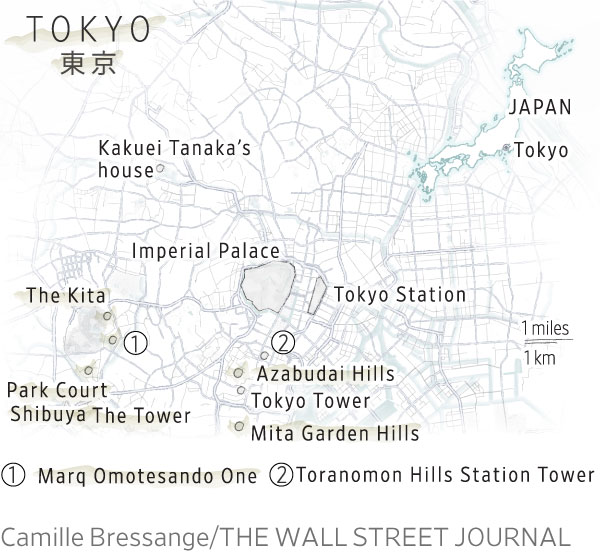

Long after Edo became Tokyo and feudalism ended in 1868, those properties served as the prototype for the rich. Kakuei Tanaka, a poor man from the provinces who got wealthy with business ventures while rising to become Japan’s prime minister between 1972 and 1974, used to hold court inside the walls of a leafy compound in the Mejiro area of Tokyo, where he could feed the carp in his pond. (The house was destroyed by fire on Jan. 8. No one was hurt.) In a country that tends to frown on ostentation and special treatment for the privileged, the high walls surrounding such properties offered privacy.

These days, most rich Japanese still prefer to keep their wealth under wraps. But other changes have made a luxury condominium in a prime central Tokyo location look attractive compared with a house on a spacious property in a residential area.

One is the burst of the land-price bubble in the early 1990s, which shattered the myth of land as an indestructible store of value. These days, say real-estate professionals, bankers are less inclined to insist on land as collateral and more willing to extend loans backed by quality condos that are seen as likely to retain value across economic cycles. Also, in an ageing country where labor is in short supply, many older couples look askance at trying to care for large grounds. “Weeding is such a pain for old people,” said Satoshi Omori, president of a Tokyo real-estate appraisal firm.

The 2011 earthquake in northeastern Japan boosted the appeal of living in an earthquake-resistant concrete building in a central location rather than a wooden house farther out, where services might be hard to come by in an emergency.

“Compact cities are a global trend and people tend to prefer places that are more convenient,” said Shigeru Funabashi, a Tokyo broker.

Funabashi is a cosmetic surgeon who has in recent years shifted his career toward real estate, having developed a fascination with luxury residences. In 2011, he went to London to take a look at One Hyde Park, which is the location of a penthouse that was recently one of the highest priced in the city. He recalls thinking to himself, “Something like this will come to Tokyo someday.”

Foreign developers were ahead of the game in tapping the wellspring of demand Funabashi sensed and spreading the word “penthouse” in the Japanese language. In the Shibuya district, popular among tourists, Canadian developer Westbank in 2020 completed a five-floor condominium designed by architect Kengo Kuma. Traditionally, such buildings had nothing fancier on the top floor than plumbing and electrical equipment. But Westbank put in a multilevel penthouse with a private infinity pool on the roof. It sold early last year for $50 million, according to the developer.

Some other buyers in the building bought two units to combine them. “It really showed us that there is this massive gap in the market for products at this level,” a Westbank representative in Japan said. She said that if Westbank had the chance to build the 12-unit property again, it would make it with only six units.

Marq Omotesando One is another luxury low-rise condominium by foreign developers in central Tokyo that was completed in 2021. The development, led by a unit of Hong Kong-based investment firm BPEA, features a 6,700-square-foot penthouse with roof pool that local agents said has been listed at a price in the tens of millions of dollars. Its current status couldn’t be determined.

At Japanese real-estate development companies, “no one really wanted to rock the boat or do anything different,” said Zoe Ward, a real-estate agent originally from Australia who has worked for 15 years in Japan’s property market. But they changed course after seeing foreign developers building extravagant properties and selling units at high prices never seen before, Ward said.

Japanese developers say that many customers of ultra expensive condos are locals, including corporate executives and younger entrepreneurs who are often familiar with high-end homes in places such as New York and London.

Azabudai Hills, a Mori Building project in central Tokyo that includes offices and apartments, opened on Nov. 24. The development includes what is currently the tallest building in Japan, with 91 Aman-branded apartments on high floors. Planning documents submitted to authorities show there are three duplex penthouse units on the 64th floor. The largest unit occupies half the floor and has a private pool, the documents indicate. Local brokers say all three have been sold.

Mori Building declined to release floor plans or price ranges for those apartments—a reminder that the rich here still don’t want their private business aired, even if their high-rise homes are visible dozens of miles away. A local publication, Daily Shincho, reported that the largest unit sold for the equivalent of $200 million, which would make it the highest-price condo ever sold in Japan by a multiple of two or three.

Swimming pools on rooftops are rare in Japan, partly because of concerns about water leaking during earthquakes. But that is also changing. A central Tokyo office-hotel building developed by Mori Building opened in October with restaurants and an infinity pool on the roof.

“The rooftop was never utilised in Japan as much as it should be,” said architect Shohei Shigematsu, who designed the building. He said his team added extra drainage to reassure the developer that water wouldn’t splash on passersby 49 floors below in the event of an earthquake.

More luxury penthouses are on the way, including several on the top floor of a 13-story building at Mita Garden Hills, a project jointly developed by units of Mitsui Fudosan and Mitsubishi Estate. The building won’t be completed until 2026, but Mitsui says all of the penthouses have been sold.

The most expensive one, with a floor area of about 4,000 square feet, sold for 5.5 billion yen, equivalent to about $38 million, according to a broker familiar with the deal. Mitsui declined to comment.

In Osaka, the centre of Japan’s second-largest urban area after the Tokyo region, a penthouse in a 46-storey building, due to be completed in December 2025, is listed for the equivalent of about $17 million. The price for the unit, which at 3,300 square feet is the building’s largest, would be the highest price ever for an Osaka-area condo, said a spokesman for Sekisui House, one of the developers.

The spokesman said the penthouse has the vibe of a European guesthouse for visiting dignitaries, with chandeliers hanging from ceilings that are as high as 16 feet. Some other units feature an elevator to carry the owner’s car into the premises.

While ultrahigh-price deals are usually not included in industry databases, prices of Tokyo apartments generally are rising, driven by the higher cost of materials and labor. The Real Estate Economic Institute, a Tokyo-based firm tracking the property market, said the average price of a new apartment sold in central Tokyo for the six months through September was up 36% compared with the same period a year earlier and topped 100 million yen, equivalent to about $700,000, for the first time.

Akao, the cosmetic surgeon and recently minted penthouse owner, says he grew fond of the luxury lifestyle when visiting Aman hotels in Japan and Greece. He wasn’t able to get his hands on one of the Aman units in Azabudai Hills, but found a good substitute in his penthouse across from Yoyogi Park, a central Tokyo urban oasis like New York’s Central Park.

There is an en-suite bathroom in the primary bedroom, rare for a Japanese home, and Miele appliances in the kitchen. The staircase from the living-dining area, which features sofas from Arflex Japan, leads to an open-air 700-square-foot deck with the infinity pool.

“I often have large group get-togethers,” Akao said. “The pool will make gatherings easier.”

Akao said that growing up in the U.S., Switzerland and Austria where his father was posted made him familiar with the lifestyle because some of his classmates lived in houses with a pool and talked about it casually at school.

While analysts say most of the recently built penthouses are bought by people who intend to live in them, there are still flippers. Akao might be one of them. He said he is trying to sell his unit before considering whether to move in. He declined to disclose what he paid but said he was asking the equivalent of about $9 million.

—Peter Landers contributed to this article.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

From citrus oils to warming spices, the classic G&T is being reimagined at home as a more thoughtful, seasonal ritual for modern entertaining.

ABC Bullion has launched a pioneering investment product that allows Australians to draw regular cashflow from their precious metal holdings.