China’s Growth Slows to Three-Decade Low Excluding Pandemic

A festering property-market meltdown offsets much of the benefit of economy’s post pandemic recovery

6 min

6 min

HONG KONG—China’s economic growth rate finished at one of the lowest levels in decades last year, underscoring the heavy toll that a property-sector collapse and weak consumer confidence have taken on the world’s second-largest economy despite the lifting of all Covid-19 restrictions.

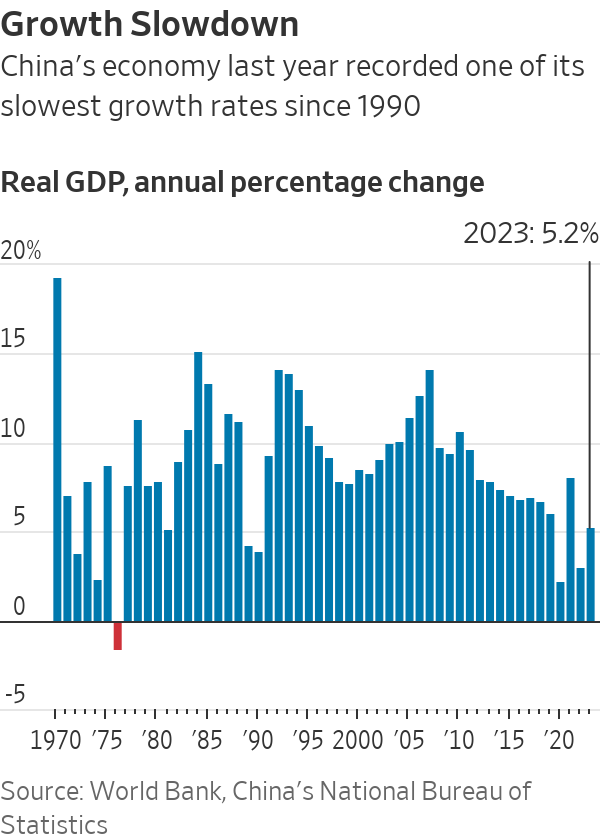

Gross domestic product in China expanded 5.2% in the fourth quarter and for the full year in 2023, according to data released by the National Bureau of Statistics on Wednesday. The reading confirmed a number uttered by Premier Li Qiang a day earlier at the World Economic Forum in Davos, Switzerland—an unusual disclosure of a high-profile data point by a senior leader before its formal release.

Apart from the three years that China was closed to the outside world during the pandemic, the country’s economy expanded in 2023 at the slowest annual rate since 1990, the year after the political turmoil of the student movement that was crushed around Beijing’s Tiananmen Square in June 1989.

In 2022, China’s economy grew 3%, while 2020—the initial year of Covid-19—saw growth of just 2.2%. This year’s outcome was flattered in part by comparison with the relatively low base of 2022, when harsh pandemic lockdowns swept the nation, crimping growth.

Last year’s 5.2% growth rate managed to top the government’s official target of around 5% growth, following a year of volatility and shifting expectations.

Maintaining growth at a similar pace this year may prove harder, given policymakers’ hesitance so far to launch any big-ticket stimulus packages. Forecasts for China’s growth rate this year among several global investment banks range from 4% to 4.9%. China is expected to announce any formal growth target at an annual legislative session set to take place in March.

In the near term, China has few obvious growth drivers. Export demand is softening as the global economy is projected to slow this year. Chinese families, hit by years of pandemic restrictions and receiving no direct financial support from the government, have turned cautious on spending amid a weak job market. Private businesses have been holding off on new investments while foreign investors are pulling funds out of the country.

The Chinese leadership’s determination to cultivate new engines of growth, in fields such as electric vehicles and renewable energy, is bearing fruit. Still, in the near term, it won’t likely be enough to make up for the shortfalls in job creation and overall growth rate from the rapid decline in its once-mighty real-estate sector.

In the longer run, China faces a daunting list of headwinds, including a population that is rapidly skewing older, high debt levels and a worsening external political environment that has seen relations with the U.S.-led West plummet.

Wednesday’s data release offered fresh signs of the dire state of the country’s demographics. Official statisticians said China’s population shrank by 2.08 million people last year, falling to 1.410 billion, after declining in 2022 for the first time in decades.

Economists are concerned that China may be falling into a vicious cycle in which falling prices and weak demand reinforce one another, as they did in Japan in the 1990s. Chinese policymakers’ reluctance to stimulate more forcefully has confounded many economists, though others have pointed to leader Xi Jinping’s ideologically-rooted reluctance to shower the economy with government money.

Instead, Chinese authorities have unleashed a barrage of smaller-bore measures, such as trimming key interest rates, cutting mortgage costs for home buyers and prodding banks to lend more to distressed property developers. Collectively, though, those measures have done little to reverse downward pressure on the economy. The government said in the fall that it would issue $137 billion in government debt, the biggest stimulus measure it has undertaken so far—though still not enough to reverse the downward momentum, economists say.

“I wonder if they are not realising how big the risk is if deflation pressure becomes entrenched,” says Alicia García-Herrero, chief Asia economist at investment bank Natixis.

Chinese stocks fell after the data was released. The CSI 300 index was down 1.4%, putting it on course to close at its lowest level in almost five years. Hong Kong’s Hang Seng Index, which includes the shares of many Chinese companies, was around 3.7% lower.

The country’s stock market is now in a multi-year slump, with foreign portfolio managers fleeing and individual investors in the country switching to safer assets. The poor state of the economy is a constant concern.

The past year had started off with a sense of buoyant optimism, as the abandonment of three years of stifling Covid-related restrictions spurred a revival of spending by consumers.

But the reopening momentum quickly lost steam after the first quarter, as global demand for Chinese-made exports—a key pillar of China’s economy throughout the pandemic years—began to wane. Persistent high youth unemployment and weak wage growth further weighed on average households’ fragile confidence.

In the fall, factory activity weakened again and consumer prices dropped into deflationary territory.

Throughout it all, a years long decline in Chinese home prices showed no sign of abating, further depriving revenue for debt-laden developers and eroding homeowners’ wealth and sense of financial security.

Looking ahead, economists have called on leaders in Beijing to step in forcefully to stabilise home prices and contain the risk of widening defaults among property developers.

“The key thing to watch in 2024 is if and when the central government would step in and take the main responsibility to stop the contagion,” said Larry Hu, chief China economist at Macquarie Group.

Whether Beijing can revive consumer confidence will be another key metric to watch this year.

In the central Chinese city of Wuhan, Bella Liu, a 32-year-old employee of a telecommunications firm, remembered 2023 as a year marked by plunging profits and frequent layoffs in her industry. After suffering a nearly 20% loss from her mutual fund investments, she is now parking more of her money in time deposits at her bank.

“In an era of slowing economic growth, I just feel lucky that I have a job,” Liu said.

Full-year economic data released by China on Wednesday showed retail sales, a key gauge of consumer spending, gained 7.4% in December and rose 7.2% for the full year compared with the respective year-earlier periods. Retail sales had fallen 0.2% for the full year in 2022.

The new data suggest that the economy is again beginning to rely more on domestic demand after counting on exports as the main pillar of growth during the pandemic years. Consumption was the largest contributor to overall growth in 2023. Still, it is unclear how much of a role it will play in driving the Chinese economy this year, in part because the release of pent-up pandemic demand has largely run its course, according to economists from Nomura.

Investment was also lacklustre in 2023. Fixed-asset investment growth slowed last year, rising 3.0% for the full year compared with a 5.1% expansion in 2022. Private-sector investment, too, remained weak, falling 0.4% in 2023 compared with a year earlier as policy uncertainty spooked entrepreneurs. Private-sector investment had risen 0.9% in 2022.

Over the course of 2023, Beijing rolled out measures aimed at reining in the technology sector, including the video game industry, while warning about foreign espionage and detaining employees of foreign firms operating in China.

Readings of the property sector offered more reason for caution. New home prices in China’s 70 major cities dropped at a faster clip toward the end of 2023.

Average new home prices in December fell 0.45% from November, and 0.89% when from a year earlier, according to calculations by The Wall Street Journal based on data released by the statistics bureau. The pace of both declines was worse than in November.

For the full year, property investment fell 9.6%, while new construction starts dropped 20.4% and home sales by value declined 6.0%.

The surveyed urban unemployment edged up to 5.1% in December, from 5% in November. Economists have cast doubt on the accuracy of official statistics on joblessness in large part because the survey leaves out the country’s nearly 300 million migrant workers.

In a surprise move, China released a revised youth unemployment figure for the first time since July, when it abruptly suspended the publication of the data series amid a run of fresh record-high readings up to 21.3%.

On Wednesday, China’s statistics bureau said that it would publish a new urban youth unemployment figure each month for people age 16 to 24 that excludes students. The reading was 14.9% in December.

The statistics bureau said that the new methodology offers a more refined and comprehensive picture that would “better reflect the employment situation” by only including graduates who were looking for work.

Still, the economy had pockets of strength, especially in dominating the global supply chain for renewable energy products such as solar panels and electric vehicles. Growth in industrial production rebounded to 4.6%, accelerating from a 3.6% increase the year before, Wednesday’s data show.

—Grace Zhu and Xiao Xiao in Beijing contributed to this article.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

With two waterfronts, bushland surrounds and a $35 million price tag, this Belongil Beach retreat could become Byron’s most expensive home ever.

From office parties to NYE fireworks, here are the bottles that deserve pride of place in the ice bucket this season.