Investments in Solar Power Eclipse Oil for First Time

Government spending, including Biden’s Inflation Reduction Act, has helped drive a gap between clean-energy spending and fossil-fuel investments

3 min

3 min

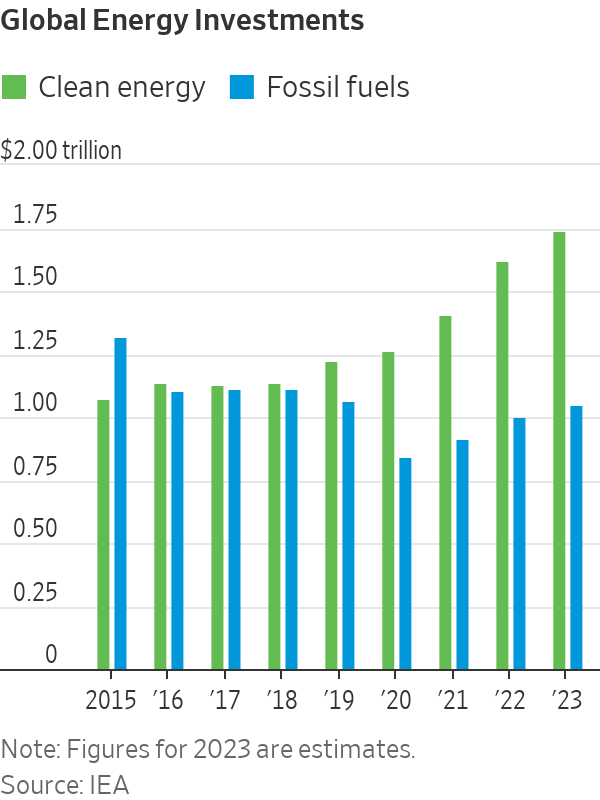

Investments in solar power are on course to overtake spending on oil production for the first time, the foremost example of a widening gap between renewable-energy funding and stagnating fossil-fuel industries, according to the head of the International Energy Agency.

More than $1 billion a day is expected to be invested in solar power this year, which is higher than total spending expected for new upstream oil projects, the IEA said in its annual World Energy Investment report.

Spending on so-called clean-energy projects—which includes renewable energy, electric vehicles, low-carbon hydrogen and battery storage, among other things—is rising at a “striking” rate and vastly outpacing spending on traditional fossil fuels, Fatih Birol, the IEA’s executive director said in an interview. The figures should raise hopes that worldwide efforts to keep global warming within manageable levels are heading in the right direction, he said.

Birol pointed to a “powerful alignment of major factors,” driving clean-energy spending higher, while spending on oil and other fossil fuels remains subdued. This includes mushrooming government spending aimed at driving adherence to global climate targets such as President Biden’s Inflation Reduction Act.

“A new clean global energy economy is emerging,” Birol told The Wall Street Journal. “There has been a substantial increase in a short period of time—I would consider this to be a dramatic shift.”

A total of $2.8 trillion will be invested in global energy supplies this year, of which $1.7 trillion, or more than 60% will go toward clean-energy projects. The figure marks a sharp increase from previous years and highlights the growing divergence between clean-energy spending and traditional fossil-fuel industries such as oil, gas and coal. For every $1 spent on fossil-fuel energy this year, $1.70 will be invested into clean-energy technologies compared with five years ago when the spending between the two was broadly equal, the IEA said.

While investments in clean energy have been strong, they haven’t been evenly split. Ninety percent of the growth in clean-energy spending occurs in the developed world and China, the IEA said. Developing nations have been slower to embrace renewable-energy sources, put off by the high upfront price tag of emerging technologies and a shortage of affordable financing. They are often financially unable to dole out large sums on subsidies and state backing, as the U.S., European Union and China have done.

The Covid-19 pandemic appears to have marked a turning point for global energy spending, the IEA’s data shows. The powerful economic rebound that followed the end of lockdown measures across most of the globe helped prompt the divergence between spending on clean energy and fossil fuels.

The energy crisis that followed Russia’s invasion of Ukraine last year has further driven the trend. Soaring oil and gas prices after the war began made emerging green-energy technologies comparatively more affordable. While clean-energy technologies have recently been hit by some inflation, their costs remain sharply below their historic levels. The war also heightened attention on energy security, with many Western nations, particularly in Europe, seeking to remove Russian fossil fuels from their economies altogether, often replacing them with renewables.

While clean-energy spending has boomed, spending on fossil fuels has been tepid. Despite earning record profits from soaring oil and gas prices, energy companies have shown a reluctance to invest in new fossil-fuel projects when demand for them appears to be approaching its zenith.

Energy forecasters are split on when demand for fossil fuels will peak, but most have set out a timeline within the first half of the century. The IEA has said peak fossil-fuel demand could come as soon as this decade. The Organization of the Petroleum Exporting Countries, a cartel of the world’s largest oil-producing nations, has said demand for crude oil could peak in developed nations in the mid-2020s, but that demand in the developing world will continue to grow until at least 2045.

Investments in clean energy and fossil fuels were largely neck-and-neck in the years leading up to the pandemic, but have diverged sharply since. While spending on fossil fuels has edged higher over the last three years, it remains lower than pre pandemic levels, the IEA said.

Only large state-owned national oil companies in the Middle East are expected to spend more on oil production this year than in 2022. Almost half of the extra spending will be absorbed by cost inflation, the IEA said. Last year marked the first one where oil-and-gas companies spent more on debt repayments, dividends and share buybacks than they did on capital expenditure.

The lack of spending on fossil fuels raises a question mark around rising prices. Oil markets are already tight and are expected to tighten further as demand grows following the pandemic, with seemingly few sources of new supply to compensate. Higher oil prices could further encourage the shift toward clean-energy sources.

“If there is not enough investment globally to reduce the oil demand growth and there is no investment at the same time [in] upstream oil we may see further volatility in global oil prices,” Birol said.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

This stylish family home combines a classic palette and finishes with a flexible floorplan

Just 55 minutes from Sydney, make this your creative getaway located in the majestic Hawkesbury region.

Excess investment in industry isn’t made up by trading partners, and it has domestic consequences

2 min

In the “ China Shock 2.0 ” narrative, not only is China a security threat and a low-end factory competitor, but it is also angling to swamp the West with cut-rate high-tech goods. There has been less focus on the downsides of such a strategy for China itself.

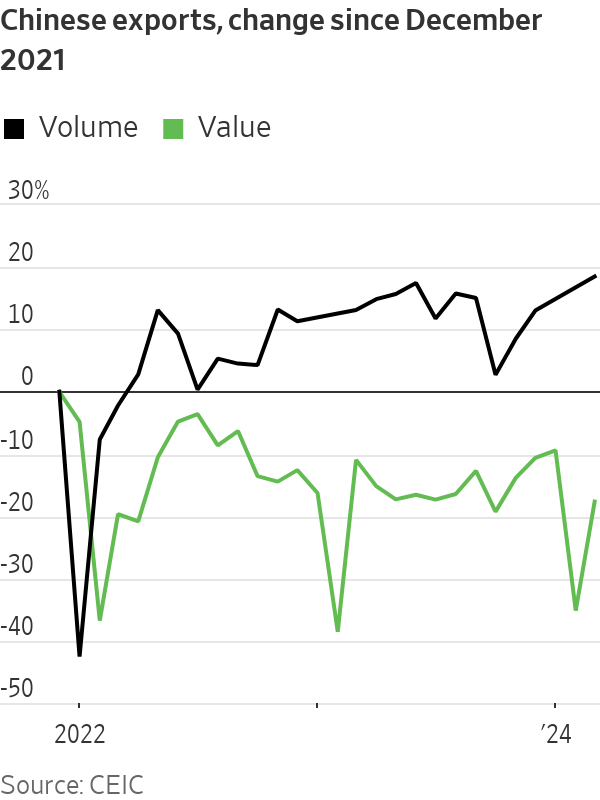

China’s first-quarter growth beat most estimates , rising 5.3% on the year—thanks mostly to strong industrial output and exports. But the economic data released Tuesday also showed that excess capacity is very real, and could be damaging to China itself.

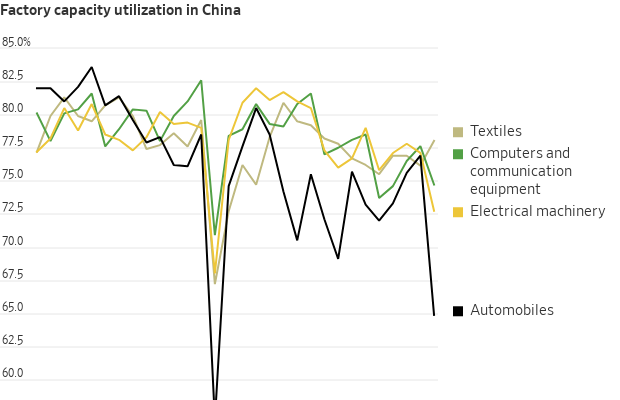

While China’s industrial engine revved up in January and February , it downshifted again in March: output rose just 4.5% on the year, down sharply from January and February’s 7%. More tellingly, manufacturing capacity utilisation plummeted to 73.8% in the first quarter—its weakest, excluding the pandemic-affected first quarter of 2020, since at least 2015. In volume terms, China’s exports hit a nearly 10-year high in March. But in value terms they were barely above where they sat in October.

In other words, firms’ pricing power both at home and abroad is weakening and margin pressure is probably mounting: The March industrial financial data, which will be released later this month, will be worth watching.

So will private investment in manufacturing. If external demand, in value terms, doesn’t find a stronger footing soon and China’s domestic economy remains weak, then eventually such investment will need to slow. Otherwise the government, or state-owned banks, will have to start absorbing the cost of too many loans to industry more directly, as they already have with real estate and infrastructure .

Particularly interesting is the breakdown of that capacity utilisation data itself. Falling run rates were especially obvious in Beijing’s favourite sectors like automobiles and electrical equipment—the so-called “new productive forces,” including electric vehicles, chips and solar panels, which policymakers have highlighted in recent speeches and have been stalking Western politicians’ nightmares. Automobile manufacturing utilisation rates fell below 65% in the first quarter: well below their previous low (excluding the first quarter of 2020) of 69.1% in mid-2016.

China’s traditional export sectors, on the other hand, have actually held up relatively well. Textiles utilisation rose in the first quarter, while run rates for computer and communication gear fell, but much less sharply.

Meanwhile, economy wide borrowing—excluding government bond issuance—weakened further in March, despite bond yields and interest rates near multiyear lows. If margin pressure starts to force some “new productive forces” to start slowing investment, fiscal policy would need to step in to prop up growth.

Alternatively, China can keep funnelling its excess savings into new manufacturing overcapacity—but Chinese banks and Beijing, not just China’s trade partners, will eventually end up footing the bill.

This stylish family home combines a classic palette and finishes with a flexible floorplan

Consumers are going to gravitate toward applications powered by the buzzy new technology, analyst Michael Wolf predicts