In France, Investors Get the Centrist Limbo They Wanted

Polarisation has for years left the country’s politics stuck in an unpopular middle ground, and the latest elections won’t change that

3 min

3 min

When it comes to France’s turbulent politics , the current impasse is probably the best investors could have hoped for.

The second round of French legislative elections delivered a widely expected hung parliament, but not its predicted makeup: Rather than coming in first, Marine Le Pen ’s far-right and anti-immigrant National Rally finished third. In a shock twist , the leftist New Popular Front alliance emerged victorious, with the party of President Emmanuel Macron and its allies in second place.

This is because leftists and centrists ended up coordinating. In many local races, candidates dropped out to avoid dividing the vote against the far right. Still, no party has an outright majority, which plunges the country into political gridlock. This was, counterintuitively, the preferred outcome for financial markets.

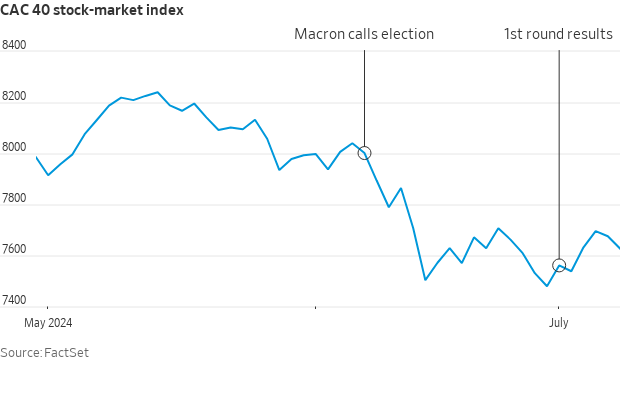

The CAC 40 initially tumbled when the elections were called in June, driven by fears of a potential National Rally government challenging the European Union with fiscally expansive plans. Then the French stock benchmark perked up, as the first-round results suggested that the far-right wouldn’t get a majority.

Yet markets remained volatile because the rise of the New Popular Front raised even greater concerns. The policies of this coalition, in which leftist firebrand Jean-Luc Mélenchon is a key leader, also include more public spending, on top of widespread tax increases. Indeed, the CAC 40 closed down 0.6% Monday, probably reflecting investors’ concerns about these parties potentially managing to form a new government. Mélenchon has stated that there will be no deals with the centrists.

These worries seem overblown. Yes, there are doubts about how France will handle its budget deficit, which amounted to 5.5% of gross domestic product in 2023 and has forced the EU to launch an “excessive deficit procedure” against the country. Macron may need to accept the reversal of reforms such as a higher retirement age.

Still, a fiscal crisis isn’t in the cards, because the European Central Bank is ultimately in control of France’s bond market.

As for economic growth, it is unclear how much impact Macron’s policies have had in the first place, particularly given resistance from unions and swaths of the public, which resulted in the famous “yellow vest” protests in 2018 and 2020.

What matters for sectors battered in the stock market, including banks, energy firms and infrastructure operators, is that the risk of widespread tax increases, nationalisations and a prolonged standoff with Brussels seems smaller now than a few weeks ago. Whatever Mélenchon says, the left will either have to compromise or else form a minority government that might scare investors but wouldn’t be able to pass laws.

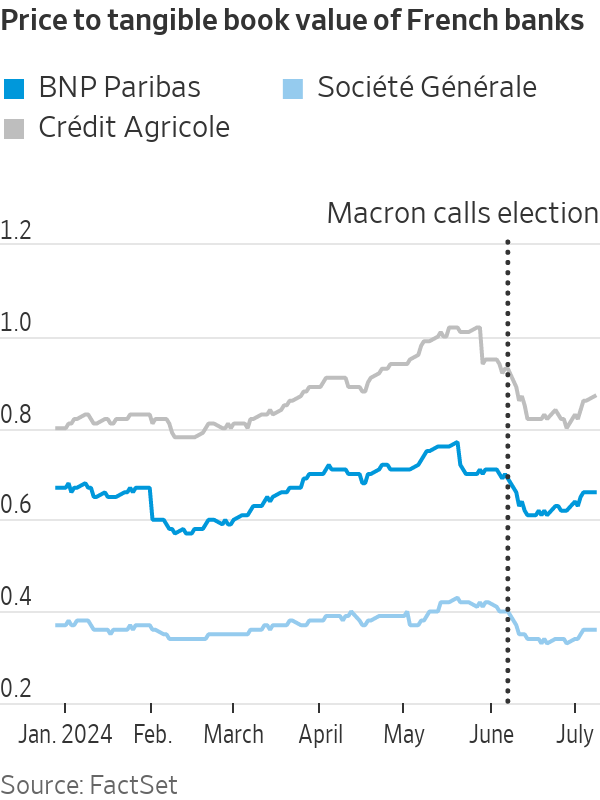

So there isn’t much justification for the lower valuation of lenders such as Société Générale and especially BNP Paribas —one of Europe’s most interesting banks that now trades at 0.65 times tangible book value. The same is likely true for firms such as energy utility Engie and infrastructure-concessions leader Vinci , which have lost 8% of their market value since the end of May.

These elections are more a symptom of Macron’s weakness than its cause. After a chaotic month, French politics is back where it has been for years, with a rising far right forcing the left to back a centrist platform that can achieve little because few people actually like it. Macron himself became president on an anti-Le Pen ticket, but in seven years has failed to rally broad support for his pro-business vision.

This could eventually make Le Pen’s victory inevitable, as she claimed after initial results came in. For now, though, it is more or less what markets ordered.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

A thoughtful timber-led renovation in Byron Bay has reimagined an existing house as a warm, resort-style family sanctuary grounded in natural materials.

Automobili Lamborghini and Babolat have expanded their collaboration with five new colourways for the ultra-exclusive BL.001 racket, limited to just 50 pieces worldwide.