What’s Killing Productivity? Some Think It’s the Banks

Bank lending in the U.K. is going to property rather than innovative businesses

4 min

4 min

LONDON—The birthplace of the industrial revolution is in dire need of innovation. Standing in the way: Britain’s mortgage-laden banks.

The U.K.—inventor of the factory system, steam engine and passenger rail—is at the forefront of a 21st-century global productivity slowdown. Growth in U.K. productivity, or output per hour worked, has halved since the financial crisis, leading some policy makers to call this era Britain’s lost decade. Among the world’s seven largest developed economies, only Italy has fared worse.

The causes are hotly debated, and include an ageing population, tighter regulation and the U.K.’s departure from the European Union. But a factor that has gained special attention: the way U.K. banks have tilted lending to the booming housing market.

Bank lending for projects that boost economic output, such as machinery and software, has stagnated. Research and regulators say the two trends are linked: As real-estate prices soared, banks shifted more capital toward housing, viewed as less risky because the loans were backed by tangible assets with rising values.

“The banking system is increasingly becoming a brake on the economy,” said Jonathan Haskel, a member of the Bank of England’s Monetary Policy Committee.

The U.K. is an extreme example of what’s happened in big economies around the world for the better part of this century. Central banks cut interest rates in the 2010s through early 2022 to make it cheaper for businesses to borrow and invest. But while debt rose sharply, most of it went toward real estate.

The world’s total assets—including those held by households, businesses and banks—more than tripled from 2000 to 2020, according to a report from the McKinsey Global Institute, a research group. Two-thirds are stored in real estate; only a fifth are in productivity-boosting assets such as factories, equipment and infrastructure, McKinsey said. “The historic link between the growth of net worth and the growth of GDP no longer holds,” the report said.

Among the world’s 10 biggest economies, the U.K. is tied with France for having the lowest share of net worth in assets that boost economic growth. Meanwhile, the U.K.’s home values and mortgage debt have exploded.

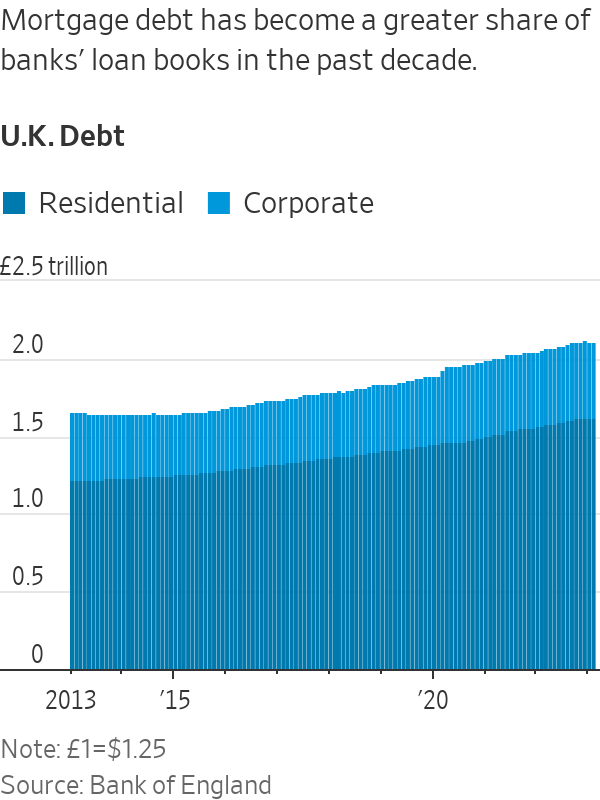

U.K. banks added £400 billion, equivalent to about $500 billion, to home lending in the decade through this February, Bank of England data show. Debt extended to businesses grew by only one-tenth of that amount.

The U.K.’s big banks “pulled back in the financial crisis and never really came back” in terms of business lending, said Richard Davies, a former regional head for Barclays’s U.K. business banking operations who now leads Allica Bank, a London startup that lends to small and midsize businesses. “The big banks are obsessed with residential mortgages.”

The obsession with mortgages leaves some businesses feeling sidelined.

Geometric Manufacturing, based in Tewkesbury, England, makes defence and cybersecurity products. Several years ago the firm asked a U.K. bank for a loan to design and manufacture a robotic arm to load its machines, an investment that would allow the factory to produce more with fewer workers, Managing Director Paul Wenham said.

Despite the option for a government guarantee through a U.K. program to help small businesses, the bank declined to participate, Wenham said. The company eventually received a small loan from a London-based startup lender. The loan came with a high interest rate and was smaller than what the company had sought.

His inability to get a bigger loan delayed the project by years, Wenham said. “We could have been reaping the rewards and benefits so much sooner,” Wenham said.

Dozens of startup lenders have stepped in to fill the void created by the retrenchment of big banks. They provided about half of all new loans to small and midsize businesses last year, government figures show. But they charge high interest rates on business loans, said Mike Conroy, director of commercial finance at UK Finance, the banking industry’s main trade group.

Conroy said the biggest factor behind weak business investment is a lack of demand, not supply. Many entrepreneurs are reluctant to take on debt, or simply don’t aspire to grow, he said. “The U.K. has many small businesses making a great contribution to the U.K. economy and local communities, even though they don’t aspire to be the next Microsoft or Google,” Conroy said.

Research in the U.S. and Australia shows that banks respond to rising home values by shifting capital away from businesses. U.S. banks located in areas with robust housing markets in the early 2000s bubble boosted mortgage lending while cutting business lending, according to a 2018 research paper in the Review of Financial Studies.

In the U.K., rules put in place after the financial crisis force banks to hold higher levels of capital for business loans, which are deemed riskier, than for mortgages.

Matt Hammerstein, CEO of Barclays’s U.K. operations, said banks have increasingly required all borrowers—whether homeowners or businesses—to put up physical assets that the lenders could sell if the borrowers fail to repay. Many business owners refuse to put up their assets, such as homes, as collateral and thus don’t win approval for loans, he said.

“What banks have done over time in order to be able to underpin their risk appetite is to expect entrepreneurs to put more of their own equity at risk,” Hammerstein said. “If you’re lending to a small business, particularly one that has intangible assets, you’re going to want some collateral.”

Default rates among established small and midsize businesses is low—about one in 50 will default in a given year, said Davies of Allica Bank. But determining each company’s risk—and thus what interest rate to charge and how much capital to hold—is less accurate and more time-consuming for big banks, which have instead shifted resources to mortgages.

In 2018, Jurga Zilinskiene wanted financing to develop software to expand her London-based language-translation business, Guildhawk. The 40-employee company translates documents for companies around the globe.

She asked a big U.K. bank for a seven-figure loan; they lent her a fraction of that, citing her lack of tangible assets that could back the loan if she defaulted. Many of her assets are intangible, such as intellectual property.

She worries that banks are too focused on making a quick profit rather than supporting the long-term health of the economy. “How can I compete with global enterprises in the United States, China?” she asks.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Limited to 630 units, Lamborghini’s latest Urus Capsule pushes personalisation further than ever, blending hybrid performance with over 70 bespoke design combinations.

From snow-dusted valleys to festival-filled autumns, Bhutan reveals itself as a rare destination where culture, nature and spirituality unfold year-round.

The lunar flyby would be the deepest humans have traveled in space in decades.

4 min

It’s go time for the highest-stakes mission at NASA in more than 50 years.

On April 1, the agency is set to launch four astronauts around the moon, the deepest human spaceflight since the final Apollo lunar landing in 1972.

The launch window for Artemis II , as the mission is called, opens at 6:24 p.m. ET.

National Aeronautics and Space Administration teams have been preparing the vehicles to depart from Florida’s Kennedy Space Center on the planned roughly 10-day trip. Crew members have trained for years for this moment.

Reid Wiseman, the NASA astronaut serving as mission commander, said he doesn’t fear taking the voyage. A widower, he does worry at times about what he is putting his daughters through.

“I could have a very comfortable life for them,” Wiseman said in an interview last September.

“But I’m also a human, and I see the spirit in their eyes that is burning in my soul too. And so we’ve just got to never stop going.”

Wiseman’s crewmates on Artemis II are NASA’s Victor Glover and Christina Koch, as well as Canadian Space Agency astronaut Jeremy Hansen.

What are the goals for Artemis II?

The biggest one: Safely fly the crew on vehicles that have never carried astronauts before.

The towering Space Launch System rocket has the job of lofting a vehicle called Orion into space and on its way to the moon.

Orion is designed to carry the crew around the moon and back. Myriad systems on the ship—life support, communications, navigation—will be tested with the astronauts on board.

SLS and Orion don’t have much flight experience. The vehicles last flew in 2022, when the agency completed its uncrewed Artemis I mission .

How is the mission expected to unfold?

Artemis II will begin when SLS takes off from a launchpad in Florida with Orion stacked on top of it.

The so-called upper stage of SLS will later separate from the main part of the rocket with Orion attached, and use its engine to set up the latter vehicle for a push to the moon.

After Orion separates from the upper stage, it will conduct what is called a translunar injection—the engine firing that commits Orion to soaring out to the moon. It will fly to the moon over the course of a few days and travel around its far side.

Orion will face a tough return home after speeding through space. As it hits Earth’s atmosphere, Orion will be flying at 25,000 miles an hour and face temperatures of 5,000 degrees as it slows down. The capsule is designed to land under parachutes in the Pacific Ocean, not far from San Diego.

Is it possible Artemis II will be delayed?

Yes.

For safety reasons, the agency won’t launch if certain tough weather conditions roll through the Cape Canaveral, Fla., area. Delays caused by technical problems are possible, too. NASA has other dates identified for the mission if it doesn’t begin April 1.

Who are the astronauts flying on Artemis II?

The crew will be led by Wiseman, a retired Navy pilot who completed military deployments before joining NASA’s astronaut corps. He traveled to the International Space Station in 2014.

Two other astronauts will represent NASA during the mission: Glover, an experienced Navy pilot, and Koch, who began her career as an electrical engineer for the agency and once spent a year at a research station in the South Pole. Both have traveled to the space station before.

Hansen is a military pilot who joined Canada’s astronaut corps in 2009. He will be making his first trip to space.

Koch’s participation in Artemis II will mark the first time a woman has flown beyond orbits near Earth. Glover and Hansen will be the first African-American and non-American astronauts, respectively, to do the same.

What will the astronauts do during the flight?

The astronauts will evaluate how Orion flies, practice emergency procedures and capture images of the far side of the moon for scientific and exploration purposes (they may become the first humans to see parts of the far side of the lunar surface). Health-tracking projects of the astronauts are designed to inform future missions.

Those efforts will play out in Orion’s crew module, which has about two minivans worth of living area.

On board, the astronauts will spend about 30 minutes a day exercising, using a device that allows them to do dead lifts, rowing and more. Sleep will come in eight-hour stretches in hammocks.

There is a custom-made warmer for meals, with beef brisket and veggie quiche on the menu.

Each astronaut is permitted two flavored beverages a day, including coffee. The crew will hold one hourlong shared meal each day.

The Universal Waste Management System—that’s the toilet—uses air flow to pull fluid and solid waste away into containers.

What happens after Artemis II?

Assuming it goes well, NASA will march on to Artemis III, scheduled for next year. During that operation, NASA plans to launch Orion with crew members on board and have the ship practice docking with lunar-lander vehicles that Elon Musk’s SpaceX and Jeff Bezos’ Blue Origin have been developing. The rendezvous operations will occur relatively close to Earth.

NASA hopes that its contractors and the agency itself are ready to attempt one or more lunar landing missions in 2028. Many current and former spaceflight officials are skeptical that timeline is feasible.

As the season turns, Handpicked Wines’ latest Pinot Noir and Chardonnay releases reveal how subtle shifts in place shape what ends up in the glass.

Wealthy Aussies are swapping large family homes for high-end apartments, with sales of prestige units tripling over the past decade.