Why Businesses Can’t Stop Asking for Tips

Employers far beyond restaurants rely on the practice to avoid paying higher wages; testing customer limits

5 min

5 min

American businesses have gotten hooked on tipping.

Tip requests have spread far beyond the restaurants and bars that have long relied on them to supplement employee wages. Juice shops, appliance-repair firms and even plant stores are among the service businesses now asking customers to hand over some extra money to their workers.

“The U.S. economy is more tip-reliant than it’s ever been,” said Scheherezade Rehman, an economist and professor of international finance at George Washington University. “But there’s a growing sense that these requests are getting out of control and that corporate America is dumping the responsibility for employee pay onto the customer.”

Some businesses that are new to tipping said they have turned to the practice to try to retain workers in a competitive job market while also keeping their prices low. Asking for tips allows them to increase worker pay without raising their wages.

Consumers seeing tip prompts at every turn say they are overwhelmed—and that worker wages should be business owners’ responsibility, not theirs.

Sixteen percent of the 517 small businesses surveyed by employee-management software company Homebase for The Wall Street Journal ask customers to leave a tip at checkout, up from 6.2% in 2019.

Payroll company Paychex, which provides software for thousands of businesses in leisure, hospitality, retail and other service industries, said more employees are receiving tips as a portion of their pay than at any time since the company started tracking tipping in 2010. As of May, 6.3% of workers whose employers used the software earned tips, compared with 5.6% in 2020. The number remained relatively flat between 2016 and 2020.

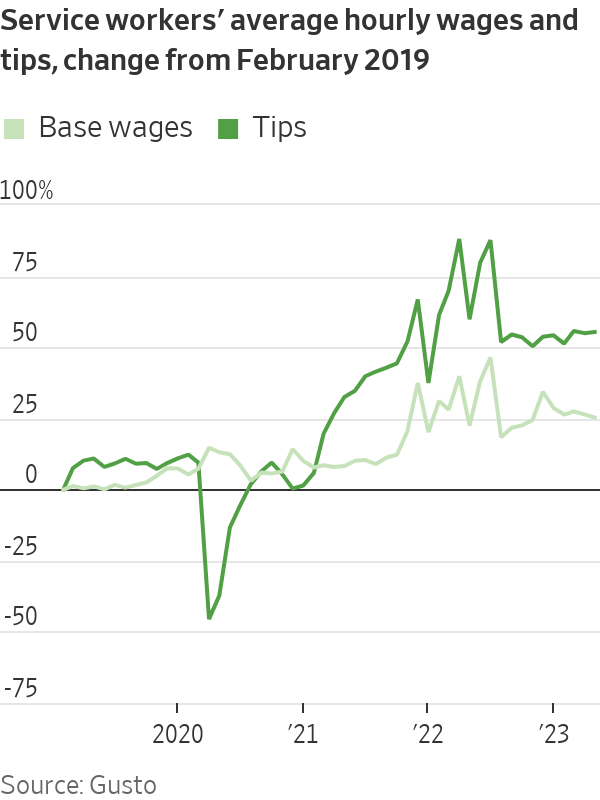

As of June, service-sector workers in non-restaurant leisure and hospitality jobs made $1.35 an hour in tips, on average, up 30% from the $1.04 an hour they made in 2019, according to an analysis of 300,000 small and midsize businesses by payroll provider Gusto.

Tips now increase wages for service workers by an average of 25%, compared with 20% between 2019 and 2020, according to Gusto. In May, the average hourly service-industry worker earned $16.64 an hour in base wages and $4.23 an hour in tips.

During pandemic lockdowns, customers of many service businesses began tipping to acknowledge workers who put themselves at risk. Rehman said that made businesses reliant on the practice. Employers with already tight margins say there’s no going back.

“With businesses still preparing for the possibility of a recession, they don’t want to lock into higher wages,” said Jonathan Morduch, a professor of public policy and economics at New York University. “Tipping gives them more flexibility.” He said the practice pushes the financial risk that employers would ordinarily shoulder onto workers.

“Businesses are happy to let workers earn more from tips, especially when there’s no pressure to raise the tipped minimum,” he said, referring to the $2.13 an hour plus tips many bar and restaurant workers across the country earn.

Holding on to workers has been especially difficult in the services sector, particularly since the pandemic. Lodging and food service have had the highest quit rate for workers since July 2021, consistently above 4.9% per three months, the U.S. Chamber of Commerce said in a May 2023 report. The quit rate for the retail trade industry isn’t far behind, around 3.3% so far in 2023. In May 2023, the overall quit rate for workers was 2.6%, according to the Bureau of Labor Statistics.

Dan Moreno, founder of Miami-based Flamingo Appliance Service, decided in 2020 to add an option for customers to tip his employees, reasoning that his home-repair technicians were taking health risks by entering customers’ homes during the pandemic.

About one-third of customers now leave a tip of between 10% and 20%, Moreno said. The requests add an average of $650 a year to his 182 technicians’ salaries, about 1% of their total yearly income.

Rising costs, he said, persuaded him to retain the option after the pandemic abated.

“You wouldn’t believe the margins we operate with,” he said. Competition for workers is fierce. Were he to eliminate the gratuity prompt, he said, he would have to raise prices beyond the 18% he already has, on average, since 2019—likely costing him clients.

He knows the requests might turn off some customers, but as the son of a repair technician and a former technician himself, he said, he tries to do as much as he can for his workers.

Within the food-service industry, tips as a share of compensation are rising faster at limited-service establishments such as bakeries and coffee shops than at full-service ones, according to Gusto.

At the Main Squeeze Juice Co. in Mandeville, La., tips add $3 to $5 to workers’ hourly pay, which starts at $10. Owner Zachary Cheaney said he added the option when he opened the location in 2020.

“We can’t just say, ‘Oh, we’re going to charge $2 extra’ instead of having tips, because we have a duty to our customers to have a very fair price point,” said Cheaney, who also consults for Main Squeeze’s corporate office. If customers think the price is too high, he said, they won’t return. Asking them to tip, he said, is different because it’s optional.

“If customers completely stopped tipping, we would be forced to pay employees more, and it would be hard on us as business operators in this crazy environment of rising costs,” he said.

The juice bar’s general manager, Tiffany Naquin, said tips make up about one-tenth of her $46,000 annual pay. Workers like tips, she said, “in all industries. It’s that little extra.” Knowing a customer will see a gratuity screen at the end motivates employees, she said. “If you give employees incentives, they are going to give you better work,” she said.

Checkouts that include a tip screen are more awkward for customers than for workers, she said. She understands if someone declines to tip, she said, and she wouldn’t let that affect the quality of service.

Morduch, the New York University economics professor, said that while most people tend to think of tips as steady income, many businesses fluctuate seasonally—which means employee pay goes up and down. Service workers who receive tips, he added, are often lower income and struggle to deal with such volatility.

Saru Jayaraman, a labor advocate and director of the Food Labor Research Center at the University of California, Berkeley, said that boosting tips without increasing base pay is bad for workers. If customers stop tipping, she said, worker pay effectively declines, which it wouldn’t if employees got a raise.

“Employers think they’re being smart by using tipping instead of raising wages,” she said. “But really they’re risking losing staff, because it’s pissing consumers off and the employees are the ones who have to deal with it.”

A May survey of about 2,400 Americans by financial services company Bankrate found that consumers are tipping less often than they did at the height of the pandemic. Forty-one percent of respondents said businesses should pay their employees better rather than rely so much on tips. Roughly a third said tipping culture is out of hand.

Denver retiree Mary Medley, though, said she sees being a generous tipper as part of her economic responsibility. For her, it isn’t about how difficult a task was, but whether she can lighten someone else’s financial burden, even a little.

“It’s not my job to figure out where it goes or how it gets distributed,” she said. “But if they’re giving me the opportunity to participate in supporting a business in a tangible way, I’ll do so.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The Federal Budget may have softened some of its proposed tax reforms, but it has exposed a bigger issue: too many families are relying on wealth structures that no longer reflect the realities of modern life.

3 min

For many Australians, the 2026 Federal Budget initially felt like a direct challenge to the way wealth is created, held and transferred between generations.

The headlines were immediate: changes to capital gains tax, reforms to discretionary trusts, restrictions on negative gearing and increased scrutiny of investment structures. Unsurprisingly, affluent families, business owners and investors began asking the same question:

Is the way we hold our wealth still fit for purpose?

In recent days, the government has announced several significant amendments following industry consultation and public feedback, including exempting testamentary trusts from the proposed 30 per cent minimum tax and expanding capital gains tax concessions for small businesses.

The backdown is welcome. But it also highlights something much bigger.

This Budget has accelerated a conversation that many Australian families have been postponing for years.

The conversation is not really about tax. It is about wealth stewardship.

For decades, Australians have built wealth through businesses, property, investments and careful long-term planning. Yet many families have not revisited the legal structures surrounding those assets in years, sometimes decades.

We often see clients who have spent years building significant wealth, only to discover their legal arrangements no longer reflect their current circumstances.

Their children are now adults. They may own multiple properties.

They may have sold a business, entered a second marriage, become grandparents or accumulated digital assets that did not exist when their original estate plans were prepared.

The trust that distributes income may need to be reconsidered. The bucket company may no longer be so attractive.

The Budget has simply exposed a reality that already existed: wealth structures cannot remain static while life continues to evolve.

Importantly, trusts themselves are not the issue.

Trusts are legitimate planning tools that provide flexibility, protection and continuity. When used appropriately, they allow families to adapt to changing circumstances over time.

And neither is tax the issue, really. Getting the fundamentals right is more important for long-term, sustainable wealth than a few favourable tax treatments around the edges.

The real issue is complacency.

Too often, families create structures and assume the job is done. It isn’t.

Estate planning is no longer a document you sign once and file away in a drawer. It is an ongoing process that should evolve alongside your life.

We are also seeing a broader shift in how Australians define wealth itself. It is no longer just the family home and an investment portfolio.

Modern wealth includes businesses, digital assets, cryptocurrency, intellectual property, frequent flyer points and increasingly complex family arrangements.

At the same time, Australians are living longer than ever before, meaning wealth may need to support multiple generations simultaneously. This creates new responsibilities and new risks.

How do you help your children enter the property market without exposing family wealth to relationship breakdowns?

How do you structure wealth so that it remains a source of opportunity rather than future conflict?

These are the questions families should be asking now.

The recent debate surrounding testamentary trusts also serves as an important reminder that policy decisions can have unintended consequences for vulnerable Australians. It is encouraging that the government has listened to feedback and clarified its position.

But the lesson remains: the wealth landscape is changing.

Increasingly, governments, regulators and tax authorities are paying closer attention to how wealth is held and transferred. That means families cannot afford to adopt a “set-and-forget” approach to their structures.

The families who will be best placed for the future are not necessarily those with the greatest wealth.

They are the families with the greatest clarity. Clarity around ownership, succession and governance. And clarity around how wealth will transition from one generation to the next.

Ultimately, preserving wealth is not about avoiding change.

It is about preparing for it.

Because the greatest risk is not change itself.

It is losing the ability to respond to it.

Anthony Hunt is Co-Founder of Wealth Lawyers and former COO of Westpac Private Bank. He advises business owners, investors and affluent Australian families on wealth protection, succession planning and intergenerational wealth transfer

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

Odd Culture Group brings a new kind of after-dark energy to the CBD, where daiquiris, disco and design collide beneath the city streets.