Fed Raises Rates but Nods to Greater Uncertainty After Banking Stress

Officials voted unanimously to increase their benchmark short-term rate by a quarter percentage point

5 min

5 min")

The Federal Reserve approved another quarter-percentage-point interest-rate increase but signalled that banking-system turmoil might end its rate-rise campaign sooner than seemed likely two weeks ago.

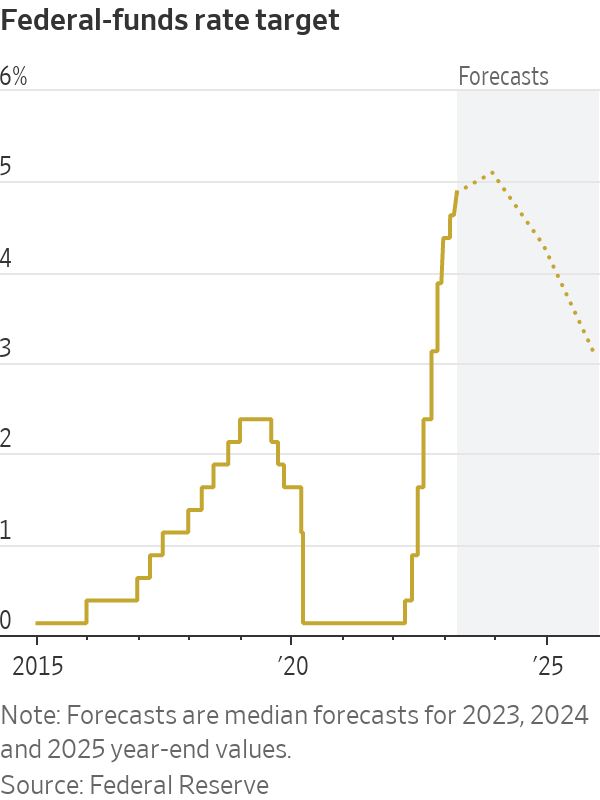

The decision Wednesday marked the Fed’s ninth consecutive rate increase aimed at battling inflation over the past year. It will bring its benchmark federal-funds rate to a range between 4.75% and 5%, the highest level since September 2007.

Officials sent a hint that they might be done raising interest rates soon in their post meeting policy statement. “The committee anticipates that some additional policy firming may be appropriate,” the statement said. Officials dropped a phrase used in their previous eight statements that said the committee anticipated “ongoing increases” in rates would be appropriate.

The policy statement said it was too soon to tell how much recent banking stress would slow the economy. “The U.S. banking system is sound and resilient,” the statement said. “Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain.”

All 11 voters on the rate-setting Federal Open Market Committee agreed to the decision.

New projections showed 17 out of 18 officials who participated in the meeting expect the fed-funds rate to rise to at least 5.1% and to stay there through December, implying one more quarter-point increase. The quarterly projections were little changed from those released in December.

Fed officials have at times over the past year acknowledged the risk of being forced to simultaneously fight two problems—financial instability and inflation. Several have said they would use emergency lending tools, along the lines of those unveiled this month, to stabilise credit markets so they could continue to raise interest rates or hold rates at higher levels to combat inflation.

At a news conference after the decision, Fed Chair Jerome Powell said officials had considered holding rates steady but opted to raise them given signs of still-high inflation and economic activity.

Various estimates of how much the banking stress could slow the economy amount to “guesswork, almost, at this point,” Mr. Powell said. “But we think it’s potentially quite real. And that argues for being alert as we go forward.”

That turmoil offers the strongest evidence yet of spillovers from higher interest rates to the broader economy. The upheaval has served as a stiff reminder of the perils Fed officials, regulators, lawmakers and the White House face trying to corral inflation that soared to a 40-year high last year.

U.S. policy makers cushioned the economic shock created by the Covid-19 pandemic in 2020 and 2021 by providing extensive financial aid and cheap money. Congress and the White House have largely delegated to the Fed the task of taming price pressures.

The fed-funds rate influences other borrowing costs throughout the economy, including rates on mortgages, credit cards and auto loans. The Fed has been raising rates to cool inflation by slowing economic growth. It believes those policy moves work through markets by tightening financial conditions, such as by raising borrowing costs or lowering prices of stocks and other assets.

Two weeks ago, Mr. Powell suggested officials would debate whether to raise rates by a quarter-point or a bigger half-point after reports showed hiring, spending and inflation were stronger early this year than they thought at the time of their Jan. 31-Feb. 1 meeting. “Nothing about the data suggests to me that we’ve tightened too much,” he said on March 7 before the Senate Banking Committee.

An astonishing run on the $200 billion Silicon Valley Bank changed everything. SVB’s depositors were heavily concentrated in the tight knit world of venture capital and startup firms, which were burning cash and withdrawing deposits as the once-highflying technology sector cooled.

On March 8, SVB said it was looking to raise capital from investors and that it would record a loss on longer-dated securities whose values had fallen as interest rates shot up. Nearly a quarter of the bank’s deposits fled over the next day and the bank was taken over by regulators on March 10.

To avoid a broader panic, federal authorities guaranteed the uninsured deposits of the California lender and a second institution, New York’s Signature Bank. The Fed also began offering loans of up to one year to banks on more generous terms as a precaution.

Banking-sector tremors are likely to lead to a pullback in lending because banks will face increased scrutiny from bank examiners and their own management teams to reduce risk taking. Banks could also see earnings squeezed if they feel pressure to raise deposit rates, which could further crimp lending.

That would mean fewer loans to consumers to buy cars, boats, homes and other big-ticket items, and less credit for businesses to hire, expand or invest, raising the risk of a steeper economic downturn.

Banks with fewer than $250 billion in assets account for roughly 50% of U.S. commercial and industrial lending, 60% of residential real estate lending, 80% of commercial real estate lending, and 45% of consumer lending, according to Goldman Sachs.

“I think we’re looking at a sizeable credit crunch,” said Daleep Singh, a former executive at the New York Fed who is now chief global economist at PGIM Fixed Income.

Since officials’ previous meeting, the economy had shown surprising strength, leading to concerns that aggressive rate rises over the previous year hadn’t done enough to slow the economy and lower inflation. Central bankers are concerned that prices will keep rising rapidly if consumers and businesses expect them to.

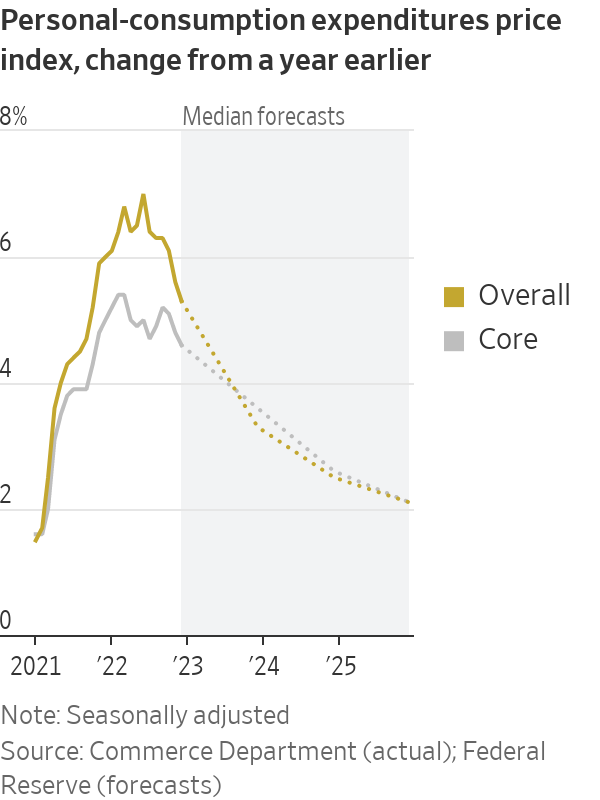

Inflation fell to 4.7% in January from 5.2% in September, as measured by the 12-month change in the personal-consumption expenditures price index excluding food and energy, the Fed’s preferred gauge. Economists expect the government to report next week that the inflation rate was unchanged in February.

Banking stress had led to questions in the past week over whether the Fed would even raise rates at all.

Some analysts fretted that a timeout on rate rises would risk so-called financial dominance, in which monetary policy becomes overly focused on avoiding market stress to the detriment of fighting inflation. A big market rally, in which stock prices rise and borrowing costs fall, could spur more demand and fan price pressures.

“They’d like to avoid that,” said William English, a former senior Fed economist who is a professor at Yale School of Management.

Others said the Fed would have been hard-pressed not to raise interest rates given recent strength in the economy and aggressive measures taken to shore up confidence in the banking system.

“Right now pausing would cause disruption,” said Donald Kohn, a former Fed vice chair. Deciding against raising rates would “signal that they don’t have confidence in their financial stability tools.”

Jan Hatzius, chief economist at Goldman Sachs, disagreed. It would have been better for the Fed to move cautiously given the highly uncertain environment that resulted from the banking stress, he said. “If more issues crop up after Wednesday, that’s also not going to be very confidence inspiring,” he said.

Fed officials have tried to signal their interest-rate moves deliberately over the past year to avoid the kind of market turmoil set off in 1994, when the Fed doubled its short-term benchmark rate from 3% to 6% in a 12-month span.

That rapid tightening hammered stocks and bonds and indirectly contributed to the demise of Kidder Peabody & Co., the bankruptcy of Orange County, Calif., and Mexico’s peso devaluation, which required a bailout from the U.S. and the International Monetary Fund.

After skipping on a rate increase in December 1994, as the peso crisis intensified, the Fed made a final rate increase in early 1995.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The Federal Budget may have softened some of its proposed tax reforms, but it has exposed a bigger issue: too many families are relying on wealth structures that no longer reflect the realities of modern life.

3 min

For many Australians, the 2026 Federal Budget initially felt like a direct challenge to the way wealth is created, held and transferred between generations.

The headlines were immediate: changes to capital gains tax, reforms to discretionary trusts, restrictions on negative gearing and increased scrutiny of investment structures. Unsurprisingly, affluent families, business owners and investors began asking the same question:

Is the way we hold our wealth still fit for purpose?

In recent days, the government has announced several significant amendments following industry consultation and public feedback, including exempting testamentary trusts from the proposed 30 per cent minimum tax and expanding capital gains tax concessions for small businesses.

The backdown is welcome. But it also highlights something much bigger.

This Budget has accelerated a conversation that many Australian families have been postponing for years.

The conversation is not really about tax. It is about wealth stewardship.

For decades, Australians have built wealth through businesses, property, investments and careful long-term planning. Yet many families have not revisited the legal structures surrounding those assets in years, sometimes decades.

We often see clients who have spent years building significant wealth, only to discover their legal arrangements no longer reflect their current circumstances.

Their children are now adults. They may own multiple properties.

They may have sold a business, entered a second marriage, become grandparents or accumulated digital assets that did not exist when their original estate plans were prepared.

The trust that distributes income may need to be reconsidered. The bucket company may no longer be so attractive.

The Budget has simply exposed a reality that already existed: wealth structures cannot remain static while life continues to evolve.

Importantly, trusts themselves are not the issue.

Trusts are legitimate planning tools that provide flexibility, protection and continuity. When used appropriately, they allow families to adapt to changing circumstances over time.

And neither is tax the issue, really. Getting the fundamentals right is more important for long-term, sustainable wealth than a few favourable tax treatments around the edges.

The real issue is complacency.

Too often, families create structures and assume the job is done. It isn’t.

Estate planning is no longer a document you sign once and file away in a drawer. It is an ongoing process that should evolve alongside your life.

We are also seeing a broader shift in how Australians define wealth itself. It is no longer just the family home and an investment portfolio.

Modern wealth includes businesses, digital assets, cryptocurrency, intellectual property, frequent flyer points and increasingly complex family arrangements.

At the same time, Australians are living longer than ever before, meaning wealth may need to support multiple generations simultaneously. This creates new responsibilities and new risks.

How do you help your children enter the property market without exposing family wealth to relationship breakdowns?

How do you structure wealth so that it remains a source of opportunity rather than future conflict?

These are the questions families should be asking now.

The recent debate surrounding testamentary trusts also serves as an important reminder that policy decisions can have unintended consequences for vulnerable Australians. It is encouraging that the government has listened to feedback and clarified its position.

But the lesson remains: the wealth landscape is changing.

Increasingly, governments, regulators and tax authorities are paying closer attention to how wealth is held and transferred. That means families cannot afford to adopt a “set-and-forget” approach to their structures.

The families who will be best placed for the future are not necessarily those with the greatest wealth.

They are the families with the greatest clarity. Clarity around ownership, succession and governance. And clarity around how wealth will transition from one generation to the next.

Ultimately, preserving wealth is not about avoiding change.

It is about preparing for it.

Because the greatest risk is not change itself.

It is losing the ability to respond to it.

Anthony Hunt is Co-Founder of Wealth Lawyers and former COO of Westpac Private Bank. He advises business owners, investors and affluent Australian families on wealth protection, succession planning and intergenerational wealth transfer

Rising rates, construction inflation and shrinking investor confidence are pushing Australia deeper into a dangerous housing spiral that monetary policy alone cannot fix.

French luxury-goods giant’s results are a sign that shoppers weren’t splurging on its collections of high-end garments in the run-up to the holiday season.