Secondhand Sellers Are Going Premium

The RealReal and ThredUp have gone upscale to improve profitability—a challenge in tougher economic times

2 min

2 min

In theory, a weakening economic environment seems good for secondhand platforms: People are more likely to sell valuable items from their closets while bargain hunters emerge. In practice, it is a bit more complicated.

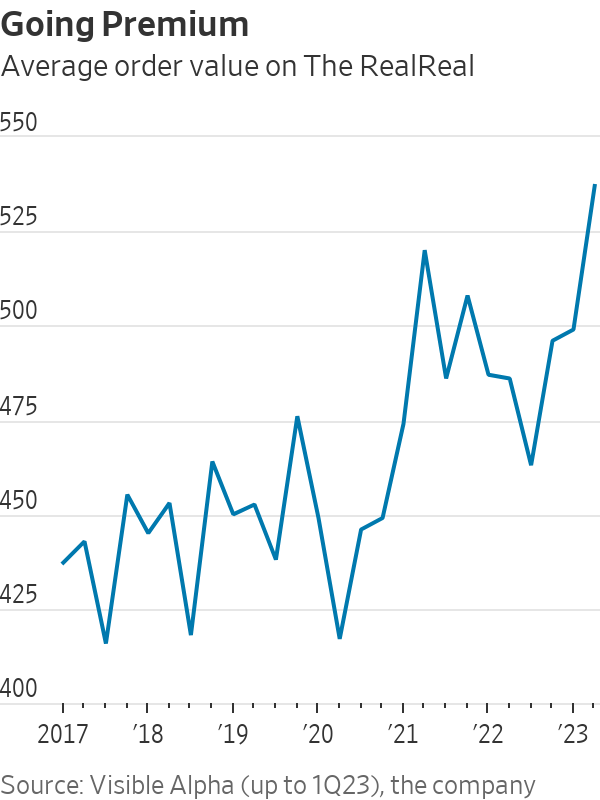

The RealReal, an online marketplace for luxury resale, said on Tuesday that gross merchandise value—the total value of goods sold through its platform—fell 7% in its second quarter, worse than the 5.7% decline that Wall Street analysts were penciling in. ThredUp, which sells more generic brands, fared better and reported revenue growth of 8%, exceeding expectations. Both companies reported narrower net losses than analyst expectations, sending The RealReal up 6% in after-hours trading and ThredUp by 2.8%.

Despite better-than-expected profits, the selling environment isn’t exactly hospitable for either platform.

ThredUp, which tries to keep its pricing 60% to 70% lower than what consumers could buy at regular retail, is facing a very promotional environment in which brands are offering steep discounts on new products. On the company’s earnings call on Tuesday, ThredUp said the market for selling clothes remains competitive, though it is improving.

Meanwhile, demand for luxury goods has generally been lukewarm in the U.S. Even the prices of highly coveted secondhand watches such as Rolexes have fizzled recently. ThredUp is projecting a slowdown in top-line growth this year compared with 2022, while The RealReal is expecting a slight decline in sales volume.

Both platforms are trying to attract wealthier, more resilient customers by upgrading their product mixes, even if it reduces their customer base in the near term. ThredUp said the budget shopper continues to look more challenged and said it is focused on attracting the “incrementally more premium buyer.”

The RealReal, meanwhile, has tweaked its commission structure for consignors by allowing them to retain more of the revenue earned from the sale of the most expensive, in-demand items while reducing incentives on products selling for less than $100. While that has reduced the company’s sales volume, it helped improve gross margins to 65.9% last quarter, up about 9 percentage points from a year earlier.

The tricky part for both platforms is that they haven’t been around long enough to know how their target buyers and sellers behave during downturns. Given that both businesses are, to some extent, supply constrained, further weakness could be a good thing if it encourages more people to raid their wardrobes. And, judging by the strong record at off-price retail during downturns, demand for value products should hold up.

So far, though, a weakening economic environment hasn’t been a bonanza for secondhand goods.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

A long-standing cultural cruise and a new expedition-style offering will soon operate side by side in French Polynesia.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.