Underwhelming Chinese Stock Markets Show Concern Over Recovery

China’s stocks have underperformed this year as questions linger on durability of economic rebound

2 min

2 min

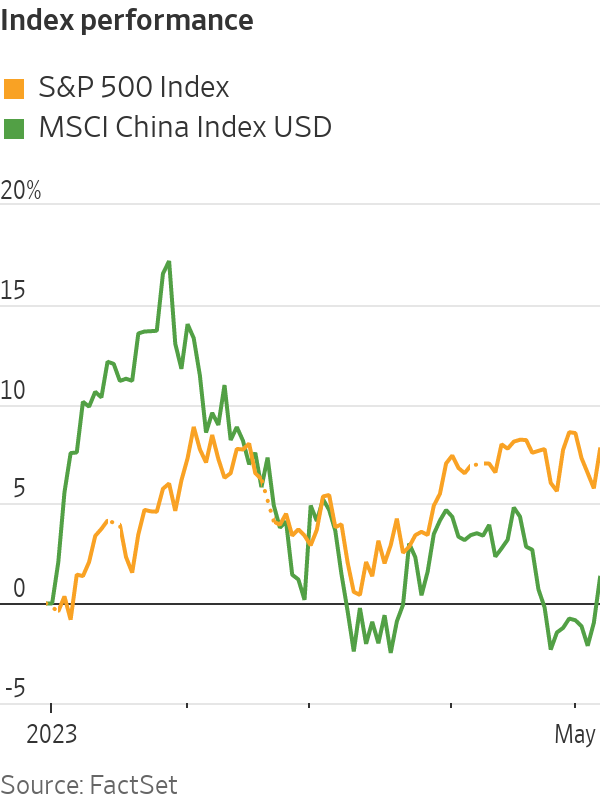

One mystery in global markets this year is that while China’s economy appears to be rebounding strongly, its stock market hasn’t been doing as well.

The MSCI China index has risen only 1.8% so far this year, underperforming many of the major markets. The S&P 500 index, for example, has gained 7.7%. Stocks listed in Shanghai and Shenzhen have done a bit better—the CSI 300 index has gone up 4.9% in 2023. That seems to be in contrast to the rebounding economy, after China scrapped its strict “zero-Covid” pandemic restrictions in December and scaled back its regulatory crackdown on its technology companies.

China’s gross domestic product grew 4.5% from a year earlier in the first quarter and, more significantly, consumption has also come back strongly: retail sales jumped more than 10% in March from a year earlier. Crowds were everywhere in Chinese scenic spots in the recent five-day “Golden Week” holiday. Total domestic trips during the holiday rose 19% from the same period in 2019, according to official figures. Tourism revenue also recovered to pre pandemic levels.

Of course, the rally in Chinese stocks late last year already priced in a big part of the recovery. The MSCI China index surged 34% in the last two months in 2022, after rumours of reopening started to circulate.

Yet earnings growth so far has been disappointing. For nearly 80% of Chinese listed companies that have reported their first-quarter results, profits only grew an average 1% year on year, with around 69% of them having missed consensus earnings estimates, according to Goldman Sachs. About 77% of A-share shares—companies listed in Shanghai and Shenzhen—revised down their earnings guidance for 2023, according to Bank of America.

Earnings growth will likely improve ahead, especially against a lower base last year, when lockdowns across the country battered the economy. The struggling housing sector also seems to have stabilised. But a big question that remains is how long the consumption bounce could last. The export sector may suffer with a potential recession looming in the U.S. and Europe. China’s job market, especially for younger workers, is still quite weak. That partly explains why investors have jumped back into shares of state-owned enterprises—a more stable choice in an uncertain time.

Chinese stocks have rebounded substantially from their lows last year, but are still way off their peaks in early 2021, when China appeared to have avoided the worst of the pandemic. A more sustained market recovery would require a more broad-based revival of earnings growth.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

The pandemic-fuelled love affair with casual footwear is fading, with Bank of America warning the downturn shows no sign of easing.

A divide has opened in the tech job market between those with artificial-intelligence skills and everyone else.