A Killer Golf Swing Is a Hot Job Skill Now

Companies are eager to hire strong players who use hybrid work schedules to schmooze clients on the course

5 min

5 min")

Standout golfers who aren’t quite PGA Tour material now have somewhere else to play professionally: Corporate America.

People who can smash 300-yard drives and sink birdie putts are sought-after hires in finance, consulting, sales and other industries, recruiters say. In the hybrid work era, the business golf outing is back in a big way.

Executive recruiter Shawn Cole says he gets so many requests to find ace golfers that he records candidates’ handicaps, an index based on average number of strokes over par, in the information packets he submits to clients. Golf alone can’t get you a plum job, he says—but not playing could cost you one.

“I know a guy that literally flies around the world in a private jet loaded with French wine, and he golfs and lands hundred-million-dollar deals,” Cole says.

Tee times and networking sessions have long gone hand-in-golf-glove. Despite criticism that doing business on the course undermines diversity, equity and inclusion efforts—and the fact that golf clubs haven’t always been open to women and minorities —people who mix golf and work say the outings are one of the last reprieves from 30-minute calendar blocks

Stars like Tiger Woods and Michelle Wie West helped expand participation in the sport. Still, just 22% of golfers are nonwhite and 26% are women, according to the National Golf Foundation.

To lure more people, clubs have relaxed rules against mobile-phone use on the course, embracing white-collar professionals who want to entertain clients on the links without disconnecting from the office. It’s no longer taboo to check email from your cart or take a quick call at the halfway turn.

With so much other business conducted virtually, shaking hands on the green and schmoozing over clubhouse beers is now seen as making an extra effort, not slacking off.

Americans played a record 531 million rounds last year. Weekday play has nearly doubled since 2019, with much of the action during business hours , according to research by Stanford University economist Nicholas Bloom .

“It would’ve been scandalous in 2019 to be having multiple meetings a week on the golf course,” Bloom says. “In 2024, if you’re producing results, no one’s going to see anything wrong with it.”

A financial adviser at a major Wall Street bank who competes on the amateur circuit told me he completes 90% of his tasks by 10 a.m. because he manages long-term investment plans that change infrequently. The rest of his workday often involves golfing with clients and prospects. He’s a member of a private club with a multiyear waiting list, and people jump at the chance to join him on a course they normally can’t access.

There is an art to bringing in business this way. He never initiates shoptalk, telling his playing partners the round is about having fun and getting to know each other. They can’t resist asking about investment strategies by the back nine, he says.

Work hard, play hard

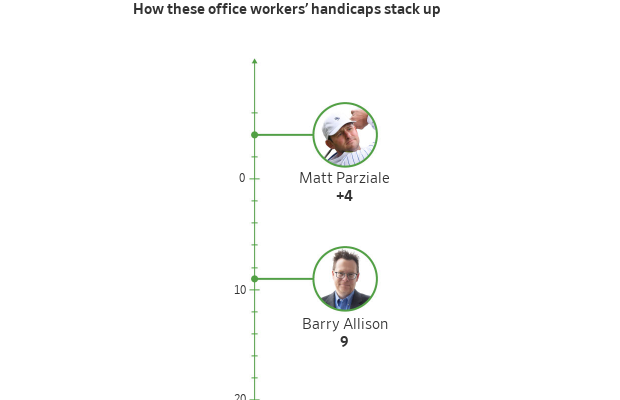

Matt Parziale golfed professionally on minor-league tours for several years, but when his dream of making the big time ended, he had to get a regular job. He became a firefighter, like his dad.

A few years later he won one of the biggest amateur tournaments in the country, earning spots in the 2018 Masters and U.S. Open, where he tied for first among non-pros.

The brush with celebrity brought introductions to business types that Parziale, 35 years old, says he wouldn’t have met otherwise. One connection led to a job with a large insurance broker. In 2022 he jumped to Deland, Gibson Insurance Associates in Wellesley, Mass., which recognised his golf game as a tool to help win large accounts.

He rescheduled our interview because he was hosting clients at a private club on Cape Cod, and squeezed me in the next morning, before teeing off with a business group in Newport, R.I.

A short time ago, Parziale couldn’t imagine making a living this way. Now he’s the norm in elite amateur golf circles.

“I look around at the guys at the events I play, and they all have these jobs ,” he says.

His boss, Chief Executive Chip Gibson, says Parziale is good at bringing in business because he puts as much effort into building relationships as honing his game. A golf outing is merely an opportunity to build trust that can eventually lead to a deal, and it’s a misconception that people who golf during work hours don’t work hard, he says.

Barry Allison’s single-digit handicap is an asset in his role as a management consultant at Accenture , where he specialises in travel and hospitality. He splits time between Washington, D.C., and The Villages, Fla., a golf mecca that boasts more than 50 courses.

It can be hard to get to know people in distributed work environments, he says. Go golfing and you’ll learn a lot about someone’s temperament—especially after a bad shot.

“If you see a guy snap a club over his knee, you don’t know what he’s going to snap next,” Allison says.

Special access

On a recent afternoon I was a lunch guest at Brae Burn Country Club, a private enclave outside Boston that was the site of U.S. Golf Association championships won by legends like Walter Hagen and Bobby Jones. I parked in the second lot because the first one was full—on a Wednesday.

My host was Cullen Onstott, managing director of the Onstott Group executive search firm and a former collegiate golfer at Fairfield University. He explained one reason companies prize excellent golfers is they can put well-practiced swings on autopilot and devote most of their attention to chitchat.

It’s hard to talk with potential customers about their needs and interests when you’re hunting for errant shots in the woods. It’s also challenging if you show off.

The first hole at Brae Burn is a 318-yard par 4 that slopes down, enabling big hitters like Onstott to reach the putting green in a single stroke. But to stay close to his playing partners and keep the conversation flowing, he sometimes hits a shorter shot.

Having an “in” at an exclusive club can make you a catch. Bo Burch, an executive recruiter in North Carolina, says clubs in his region tend to attract members according to their business sectors. One might be chock-full of real-estate investors while another has potential buyers of industrial manufacturing equipment.

Burch looks for candidates who are members of clubs that align with his clients’ industries, though he stresses that business acumen comes first when filling positions.

Tami McQueen, a former Division I tennis player and current chief marketing officer at Atlanta investment firm BIP Capital, signed up for private golf lessons this year. She had noticed colleagues were wearing polos with course logos and bringing their clubs to work. She wanted in.

McQueen joined business associates on the golf course for the first time in March at the PGA National Resort in Palm Beach Gardens, Fla. She has lowered her handicap to a respectable 26 and says her new skill lends a professional edge.

“To be able to say, ‘I can play with you and we can have those business meetings on the course’ definitely opens a lot more doors,” she says.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

BMW has unveiled the Neue Klasse in Munich, marking its biggest investment to date and a new era of electrification, digitalisation and sustainable design.