America’s Billionaires Love Japanese Stocks. Why Don’t the Japanese?

Japan’s government wants cash-hoarding households to invest more

3 min

3 min

TOKYO—Japan’s government is on a mission to make buying stocks hot again.

Many of America’s biggest investors are bullish on Japan. Warren Buffett shared that he increased his investments in Japanese companies during an April visit to the country. Ken Griffin is preparing to reopen an office in Tokyo for his hedge fund, Citadel, and investment banks Goldman Sachs and Morgan Stanley have issued optimistic outlooks for Japan’s stock market.

Japan’s problem is this: There are few signs its estimated 125 million residents share in the excitement.

Burned by dismal returns since the bursting of Japan’s asset bubble in the late 1980s and early 1990s, generations of families here have stashed most of their money in low-yielding savings accounts rather than trying to increase their wealth through the stock market.

Japanese households put an average of just 11% of their savings into stocks and 54% in cash and bank deposits, according to Bank of Japan data released last month. That trails well behind the U.S., where households have about 39% of their money tied up in the market and only 13% in cash and bank deposits, according to Federal Reserve data.

Haruyo Arai, a 62-year-old office worker, began investing in the stock market just last month.

“I was brought up by parents who would say, ‘Don’t dabble in stocks,’ ” she said.

Japanese Prime Minister Fumio Kishida has pledged to double households’ asset incomes, in part by encouraging people to invest in risky assets like stocks. The government is raising caps for Japan’s tax-exempt investment system for small investors, the Nippon Individual Savings Account, with changes set to take effect in January. The Tokyo Stock Exchange has been urging companies to boost their valuations and increase shareholder returns.

Arai cited the upcoming expansion to NISA, along with a desire to save more money for the future, as some of the reasons she decided to begin taking investing more seriously. She has been taking weekend classes at Tokyo-based Financial Academy to learn more about stocks and waking up early every morning to watch a TV news program focused on the economy.

Some believe investors like Arai will prove to be the exception, not the rule. Stocks here haven’t hit a record in decades. There isn’t much buzz among ordinary people about investing in Japanese markets.

“I’ve got the impression that Japanese people don’t really think positively about the desire to make money,” said Takashi Kawaguchi, a 48-year-old office worker who, like Arai, has been learning about investing at Financial Academy.

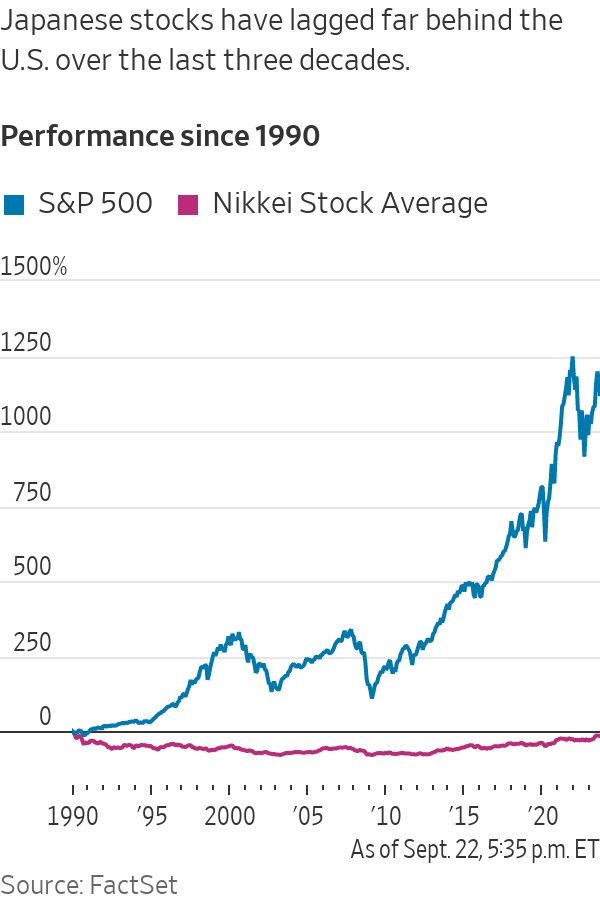

While the 2023 rally has helped lift Japanese stock indexes to 33-year highs, long-term returns pale in comparison to what an investor would have gotten by investing in U.S. stocks. The Nikkei closed at 32,402 on Friday, still 17% below its record hit in 1989. The S&P 500 has grown more than twelvefold over that time. That has made many investors here turn to foreign markets instead of focusing their bets within Japan.

“The Nikkei might hit 40,000, god knows when,” said Heihachiro “Hutch” Okamoto, foreign equity consultant at retail brokerage Monex. “But most of our investors prefer U.S. stocks.”

To Okamoto’s point, the most popular names traded on Monex daily aren’t Japanese stock indexes like the Topix or Nikkei, brand-name companies like Sony or even the “sogo shosha”—the trading houses that Buffett has invested in. Instead, they are all American names: companies like Nvidia, Tesla, Apple and Amazon.com, as well as funds tracking the S&P 500 and the Nasdaq-100.

And that is just among those interested in investing in the first place. While in past years, everyday investors in Japan made a name for themselves with their forays into the foreign exchange market, the overall trading culture here has been one of hesitation.

“Most people here think investing is very risky,” said Hidekazu Ishida, a special adviser at FinCity.Tokyo, which works with the government and the financial industry to try to boost investment in Tokyo. Being into finance comes off as “kakkowarui,” he added, referencing a word for uncool.

Even some heads of companies are lukewarm about the idea of encouraging more individual investors to buy Japanese stocks.

“I’m neutral about that,” said Takeshi Niinami, chief executive officer of whisky and beverage giant Suntory, when asked if he thought it would be a good idea for more Japanese people to invest in the market. Stock investing is risky, he said. And many Japanese people remain wary of participating in the market, because of the severity of prior downturns.

“I think perhaps increasing interest rates is better for people,” he said.

—Chieko Tsuneoka and Alastair Gale contributed to this article

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

The megamansion was built for Tony Pritzker, heir to the Hyatt Hotel fortune and brother of Illinois Gov. JB Pritzker.

Powerhouse real estate couple Avi Khan and Kaylea Sayer welcome their daughter while balancing record-breaking careers, proving success and family can grow side by side.