Corporate Layoffs Spread Beyond High-Growth Tech Giants

Dow, IBM and SAP say they will lay off thousands of workers as belt-tightening becomes the new business priority

4 min

4 min

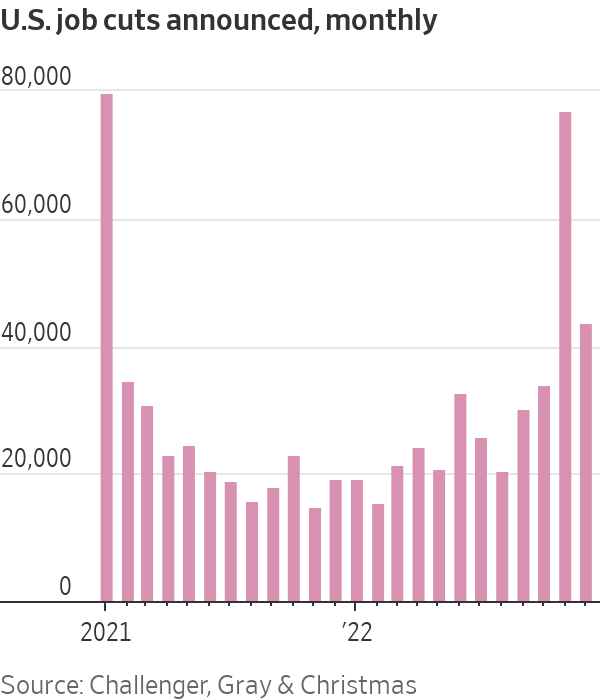

Dow Inc., International Business Machines Corp. and SAP SE announced plans to cut thousands of jobs to prepare for a darkening economic outlook, as the current wave of corporate layoffs spreads beyond high-growth technology companies.

Together with layoffs announced by manufacturer 3M Co. this week, these companies are trimming more than 10,000 jobs, just a fraction of their total workforces. Still, the decisions mark a shift in sentiment inside executive suites, where many leaders have been holding on to workers after struggling to hire and retain them in recent years when the pandemic disrupted workplaces.

Unlike Microsoft Corp. and Google parent Alphabet Inc., which announced larger layoffs this month, these companies haven’t expanded their workforces dramatically during the pandemic. Instead, the leaders of these global giants said they were shrinking to adjust to slowing growth, or responding to weaker demand for their products.

“We are taking these actions to further optimise our cost structure,” Jim Fitterling, Dow chief executive, said in announcing the cuts, noting the company was navigating “macro uncertainties and challenging energy markets, particularly in Europe.”

The U.S. job market remains historically tight, with unemployment in December at 3.5% matching multi decade lows. The number of job openings still far outpaces the number of people looking for work. The Federal Reserve has been raising interest rates to tame growth and combat high inflation. But CEOs say many companies are beginning to scrutinise hiring more closely.

Slower hiring has already lengthened the time it takes Americans to land a new job. In December, 826,000 unemployed workers had been out of a job for about 3½ to 6 months, up from 526,000 in April 2022, according to the Labor Department.

“Employers are hovering with their feet above the brake. They’re more cautious. They’re more precise in their hiring,” said Jonas Prising, chief executive of ManpowerGroup Inc., a provider of temporary workers. “But they’ve not stopped hiring.”

Additional signs of a cooling economy emerged on Thursday when the Commerce Department said U.S. gross domestic product growth slowed to a 2.9% annual rate in the fourth quarter, down from a 3.2% annual rate in the third quarter.

Not all companies are in layoff mode. Walmart Inc., the country’s biggest private employer, said this week it was raising its starting wages for hourly U.S. workers to $14 from $12, amid a still tight job market for front line workers. Chipotle Mexican Grill Inc. said Thursday it plans to hire 15,000 new employees to work in its restaurants, while plane maker Airbus SE said it is recruiting over 13,000 new staffers this year. Airbus said 9,000 of the new jobs would be based in Europe with the rest spread among the U.S., China and elsewhere.

General Electric Co., which slashed thousands of aerospace workers in 2020 and is currently laying off 2,000 workers from its wind turbine business, is hiring in other areas. “If you know any welders or machinists, send them my way,” Chief Executive Larry Culp said this week.

Annette Clayton, CEO of North American operations at Schneider Electric SE, a Europe-headquartered energy-management and automation company, said the U.S. needs far more electricians to install electric-vehicle chargers and perform other tasks. “The shortage of electricians is very, very important for us,” she said.

Railroad CSX Corp. told investors on Wednesday that after sustained effort, it had reached its goal of about 7,000 train and engine employees around the beginning of the year, but plans to hire several hundred more people in those roles to serve as a cushion and to accommodate attrition that remains higher than the company would like.

Freeport-McMoRan Inc. executives said Wednesday they expect U.S. labor shortages to continue to crimp production at the mining giant. The company has about 1,300 job openings in a U.S. workforce of about 10,000 to 12,000, and many of its domestic workers are new and need training and experience to match prior expertise, President Kathleen Quirk told analysts.

“We could have in 2022 produced more if we were fully staffed, and I believe that is the case again this year,” Ms. Quirk said.

The latest layoffs are modest relative to the size of these companies. For example, IBM’s plan to eliminate about 3,900 roles would amount to a 1.4% reduction in its head count of 280,000, according to its latest annual report.

The planned 3,000 job cuts at SAP affect about 2.5% of the business-software maker’s global workforce. Finance chief Luka Mucic said the job cuts would be spread across the company’s geographic footprint, with most of them happening outside its home base in Germany. “The purpose is to further focus on strategic growth areas,” Mr. Mucic said. The company employed around 111,015 people on average last year.

Chemicals giant Dow said on Thursday it was trimming about 2,000 employees. The Midland, Mich., company said it currently employs about 37,800 people. Executives said they were targeting $1 billion in cost cuts this year and shutting down some assets to align spending with the macroeconomic environment.

3M, which had about 95,000 employees at the end of 2021, cited weakening consumer demand for its plans to eliminate 2,500 manufacturing jobs. The maker of Scotch tape, Post-it Notes and thousands of other industrial and consumer products said it expects lower sales and profit in 2023.

“We’re looking at everything that we do as we manage through the challenges that we’re facing in the end markets,” 3M Chief Executive Mike Roman said during an earnings conference call. “We expect the demand trends we saw in December to extend through the first half of 2023.”

Some companies still hiring now say the job cuts across the economy are making it easier to find qualified candidates. “We’ve got the pick of the litter,” said Bill McDermott, CEO of business-software provider ServiceNow Inc. “We have so many applicants.”

At Honeywell International Inc., CEO Darius Adamczyk said the job market remains competitive. With the layoffs in technology, though, Mr. Adamczyk said he anticipated that the labor market would likely soften, potentially also expanding the applicants Honeywell could attract.

“We’re probably going to be even more selective than we were before because we’re going to have a broader pool to draw from,” he said.

Across the corporate sphere, many of the layoffs happening now are still small relative to the size of the organisations, said Denis Machuel, CEO of global staffing firm Adecco Group AG.

“I would qualify it more as a recalibration of the workforce than deep cuts,” Mr. Machuel said. “They are adjusting, but they are not cutting the muscle.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The Federal Budget may have softened some of its proposed tax reforms, but it has exposed a bigger issue: too many families are relying on wealth structures that no longer reflect the realities of modern life.

3 min

For many Australians, the 2026 Federal Budget initially felt like a direct challenge to the way wealth is created, held and transferred between generations.

The headlines were immediate: changes to capital gains tax, reforms to discretionary trusts, restrictions on negative gearing and increased scrutiny of investment structures. Unsurprisingly, affluent families, business owners and investors began asking the same question:

Is the way we hold our wealth still fit for purpose?

In recent days, the government has announced several significant amendments following industry consultation and public feedback, including exempting testamentary trusts from the proposed 30 per cent minimum tax and expanding capital gains tax concessions for small businesses.

The backdown is welcome. But it also highlights something much bigger.

This Budget has accelerated a conversation that many Australian families have been postponing for years.

The conversation is not really about tax. It is about wealth stewardship.

For decades, Australians have built wealth through businesses, property, investments and careful long-term planning. Yet many families have not revisited the legal structures surrounding those assets in years, sometimes decades.

We often see clients who have spent years building significant wealth, only to discover their legal arrangements no longer reflect their current circumstances.

Their children are now adults. They may own multiple properties.

They may have sold a business, entered a second marriage, become grandparents or accumulated digital assets that did not exist when their original estate plans were prepared.

The trust that distributes income may need to be reconsidered. The bucket company may no longer be so attractive.

The Budget has simply exposed a reality that already existed: wealth structures cannot remain static while life continues to evolve.

Importantly, trusts themselves are not the issue.

Trusts are legitimate planning tools that provide flexibility, protection and continuity. When used appropriately, they allow families to adapt to changing circumstances over time.

And neither is tax the issue, really. Getting the fundamentals right is more important for long-term, sustainable wealth than a few favourable tax treatments around the edges.

The real issue is complacency.

Too often, families create structures and assume the job is done. It isn’t.

Estate planning is no longer a document you sign once and file away in a drawer. It is an ongoing process that should evolve alongside your life.

We are also seeing a broader shift in how Australians define wealth itself. It is no longer just the family home and an investment portfolio.

Modern wealth includes businesses, digital assets, cryptocurrency, intellectual property, frequent flyer points and increasingly complex family arrangements.

At the same time, Australians are living longer than ever before, meaning wealth may need to support multiple generations simultaneously. This creates new responsibilities and new risks.

How do you help your children enter the property market without exposing family wealth to relationship breakdowns?

How do you structure wealth so that it remains a source of opportunity rather than future conflict?

These are the questions families should be asking now.

The recent debate surrounding testamentary trusts also serves as an important reminder that policy decisions can have unintended consequences for vulnerable Australians. It is encouraging that the government has listened to feedback and clarified its position.

But the lesson remains: the wealth landscape is changing.

Increasingly, governments, regulators and tax authorities are paying closer attention to how wealth is held and transferred. That means families cannot afford to adopt a “set-and-forget” approach to their structures.

The families who will be best placed for the future are not necessarily those with the greatest wealth.

They are the families with the greatest clarity. Clarity around ownership, succession and governance. And clarity around how wealth will transition from one generation to the next.

Ultimately, preserving wealth is not about avoiding change.

It is about preparing for it.

Because the greatest risk is not change itself.

It is losing the ability to respond to it.

Anthony Hunt is Co-Founder of Wealth Lawyers and former COO of Westpac Private Bank. He advises business owners, investors and affluent Australian families on wealth protection, succession planning and intergenerational wealth transfer

A bold new era for Australian luxury: MAISON de SABRÉ launches The Palais, a flagship handbag eight years in the making.

A luxury lifestyle might cost more than it used to, but how does it compare with cities around the world?