Fed Approves Quarter-Point Rate Hike, Signals More Increases Likely

Officials are slowing interest-rate increases as they debate when to pause

4 min

4 min

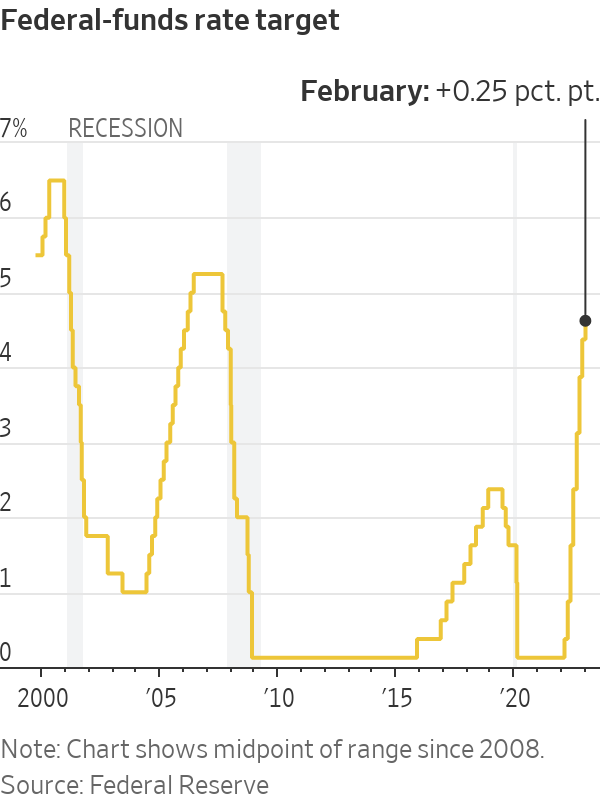

WASHINGTON—The Federal Reserve approved an interest-rate increase of a quarter-percentage-point and signalled plans to raise rates again next month to continue lowering inflation.

The decision Wednesday followed six consecutive rate rises that were larger, including an increase of a half-point in December and a 0.75-point increase in November.

Officials nodded to recent improvement in inflation readings but didn’t significantly alter their guidance in a policy statement released after the meeting regarding coming rate moves.

“The committee anticipates that ongoing increases” in interest rates “will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive,” said the statement, using the same language included in policy statements since last March.

The latest increase caps a year in which the Fed lifted its benchmark federal-funds rate from near zero to a range between 4.5% and 4.75%, a level last reached in 2007. That extends the central bank’s most rapid pace of rate increases since the early 1980s to fight inflation, which hit a 40-year high last year.

One big question heading into Wednesday’s meeting was the extent to which recent economic data had given Fed officials more confidence that inflation and wage pressures had peaked.

In December, most of them penciled in raising the fed-funds rate to a range between 5% and 5.25% this year. After the hike they approved Wednesday, that projection would imply additional quarter-point increases at the Fed’s meetings in March and May, followed by a pause in rate rises.

Many officials had repeated in recent weeks that they still saw such a rate path as appropriate given strong wage pressures, a tight labour market and high service-sector inflation. But officials also said they would base their decisions on how the economy performs in the coming months.

“We can now say for the first time, the disinflationary process has started,” said Fed Chair Jerome Powell at a news conference after Wednesday’s meeting. But he added, “The job is not fully done.”

Mr. Powell said the central bank was trying to manage the risk of raising rates too much and causing unnecessary economic harm with that of not doing enough to bring down inflation. In repeating his longstanding view that the latter mistake would be harder to fix, Mr. Powell said he didn’t want to be in a position where six or 12 months from now, after a halt to raising rates, the Fed would belatedly conclude that it hadn’t done enough to bring down inflation this year and would have to raise rates higher.

“We’re going to be cautious about declaring victory and sending signals that we think the game is won,” he said. “Certainty is just not appropriate here.”

The fed-funds rate influences other borrowing costs throughout the economy, including rates on mortgages, credit cards and auto loans. The Fed is raising rates to cool inflation by slowing economic growth. It believes those policy moves work through financial markets by tightening financial conditions, such as by raising borrowing costs or lowering prices of stocks and other assets.

Officials have been guarded in recent weeks about providing any guidance that might ignite market rallies that could undermine their efforts to fight inflation.

In recent weeks, markets have rallied partly because investors anticipated that the Fed would slow its rate increases this week and remove uncertainty over the rate outlook, which reduces interest-rate volatility. Lower volatility can ease financial conditions.

Markets have also been cheered by news that inflation and wage growth might have peaked last year, which could make the Fed more comfortable in pausing rate increases. Since Fed officials met in December, economic activity has been mixed. Consumer spending has moderated, and manufacturing activity has weakened. But hiring has held steady, pushing the unemployment down to 3.5% in December, a half-century low.

Investors in bond markets increasingly expect that the Fed will cut interest rates later this year because of a sharp slowdown in economic activity that lowers inflation faster than policy makers expect.

Fed officials and some economists, meanwhile, are concerned that the recent decline in inflation could reflect the long-anticipated easing of supply-chain bottlenecks—and that might not be enough to bring inflation down to the Fed’s 2% goal.

“I’m somewhat worried that the market view is based more on hope,” said Karen Dynan, an economist at Harvard University who served in the Obama administration. “Labor markets still look really tight.”

Officials’ deliberations over how much more to raise rates this year and how long to hold rates at some higher level could hinge over how much they think their past increases will slow the economy this year. Debates could also turn on the degree to which wage and price pressures might slow without significant weakness in the job market.

Officials agreed to slow rate rises to gain more time to study the effects of their moves.

Inflation fell to 4.4% in December from 5.2% in September, as measured by the 12-month change in the personal consumption expenditures price index excluding food and energy. Though still above the Fed’s 2% goal, it moderated in the October-to-December period to an annualised 2.9% rate.

“Inflation has eased somewhat but remains elevated,” said the Fed’s policy statement.

Overall inflation is slowing largely because prices of energy and other goods are falling. Large increases in housing costs have slowed, but haven’t filtered through to official price gauges yet. As a result, Mr. Powell and several colleagues shifted attention recently toward a narrower subset of labor-intensive services by excluding prices for food, energy, shelter and goods.

Mr. Powell has said prices in this category, which rose 4% in December from a year earlier, offer the best gauge of higher wage costs passing through to consumer prices.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The Federal Budget may have softened some of its proposed tax reforms, but it has exposed a bigger issue: too many families are relying on wealth structures that no longer reflect the realities of modern life.

3 min

For many Australians, the 2026 Federal Budget initially felt like a direct challenge to the way wealth is created, held and transferred between generations.

The headlines were immediate: changes to capital gains tax, reforms to discretionary trusts, restrictions on negative gearing and increased scrutiny of investment structures. Unsurprisingly, affluent families, business owners and investors began asking the same question:

Is the way we hold our wealth still fit for purpose?

In recent days, the government has announced several significant amendments following industry consultation and public feedback, including exempting testamentary trusts from the proposed 30 per cent minimum tax and expanding capital gains tax concessions for small businesses.

The backdown is welcome. But it also highlights something much bigger.

This Budget has accelerated a conversation that many Australian families have been postponing for years.

The conversation is not really about tax. It is about wealth stewardship.

For decades, Australians have built wealth through businesses, property, investments and careful long-term planning. Yet many families have not revisited the legal structures surrounding those assets in years, sometimes decades.

We often see clients who have spent years building significant wealth, only to discover their legal arrangements no longer reflect their current circumstances.

Their children are now adults. They may own multiple properties.

They may have sold a business, entered a second marriage, become grandparents or accumulated digital assets that did not exist when their original estate plans were prepared.

The trust that distributes income may need to be reconsidered. The bucket company may no longer be so attractive.

The Budget has simply exposed a reality that already existed: wealth structures cannot remain static while life continues to evolve.

Importantly, trusts themselves are not the issue.

Trusts are legitimate planning tools that provide flexibility, protection and continuity. When used appropriately, they allow families to adapt to changing circumstances over time.

And neither is tax the issue, really. Getting the fundamentals right is more important for long-term, sustainable wealth than a few favourable tax treatments around the edges.

The real issue is complacency.

Too often, families create structures and assume the job is done. It isn’t.

Estate planning is no longer a document you sign once and file away in a drawer. It is an ongoing process that should evolve alongside your life.

We are also seeing a broader shift in how Australians define wealth itself. It is no longer just the family home and an investment portfolio.

Modern wealth includes businesses, digital assets, cryptocurrency, intellectual property, frequent flyer points and increasingly complex family arrangements.

At the same time, Australians are living longer than ever before, meaning wealth may need to support multiple generations simultaneously. This creates new responsibilities and new risks.

How do you help your children enter the property market without exposing family wealth to relationship breakdowns?

How do you structure wealth so that it remains a source of opportunity rather than future conflict?

These are the questions families should be asking now.

The recent debate surrounding testamentary trusts also serves as an important reminder that policy decisions can have unintended consequences for vulnerable Australians. It is encouraging that the government has listened to feedback and clarified its position.

But the lesson remains: the wealth landscape is changing.

Increasingly, governments, regulators and tax authorities are paying closer attention to how wealth is held and transferred. That means families cannot afford to adopt a “set-and-forget” approach to their structures.

The families who will be best placed for the future are not necessarily those with the greatest wealth.

They are the families with the greatest clarity. Clarity around ownership, succession and governance. And clarity around how wealth will transition from one generation to the next.

Ultimately, preserving wealth is not about avoiding change.

It is about preparing for it.

Because the greatest risk is not change itself.

It is losing the ability to respond to it.

Anthony Hunt is Co-Founder of Wealth Lawyers and former COO of Westpac Private Bank. He advises business owners, investors and affluent Australian families on wealth protection, succession planning and intergenerational wealth transfer

ABC Bullion has launched a pioneering investment product that allows Australians to draw regular cashflow from their precious metal holdings.

A cluster of century-old warehouses beneath the Harbour Bridge has been transformed into a modern workplace hub, now home to more than 100 businesses.