The Biggest Winners in America’s Climate Law: Foreign Companies

U.S. seeks to build domestic supply chains but needs overseas expertise

4 min

4 min

The 2022 climate law unleashed a torrent of government subsidies to help the U.S. build clean-energy industries. The biggest beneficiaries so far are foreign companies.

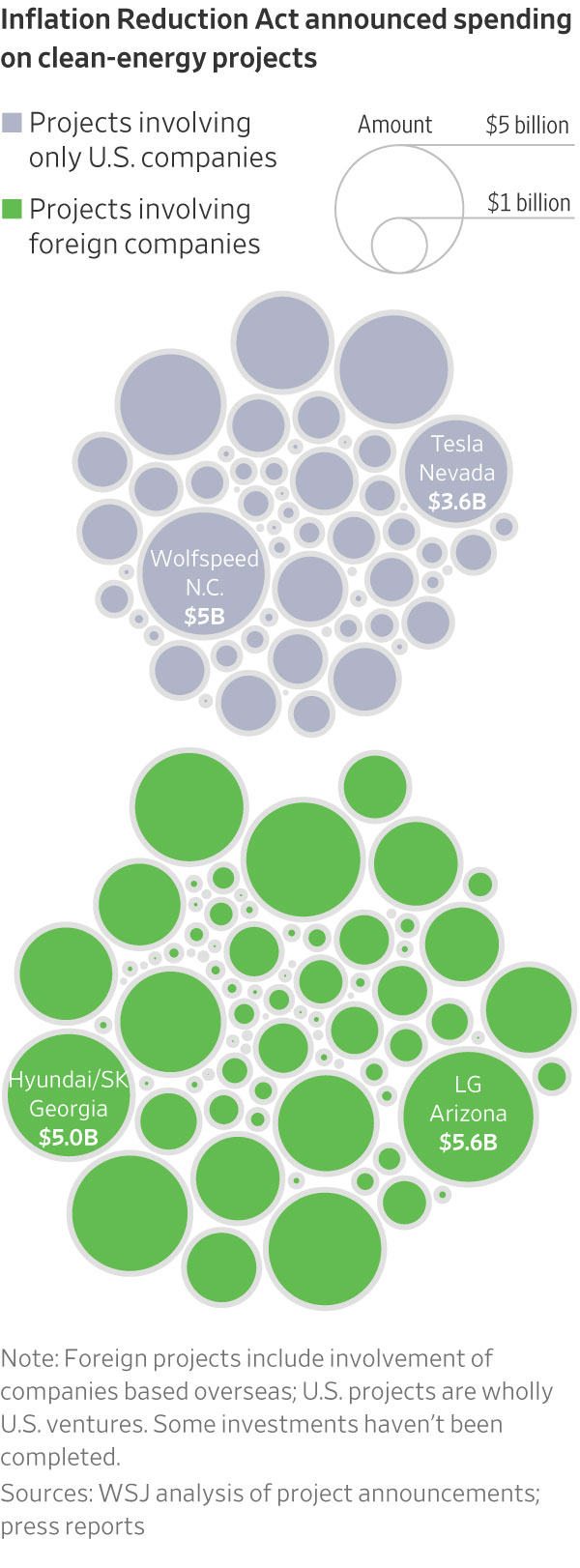

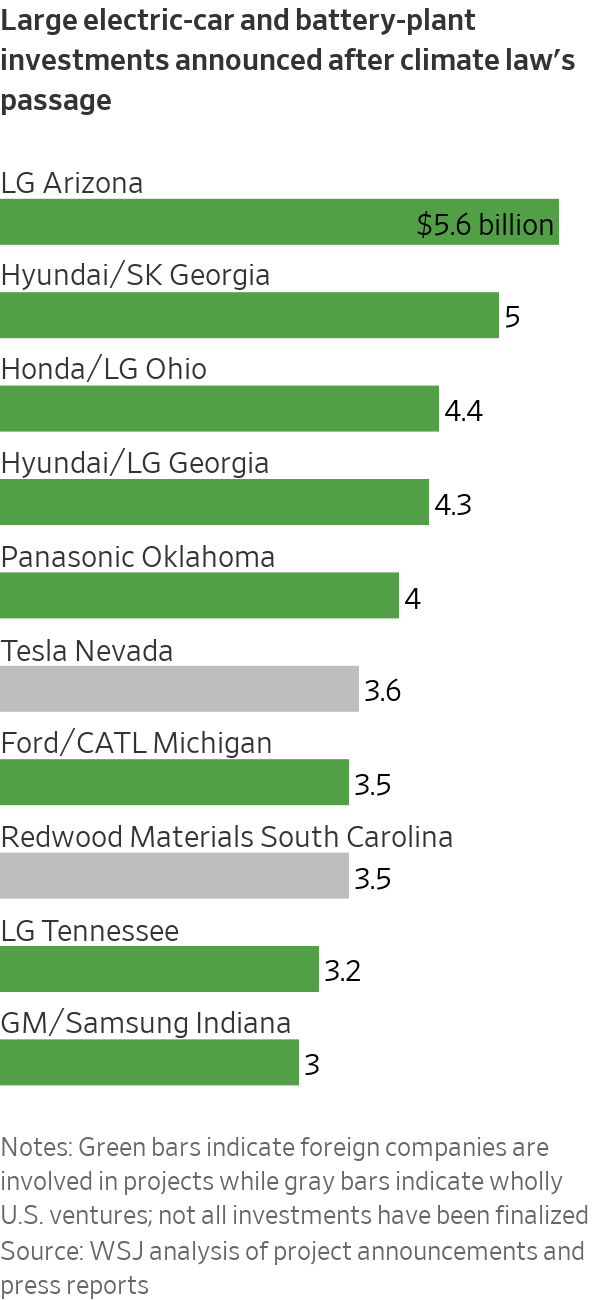

The Inflation Reduction Act has spurred nearly $110 billion in U.S. clean-energy projects since it passed almost a year ago, a Wall Street Journal analysis shows. Companies based overseas, largely from South Korea, Japan and China, are involved in projects accounting for more than 60% of that spending. Fifteen of the 20 largest such investments, nearly all in battery factories, involve foreign businesses, the Journal’s analysis shows.

These overseas manufacturers will be able to claim billions of dollars in tax credits, making them among the biggest winners from the climate law. The credits are often tied to production volume, rewarding the largest investors.

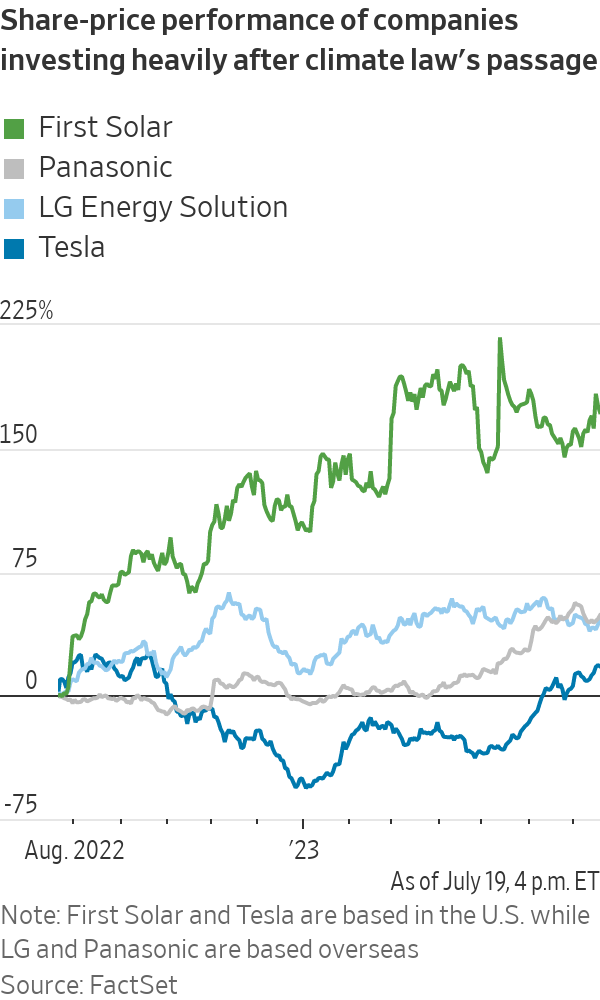

Japan’s Panasonic, one of the few companies to publicly estimate the impact of the law, could earn more than $2 billion in tax credits a year based on the capacity of battery plants it is operating or building in Nevada and Kansas. The company, which supplies batteries to electric-vehicle maker Tesla, is considering a third factory in the U.S. that would lift that total.

The climate law is designed to build up domestic supply chains for green-energy industries, but the reality is that the technology for building batteries and renewable-energy equipment resides overseas. The incentives are leading these companies to invest in the U.S., often alongside domestic businesses.

“It’s a testament to the fact that we still live in a globalised economy,” said Aniket Shah, head of environmental, social and corporate governance—or ESG—strategy at investment bank Jefferies. “You can’t just out of nowhere put up borders and say, ‘It has to be made in America by American companies.’ ”

The Journal looked at roughly 210 clean-energy projects and company initiatives spurred by the law, including projects tracked by industry groups American Clean Power and E2 (Environmental Entrepreneurs); announcements from companies and state and local governments; and media reports. Of those, about 140 disclosed investment amounts totalling roughly $110 billion.

Projects were characterised as either wholly U.S. ventures or foreign if overseas companies are contributing significant investment or technology. Renewable-power facilities and projects already in the works before the law passed were excluded.

Forecasters estimate the climate law could unleash some $3 trillion in total clean-energy investments over the next decade. U.S. companies are also investing heavily, including Tesla, solar-panel maker First Solar and hydrogen producer Air Products and Chemicals.

Full domestic supply chains for batteries or solar panels are still years away because foreign companies dominate nearly every step in the process, from raw materials to sophisticated parts.

The large investments by overseas businesses have generally been welcomed by U.S. communities, many of which have benefited for decades from spending and jobs created by foreign automakers and other companies. But some investments from Chinese companies have fuelled a backlash as tensions between the two countries escalate.

At least 10 of the projects representing nearly $8 billion in investments included in the Journal’s analysis involve companies either based in China or with substantial ties to China through their core operations or large investors.

Some projects are facing resistance, including two in Michigan: a $3.5 billion battery factory that Ford Motor is building with technology and expertise from China’s CATL; and a $2.4 billion battery-component factory from China-based Gotion. Ford is keeping 100% ownership of the battery factory—in part to sidestep the issue of public funds flowing to CATL, according to a person with knowledge of the deal. Ford is licensing the battery-making know-how and services from CATL, the companies said.

But China hawks say the payments Ford makes to CATL mean the Chinese company reaps indirect benefits from government support.

“What we’re seeing is foreign policy conflict with climate policy and trade policy,” Shah said. “We’re going to have to decide as a country what matters more: our enmity with China or our desire to decarbonise quickly.”

Microvast, a startup that was planning to build a more than $500 million battery-component plant in Kentucky, was named as a potential recipient of a $200 million grant from the Energy Department last year. The department later rejected the application. The move followed criticism from Republicans about the company’s ties to China, which include a China subsidiary that accounts for more than 60% of its revenue.

The Energy Department didn’t give a reason for withdrawing the grant. The department takes a number of factors into account when evaluating such projects, including technology risks and the potential for foreign influence, a spokeswoman said.

Microvast, based in Stafford, Texas, says it is a U.S. company and that Chief Executive Yang Wu is an American citizen. The company recently scrapped plans for the Kentucky plant.

“We must be assured that these taxpayer dollars are not being funnelled to the Chinese,” said Cathy McMorris Rodgers (R., Wash.), chair of the House of Representatives committee on energy and commerce, during a June hearing.

Microvast is committed to its goals of investing in the U.S. through other facilities, a spokeswoman said.

The issue is expected to come to a head when the Treasury Department completes rules for electric-car tax credits. The department has proposed that cars using battery materials that were produced by a “foreign entity of concern” such as a Chinese company wouldn’t qualify for tax credits beginning in 2025.

Many expect Treasury to use a loose standard so that some cars qualify, potentially fuelling criticism from some politicians who crafted the climate law such as Sen. Joe Manchin (D., W.Va.), who has argued more lenient criteria go against the intent of the Inflation Reduction Act. Treasury is monitoring shifting markets and supply chains while making rules that advance the law’s goals, a spokeswoman said.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

The megamansion was built for Tony Pritzker, heir to the Hyatt Hotel fortune and brother of Illinois Gov. JB Pritzker.

BMW has unveiled the Neue Klasse in Munich, marking its biggest investment to date and a new era of electrification, digitalisation and sustainable design.