The Improbably Strong Economy

A lot had to go right for the U.S. to avoid a recession. So far, it has.

3 min

3 min

The economy is still generating jobs. A year ago, a lot of economists and Federal Reserve policy makers thought that it would be shedding them by now.

On Friday, the Labor Department reported that the U.S. added a seasonally 150,000 jobs in October from the previous month, versus September’s gain of 297,000 jobs. Some of that step down was due to auto workers’ strikes, which have since been resolved but temporarily caused workers to not draw pay checks.

Average hourly earnings rose 0.2% from a month earlier, putting them 4.1% higher than a year earlier. That was the smallest year-over-year gain since June 2021, though unlike then wages are now outpacing inflation.

One takeaway is that the job market is moderating, but not buckling—a message reinforced by a variety of other data, including low levels of weekly unemployment claims and layoffs. Another is that the Federal Reserve is probably through with tightening: Futures markets on Friday morning indicated that the chance of the central bank raising its target range on overnight rates at its December meeting was below 10%. The yield on the 10-year Treasury note, which briefly hit 5% less than two weeks ago, continued to retreat Friday, falling to 4.53% midmorning.

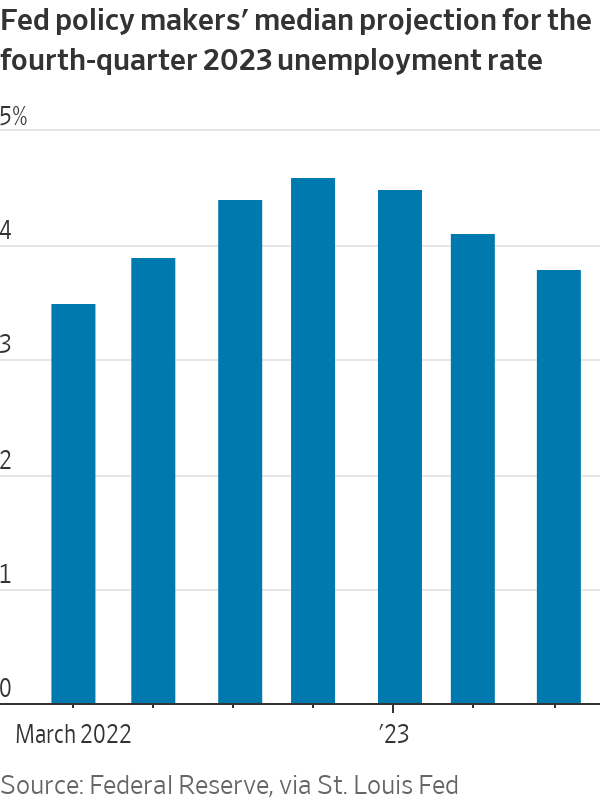

This wasn’t the sort of job market the Fed expected. When policy makers offered projections last December, they forecast that the unemployment rate would average 4.6% in this year’s fourth quarter, versus the 3.7% rate (since revised to 3.6%) they had seen in the November 2022 job report. That was tantamount to a recession forecast, though they didn’t put it that way, since such a large increase in the unemployment rate would count as a strong signal the U.S. is in a downturn. Friday’s report showed the October unemployment rate at 3.9%.

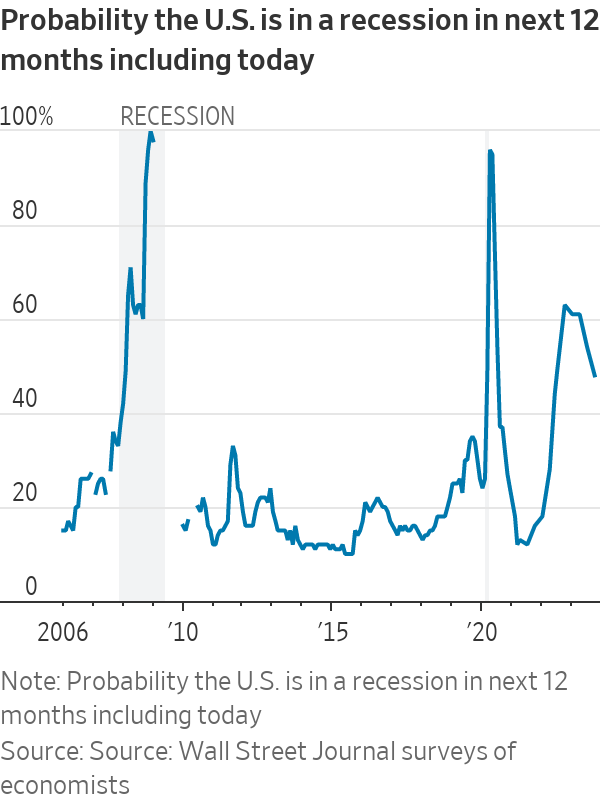

Economists got it wrong, too. In October of last year, forecasters polled by The Wall Street Journal estimated the unemployment rate at the end of 2023 to be at 4.7%, on average. They also put the chances of a recession within the next 12 months at 63%. By last month, they dropped the recession chance to 48%. Available data show that, as a group, economists have never forecast a recession before it has actually started. Now it looks as if the one time they did forecast one, they were either wrong or early.

It is easy to make fun of other people’s past forecasts, but considering the hurdles the economy has had to clear, it really is striking that it has done so well. A year ago there was some hope that the continued recovery in the service sector, and service-sector jobs, might help take up the slack as the goods sector adjusted to slowing demand. But there was also the concern that the service sector could run out of steam before the goods sector found its footing.

Another worry: That the excess savings that Americans had built up after the pandemic struck would run out, and that would cut into their ability to spend. But recent revisions to the available data suggest there was more money left in the tank than thought.

To these, add that inflation has cooled despite the addition of 2.4 million jobs so far this year, and gross domestic product is expanding much faster than economists expected. Plus, at least so far this year, the economy has made it through a regional bank crisis, a sharp increase in both short- and long-term borrowing costs, and the resumption of student-debt payments.

The jury is out on what happens next. The cooling in the job market could turn into a lurch lower, for example, as the full effect of the Fed’s past rate increases begins to take hold. Inflation, which is still too high, could accelerate, prompting the central bank to further tighten the screws.

But the chances of the economy avoiding a recession seem stronger now than they did even a few months ago. A lot of that would be down to luck, but it would nonetheless be something worth celebrating.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

A survey of people with at least $1 million in investable assets found women in their 30s and 40s look nothing like older generations in terms of assets and priorities

A Vaucluse masterpiece by MHNDU with interiors by Poco Designs brings architectural ambition and breathtaking ocean outlook to the auction block.