Trade Woes in Asia Bring Inflation Relief to U.S. Consumers

But slowing exports to Western nations won’t alone stem rapidly rising prices

4 min

4 min

SINGAPORE—Sinking global trade is pummelling Asian exports, bringing some relief on inflation to U.S. and other Western consumers.

But easing prices for home furnishings, electronics and other manufactured goods don’t signal high inflation will soon be defeated. Wage growth and services price gains are still elevated. And central banks in the U.S. and Europe are warning they aren’t finished raising interest rates in their fight to cool inflation.

Cheap Asian goods helped keep a lid on price growth for decades before the pandemic. Economists say that phenomenon is unlikely to return with the same intensity now that the high-water mark of globalisation has passed.

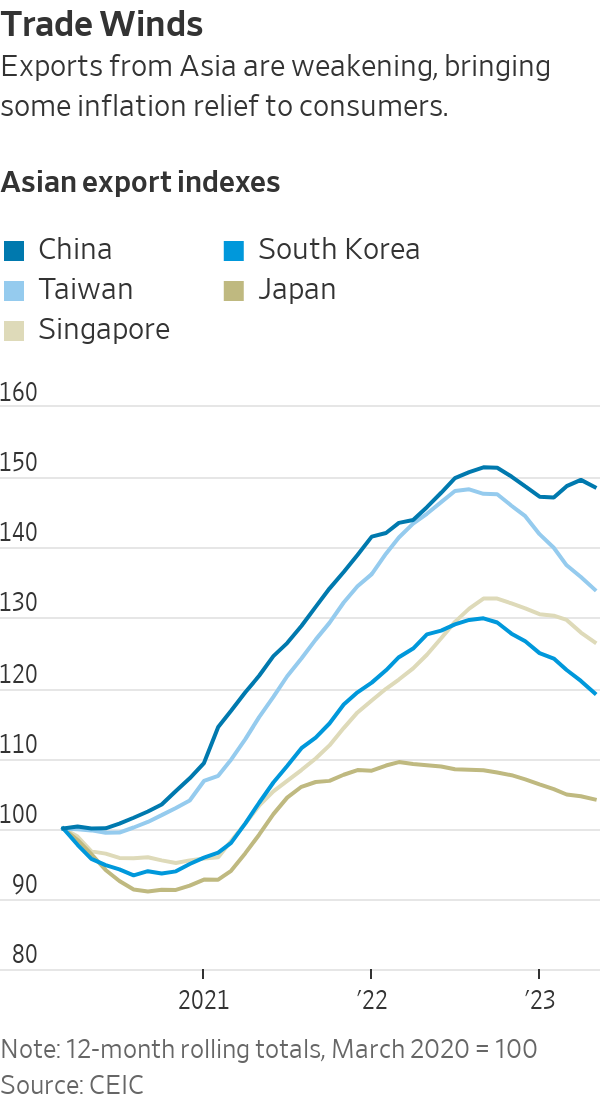

Asia’s powerhouse exporters enjoyed a boom in overseas sales during the pandemic as locked-down consumers splurged on new computers, workout gear and home improvements.

On a rolling 12-month basis, the U.S. dollar value of exports from China, Japan, South Korea, Taiwan and Singapore peaked last year in September at $6.1 trillion. That was 40% higher than recorded over the 12 months through March 2020, when the pandemic began, according to a Wall Street Journal analysis of official figures compiled by data provider CEIC.

Asian exports started sliding late last year as rising interest rates took some heat out of economic growth. Western consumers have slowed spending on goods in favour of eating out, traveling and other services they missed during the pandemic. Hopes that China’s reopening would spur a rebound in trade have fizzled along with the country’s consumer-led recovery.

Exports from South Korea over the 12 months through May were 11% lower than they were in the year through September. Taiwan exports were down 14% over the same period. Singapore’s were down 6%, Japan’s 4% and China’s by 3%.

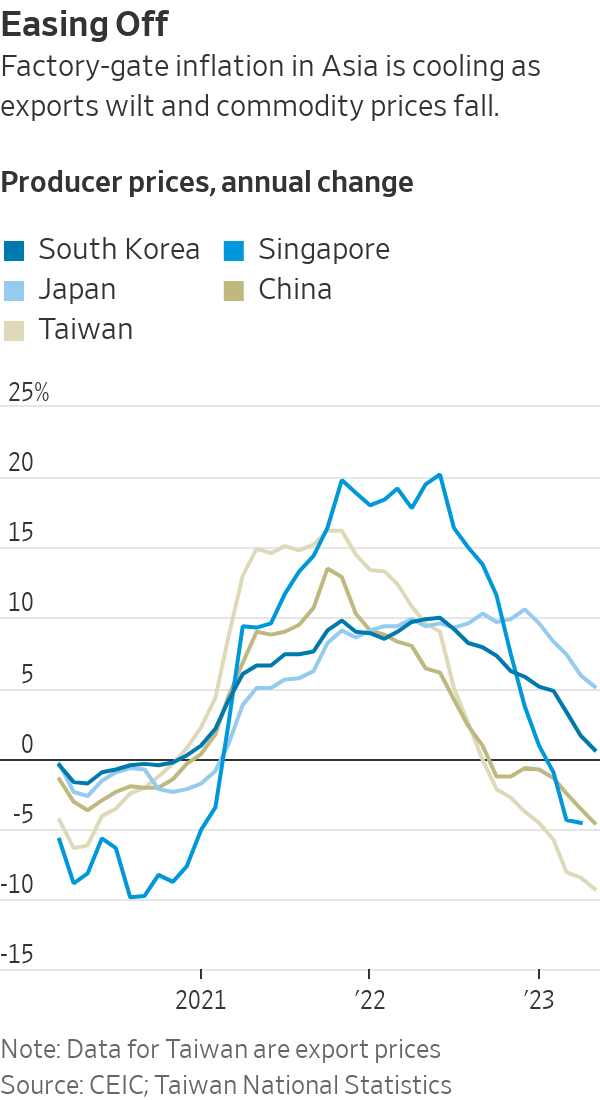

The weakness in trade is showing up in the prices charged for goods when they leave Asia’s factories. Chinese producer prices fell 4.6% in May compared with a year earlier, the eighth straight month of declining supplier prices in the world’s largest factory floor. Similar gauges of inflation in other Asian exporter economies are weakening, too, as lower commodity prices reduce costs and collapsing demand for goods saps companies’ pricing power.

The effects of cooling Asia trade are starting to be felt in the U.S., where the Federal Reserve signalled it expects to further increase interest rates after holding them steady this month.

U.S. import prices for goods from Hong Kong, Singapore, Taiwan and South Korea were down 6.3% in May compared with a year earlier, according to the Labor Department. Import prices were down 2% from China and 3.7% from the Association of Southeast Asian Nations, a 10-member group that includes Indonesia, Malaysia and Thailand.

The prices paid by importers don’t quite line up with the prices faced by consumers, as companies need to cover labor, shipping and other costs to get products into stores.

Nonetheless, prices declined in May from a year earlier for a variety of goods in the U.S. that are often sourced from Asia, including furniture, home appliances, televisions, sports equipment, computers and smartphones.

Overall U.S. inflation is proving resilient, though. The consumer-price index, which measures what Americans pay for goods and services, rose 4% in May from a year earlier—twice the Fed’s 2% goal. Core consumer prices, which exclude food and energy, climbed 5.3%.

If surging prices for goods during the pandemic delivered the first burst of inflation, and rocketing energy prices after Russia invaded Ukraine propelled the second, then the current stickiness of inflation is being fuelled by increases in wages and the price of services. So while easing goods-price inflation is welcome, it doesn’t mean central banks have won the battle, economists say.

“The disinflation impulse coming from Asia is not going to be the magic bullet for the West’s inflation problem,” said Frederic Neumann, chief Asia economist at HSBC in Hong Kong, referring to the slowing pace of price increases.

In the decades before the pandemic, the integration of China into the global economy contributed to a long spell of low and stable inflation enjoyed by many Western economies. The broader integration of markets for goods, services, labor and capital under the banner of globalisation meant cheaper goods for consumers and fewer inflation worries for central banks, though economists debate just how big the effects were.

Now, governments and corporations are tiptoeing away from unfettered globalisation in the interests of security and economic resilience. Manufacturers are adding factories in Vietnam or India while reducing their reliance on China, reflecting concern over icy relations between the U.S.-led West and Beijing. Governments are dangling subsidies in strategic industries such as semiconductors and green-technology products to bring investment and jobs home.

Such trade fractures can increase costs for manufacturers, which, alongside healthier global demand, suggests that inflation in the future won’t be as subdued as it was in the recent past, economists say.

That doesn’t mean globalisation is over or that Asia won’t remain a competitive place to manufacture. But it does mean Asia is unlikely to be as potent a force in tempering price gains as it once was.

“The golden era of globalisation—and the disinflationary pressure associated with that—I think that has gone,” said Neil Shearing, group chief economist at Capital Economics in London.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

Limited to 630 units, Lamborghini’s latest Urus Capsule pushes personalisation further than ever, blending hybrid performance with over 70 bespoke design combinations.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

3 minFor decades, Australia has leaned into its reputation as the lucky country. But luck, as it turns out, is not an economic strategy.

What once looked like resilience now appears increasingly fragile. Beneath the surface of rising property values and steady headline growth, the Australian economy is showing signs of strain that can no longer be ignored.

Recent data paints a sobering picture. Australia has recorded one of the largest declines in real household disposable income per capita among advanced economies.

Wages have failed to keep pace with inflation, meaning many Australians are working harder for less. On a per capita basis, income growth has stalled and, at times, reversed.

And yet, on paper, things still look relatively solid. GDP is growing. Unemployment remains low. But that growth is increasingly being driven by population expansion rather than productivity.

More people are contributing to output, but not necessarily improving living standards.

That distinction matters.

For years, Australia’s economic success rested on a powerful combination: a once-in-a-generation mining boom, a credit-fuelled housing market, strong migration and a property sector that rarely faltered. Between 1991 and 2020, the country avoided recession entirely, building enormous wealth in the process.

But much of that wealth is tied to property. Around two-thirds of household wealth sits in real estate, inflated by leverage and sustained by demand. It has worked, until now.

The problem is the supply side of the economy has not kept up.

Housing supply is falling behind population growth. Rental vacancies are near record lows.

Construction firms are collapsing at an elevated rate. At the same time, massive infrastructure pipelines are competing with residential projects for labour and materials, pushing costs higher and delaying delivery.

The result is a system under pressure from all angles.

Despite near full employment, productivity growth has stagnated for years. In simple terms, Australians are putting in more hours without generating more output per hour. The economy is running faster, butgoing nowhere.

Meanwhile, government spending continues to expand. Public debt is approaching $1 trillion, with spending now accounting for a record share of GDP.

The gap between spending and revenue has been filled by borrowing for decades, adding further pressure to an already stretched system.

This is where the uncomfortable question emerges.

Has Australia become too reliant on a model driven by rising property values, expanding credit and population growth?

As asset prices rise, households feel wealthier and borrow more. Banks lend more. Governments collect more revenue. Migration fuels demand. The cycle reinforces itself.

But when productivity stalls and debt outpaces real income, the system begins to depend on constant expansion just to stay stable.

It is not a collapse scenario. But it is not particularly stable either.

Nowhere is this more evident than in housing.

The National Housing Accord targets 1.2 million new homes over five years, yet current completion rates are well below that pace. With approvals falling and construction costs rising, the gap between supply and demand is widening, not narrowing.

Housing is also one of the largest contributors to inflation, with costs rising sharply across rents, construction and utilities. Yet the private sector, from small investors to major developers, is struggling to make projects stack up in the current environment.

This brings the policy debate into sharper focus.

Tax settings such as negative gearing and capital gains concessions have undoubtedly boosted demand over the past two decades. But they have also supported supply. Removing them may ease prices briefly, but risks deepening the supply shortage over time.

That is the paradox.

Policies designed to make housing more affordable can, in practice, make the shortage worse if they discourage development. The optics may appeal, but the economics are far less forgiving.

It is also worth remembering that most property investors are not institutional players. The majority own just one investment property. They are, in many cases, ordinary Australians using real estate as their primary wealth-building tool.

Undermining that system without replacing it with a viable alternative risks unintended consequences, from reduced supply to higher rents and increased inflation.

So where does that leave Australia?

At a crossroads.

The country can continue to rely on population growth and rising asset prices to drive economic activity. Or it can shift towards a model built on productivity, innovation and sustainable growth.

The latter is harder. It requires structural reform, long-term thinking and political discipline.

But it is also the only path that leads to genuine, lasting prosperity.

The question is no longer whether Australia has been lucky.

It is whether it can evolve before that luck runs out.

Paul Miron is the Co-Founder & Fund Manager of Msquared Capital.

Exclusive eco-conscious lodges are attracting wealthy travellers seeking immersive experiences that prioritise conservation, community and restraint over excess.

Powerhouse real estate couple Avi Khan and Kaylea Sayer welcome their daughter while balancing record-breaking careers, proving success and family can grow side by side.