Why the Drivers of Lower Inflation Matter

Competing effects of central banks, healing supply chains affect recession odds

4 min

4 min

Recent good news on inflation has ignited a debate over how much central banks’ interest-rate increases are responsible.

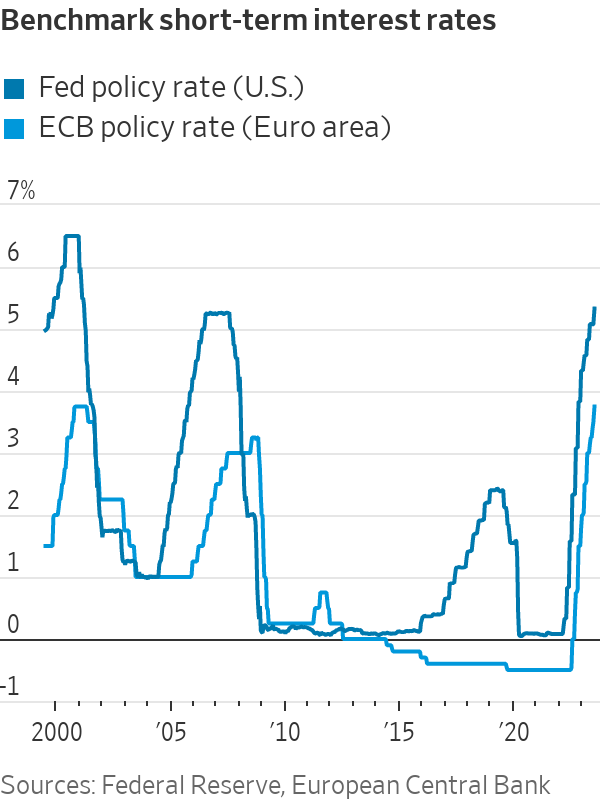

The answer matters for where inflation and interest rates are headed. The Federal Reserve and the European Central Bank in the past week lifted their benchmark interest rates to 22-year highs and left the door open to additional increases.

If higher rates weren’t responsible for the progress on inflation to date, that suggests central banks may be able to lower them before a painful recession sets in.

Central banks generally see their influence on inflation coming through higher rates damping the demand for goods, services and workers, which leads to higher unemployment. That in turn puts downward pressure on prices and wages.

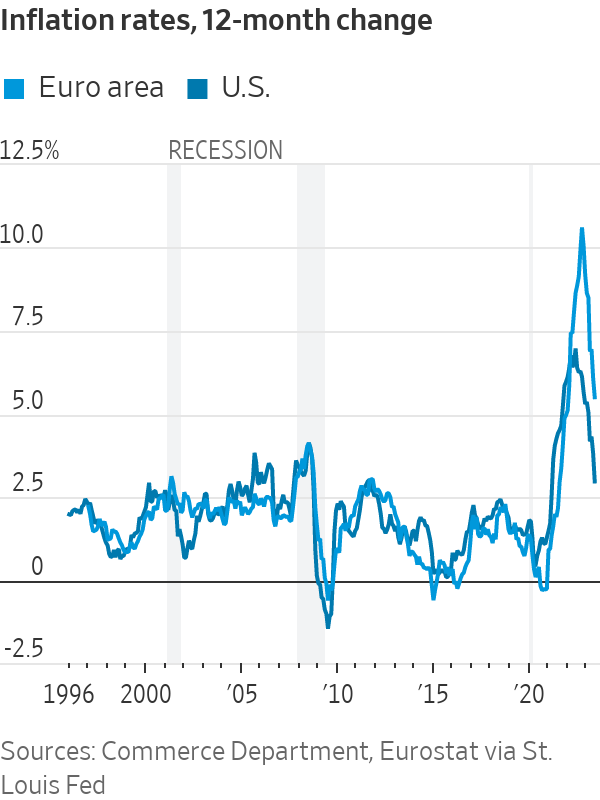

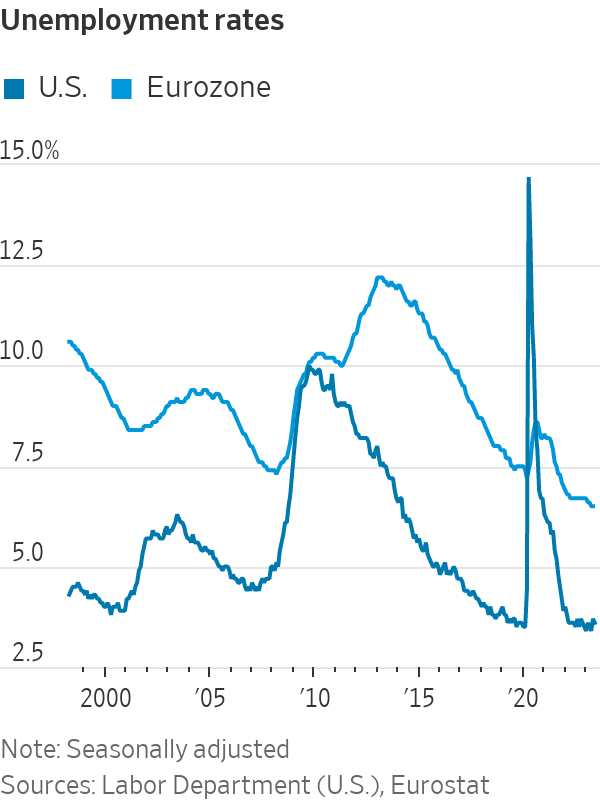

Only the second part of that sequence has occurred. Inflation fell to 3% in the U.S. in June, according to the Fed’s preferred gauge, the personal-consumption expenditures price index, down from 7% one year earlier. Yet the unemployment rate, at 3.6% in June, has held steady for the past year.

In the eurozone, inflation declined to 5.5% in June, the lowest level in nearly 18 months, and unemployment has drifted to the lowest in more than 25 years.

There are competing explanations for this.

One camp argues that inflation has been mostly driven by supply shocks that are going away on their own—much as a postwar surge in the late 1940s unwound by itself. The ripple effects gave the illusion of broader, more persistent price increases.

Take the auto market. Sellers weren’t able to meet pent-up demand two years ago, leading to huge price increases, which in turn spawned higher prices later on for car repairs and auto insurance.

Similarly, a surge in household formation during the pandemic sent up housing prices and rents.

The first camp attributes most of the recent decline in inflation to the ebbing of these one-time supply disruptions, not rate increases, which are supposed to work through the labor market. “It’s calling into question a lot of the old assumptions,” said Lindsay Owens, executive director at the Groundwork Collaborative, a liberal think tank.

A second camp, which includes most economists, disagrees. They say monetary policy kept demand for goods, services, and labor lower than otherwise, taking pressure off strained supply chains and allowing price pressures to ease.

Interest rates can also influence behaviour. The prospect that central bankers would risk a recession to bring down inflation may have influenced expectations of price- and wage-setters, including corporate executives who plan annual budgets for investment and hiring.

Jamie Dimon, chief executive of JPMorgan Chase, warned one year ago of an economic “hurricane” as central banks accelerated rate increases. “You’d better brace yourself,” he said in June 2022, and pledged the bank would be “very conservative” with its balance sheet.

“Inflation is coming down precisely because the Fed avoided more excess demand growth, and they anchored inflation expectations,” said Angel Ubide, head of economic research for global fixed income at Citadel, a hedge-fund firm.

Inflation would be higher now if not for Fed rate increases, “and maybe still rising,” said Karen Dynan, an economist at Harvard University.

In 2021, supply-chain constraints meant even marginal increases in demand led to unusually large price increases. The reverse might be true now: Marginal decreases in demand can bring down prices faster, particularly if more supply is becoming available.

The car market illustrates how monetary policy has been transmitted. Rising rates raised monthly payments, damping demand and robbing sellers of pricing power. In addition, since March, banks appear to be rejecting more car-loan applications.

“That’s leading to a new group of people getting squeezed out of the market, and therefore, it’s playing a role putting downward pressure on prices,” said Julia Coronado, founder of economic-advisory firm MacroPolicy Perspectives.

In Europe, economic growth has stalled since late last year. Business surveys in the past week suggest that growth is weakening sharply, especially in manufacturing, which is most sensitive to interest rates.

The net share of banks reporting increased loan demand declined to a record low in the three months through June, according to an ECB survey of banks. Credit growth to households is the lowest since mid-2016.

Asked at a news conference on Thursday about the transmission of ECB rate increases to growth and inflation, President Christine Lagarde said that in the financial system, “a lot has been transmitted. A lot. We know that. In the economy at large, not as much yet.”

A report published by German insurer Allianz identifies three different forces on the U.S. inflation rate since the second quarter of 2022. Higher inflationary pressures from consumption growth, strong labor markets and government spending added 4 percentage points; fading supply-chain disruptions subtracted five points, and Federal Reserve actions subtracted another five. The net impact was that inflation fell 6 percentage points, whereas it would have fallen only one point without the Fed’s actions.

Fed Chair Jerome Powell said rate increases are “working about as we expect, and we think it’ll play an important role going forward” in bringing down prices for the most labor-intensive services.

Monetary policy has also affected the labor market, but this has shown up in declining job-vacancy rates rather than rising unemployment, some economists say.

Hiring plans in the eurozone services sector are dropping rapidly, according to a survey this month by the European Commission, the European Union’s executive body.

“The labor market is normalising on both sides of the Atlantic, reflecting the impact of higher rates,” said Stefan Gerlach, a former deputy governor of Ireland’s central bank.

The debate over the effect of rate increases also matters for how much further, if at all, central banks need to lift them. Optimists underestimated how much strong demand lifted inflation two years ago. Pessimists may be overestimating the importance of constraining demand to bring it down now.

Gerlach expects inflation to continue declining as higher rates sap demand. “I’m worried central banks have done too much,” he said. “They may have felt embarrassed about having misunderstood inflation the first time.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

With two waterfronts, bushland surrounds and a $35 million price tag, this Belongil Beach retreat could become Byron’s most expensive home ever.