World Bank Warns of Lost Decade for Global Economy

Lender sees demographics, war and pandemic aftereffects holding back growth

4 min

4 min")

Over the past year, governments around the world have announced tax breaks, subsidies and new laws in a bid to accelerate investment, combat climate change and expand their workforces.

That might not be enough.

The World Bank is warning of a “lost decade” ahead for global growth, as the war in Ukraine, the Covid-19 pandemic and high inflation compound existing structural challenges.

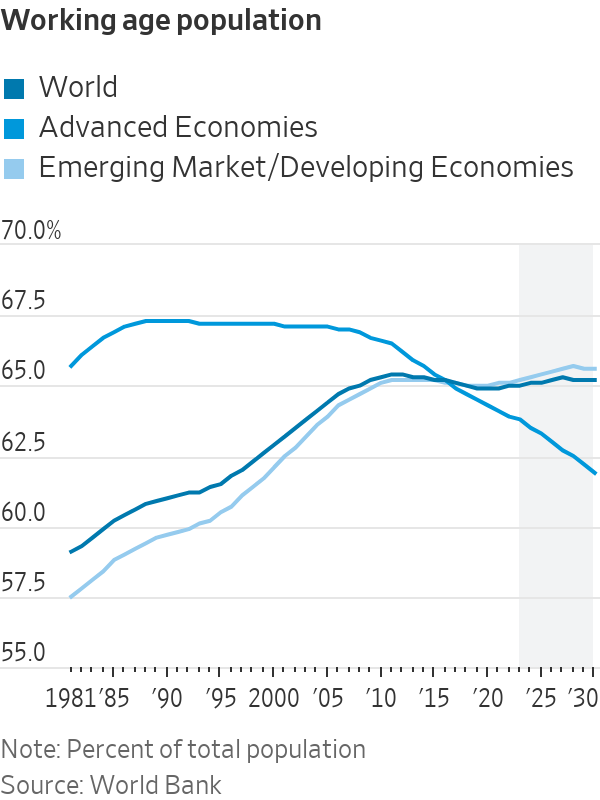

The Washington, D.C.-based international lender says that “it will take a herculean collective policy effort to restore growth in the next decade to the average of the previous one.” Three main factors are behind the reversal in economic progress: an ageing workforce, weakening investment and slowing productivity.

“Across the world, a structural growth slowdown is under way: At current trends, the global potential growth rate—the maximum rate at which an economy can grow without igniting inflation—is expected to fall to a three-decade low over the remainder of the 2020s,” the World Bank said.

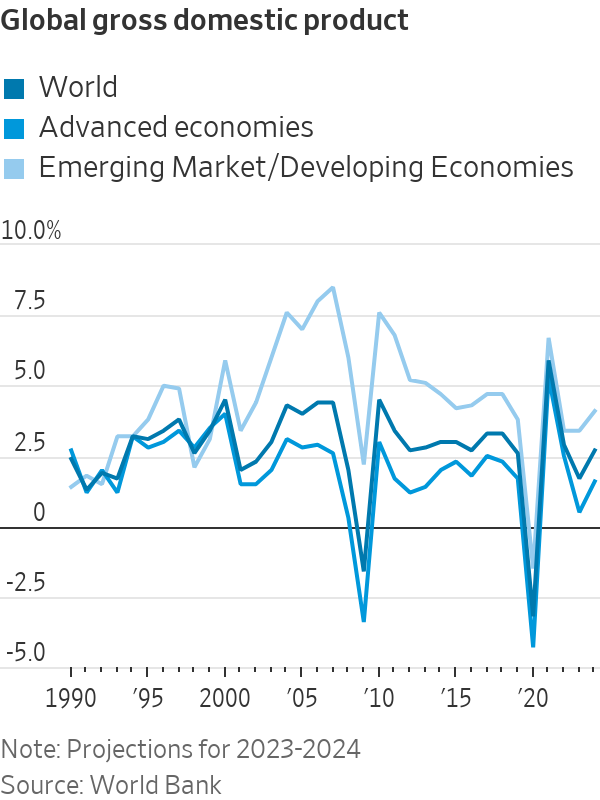

Potential growth was 3.5% in the decade from 2000 to 2010. It dropped to 2.6% a year on average from 2011 to 2021, and will shrink further to 2.2% a year from 2022 to 2030, the bank said. About half of the slowdown is attributable to demographic factors.

The latest alarm bells from the World Bank about the global economy come in the wake of the U.S.’s passing the Inflation Reduction Act, which includes hundreds of billions in incentives and funding for clean energy, as well as a law to ratchet up investments in semiconductors. In response, the European Union is relaxing its rules on government tax breaks and other benefits for clean-tech companies.

Meantime, major economies are trying to boost their workforce numbers, often in the face of steep resistance. In France, protesters responded violently to President Emmanuel Macron’s overhaul of the country’s pension system, while China’s shrinking population has prompted local governments there to offer cash rewards and longer maternity leaves to boost births.

These efforts so far might be too little, too late. Weakness in growth could be even more pronounced if financial crises erupt in major economies and trigger a global recession, the World Bank report cautions. The warning comes just weeks after the collapse of Silicon Valley Bank sparked turmoil in the U.S. and European banking sectors.

Questions surrounding global growth prospects will be in the air in Washington, D.C., alongside the blooming cherry blossoms at the spring meetings of the International Monetary Fund and World Bank from April 10 to 16.

Policy makers and central-bank officials will join economists from around the world to discuss topics including inflation, supply chains, global trade fragmentation, artificial intelligence and human capital.

Earlier this year, the World Bank sharply lowered its short-term growth forecast for the global economy, citing persistently high inflation that has elevated the risk for a worldwide recession. It expects global growth to slow to 1.7% in 2023. Other organisations, such as the International Monetary Fund and the Peterson Institute for International Economics, a Washington-based think tank, expect global GDP growth to expand a more robust 2.9% in 2023.

This isn’t the first time the World Bank has warned of a lost decade. In 2021, the lender said the Covid-19 pandemic raised the prospect owing to lower trade and investment caused by uncertainty over the pandemic. It issued similar warnings after the 2008 financial crisis. Global growth from 2009 to 2018 averaged 2.8% a year, compared with 3.5% in the prior decade.

The World Bank identifies a number of challenges conspiring to push down global growth: weak investment, slow productivity growth, restrictive trade measures such as tariffs and the continuing negative effects—such as learning losses from school closures—because of the pandemic.

It said pro-growth policies would help. Measures to boost labor-force participation among discouraged workers and women can help reverse the negative trend in labor force growth from an older population and lower birthrates, according to the World Bank.

Some view the World Bank’s projection for a lost decade as too pessimistic. Harvard University economist Karen Dynan said that ageing populations in nearly every part of the world will be a drag on global growth, but she was more optimistic on raising productivity—output per worker.

“I expect, outside the demographic effects, output per person to look a lot like it did before the pandemic,” she said.

“The World Bank is right to draw concern to the possibility of a lost decade in sub-Saharan Africa, in Central America, in South Asia—an awful lot of human beings are at risk or are facing very grim situations,” said Adam Posen, president of the Peterson Institute for International Economics.

“But from a global GDP outlook, or even a global population outlook, most of the major emerging markets along with most of the Group of 20 essentially are doing pretty well,” Mr. Posen said. He pointed to economic resilience in Europe and emerging markets in recent years, even as the Federal Reserve has sharply raised interest rates.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

From Italian vegetable-tanned leather to real-world training insight, Australian brand PK9 Gear is redefining what luxury means for discerning dog owners.