Bond Yields End Higher After Wild Session, Lifted By Inflation Data

Higher Treasury yields reflect bets that the inflation report will lead the Fed to raise interest rates more than previously anticipated

3 min

3 min

A wild day of bond-market swings left Treasury yields higher Thursday, reflecting investors’ bets that the latest hot inflation report would push the Federal Reserve to raise interest rates more than previously anticipated.

Yields, which rise when bond prices fall, initially surged toward new multiyear highs after the inflation data, threatening a dramatic break from their recent trading range. Bonds rallied with stocks later in the session, eroding some of the climb. But, unlike stocks, they failed to recoup all of their price declines.

As has often happened this year, yields rose most sharply on short-term bonds, which are particularly sensitive to the near-term interest-rate outlook. But they also climbed on longer-term Treasurys, which tend to have a larger impact on the financial markets and the economy.

Taken together, Thursday’s moves in stocks, bonds and currencies were difficult to understand, said Zach Griffiths, a senior strategist at the research firm CreditSights. They provided more evidence, he added, of “just how volatile markets are and how difficult [they are] to navigate.”

Still, he said, Treasury yields, on their own, did tell a coherent story—with rising short-term yields driven by bets on higher rates and the less-rapid increase in longer-term yields reflecting a “recognition that recession risks are rising.”

At one point Thursday, the yield on the benchmark 10-year Treasury note reached as high as 4.073%—on track for its first close at 4% or higher since 2008, according to Tradeweb. It eventually settled at 3.952%, still up from 3.901% Wednesday and around 3.85% Thursday morning just before the Labor Department released its latest consumer-price index data.

Once again, that data was disappointing to investors. Coming into Thursday, investors had hoped to see a cooling in so-called core inflation, which excludes volatile food and energy categories. Instead, those prices rose 0.6% in September from the previous month—above the forecast of economists surveyed by The Wall Street Journal, who had expected a gain of 0.4%.

Treasury yields are largely determined by what investors expect interest rates set by the Fed will be over the life of a bond. They, in turn, set a floor on borrowing costs across the economy, with rising yields pushing up rates on everything from mortgages to corporate bonds.

Interest-rate derivatives on Thursday showed that investors have essentially no doubt that the Fed will raise rates by at least another 0.75 percentage point at its next meeting in early November. They also showed the chances of a 0.75 percentage point increase in December rising to about 60% to 70% from less than 35% on Wednesday.

The inflation report caught bond investors at a vulnerable moment. Hammered all year by domestic inflation and the Fed’s response, Treasurys have encountered new threats in recent weeks from overseas developments. In particular, they were hurt by volatility in the U.K. bond market stemming from investors’ concerns about recently released tax-cut plans in that country.

They have also been generally weighed down by actions taken by global central banks to both fight inflation and support their local currencies. Many central banks have aggressively raised interest rates. Some in Asia have also intervened in foreign-exchange markets, raising concerns among investors that they might be selling U.S. Treasurys in the process.

Complicating matters on Thursday, Treasurys got some support from overseas events. Most notably, U.K. bonds staged a major rally in response to speculation that the U.K. government might reverse some of its new budget policies. That, analysts said, helped drag down Treasury yields overnight and mitigated their climb after the inflation data.

The 10-year yield has briefly inched above 4% in a couple of overnight trading sessions in recent weeks. But it has yet to settle above that threshold.

The yield has climbed from 1.496% at the end of last year and 3.131% at the end of August, contributing to deeply negative returns for investors across a range of asset classes.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

This stylish family home combines a classic palette and finishes with a flexible floorplan

Just 55 minutes from Sydney, make this your creative getaway located in the majestic Hawkesbury region.

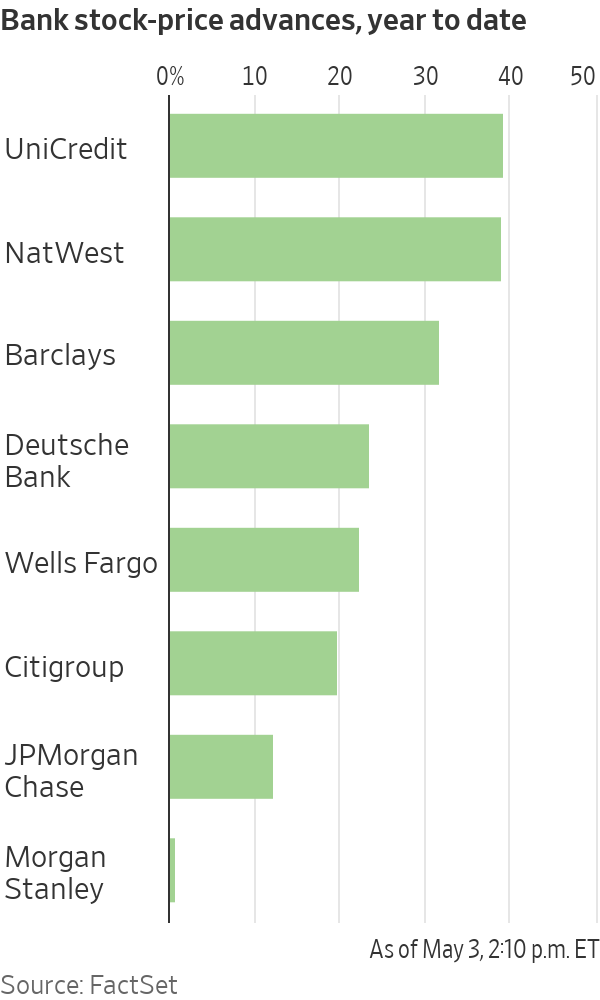

Shares in European banks such as UniCredit have been on a tear

4 min

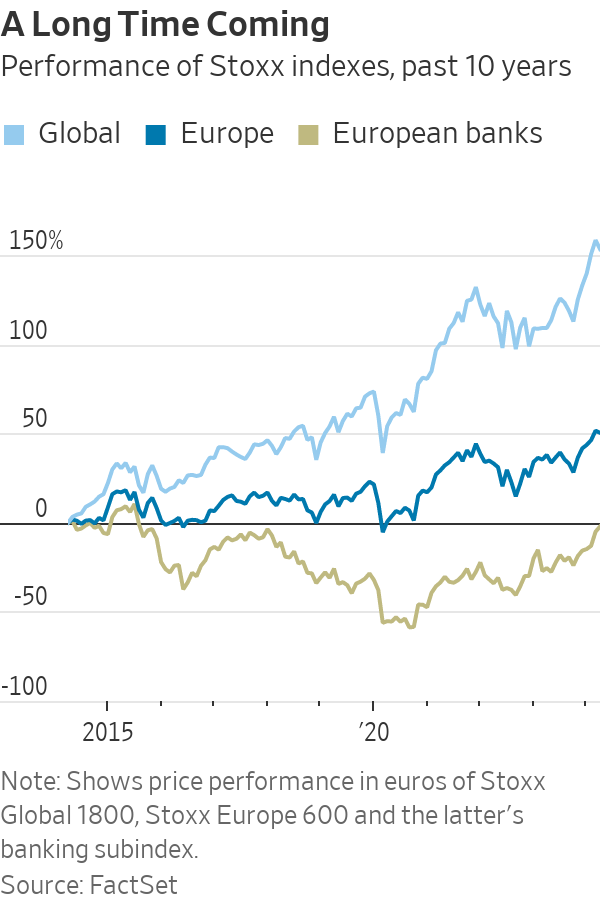

After years in the doldrums, European banks have cleaned up their balance sheets, cut costs and started earning more on loans.

The result: Stock prices have surged and lenders are preparing to hand back some $130 billion to shareholders this year. Even dealmaking within the sector, long a taboo topic, is back, with BBVA of Spain resurrecting an approach for smaller rival Sabadell .

The resurgence is enriching a small group of hedge funds and others who started building contrarian bets on European lenders when they were out of favour. Beneficiaries include hedge-fund firms such as Basswood Capital Management and so-called value investors such as Pzena Investment Management and Smead Capital Management.

It is also bringing in new investors, enticed by still-depressed share prices and promising payouts.

“There’s still a lot of juice left to squeeze,” said Bennett Lindenbaum, co-founder of Basswood, a hedge-fund firm based in New York that focuses on the financial sector.

Basswood began accumulating positions around 2018. European banks were plagued by issues including political turmoil in Italy and money-laundering scandals . Meanwhile, negative interest rates had hammered profits.

Still, Basswood’s team figured valuations were cheap, lenders had shored up capital and interest rates wouldn’t stay negative forever. The firm set up a European office and scooped up stock in banks such as Deutsche Bank , UniCredit and BNP Paribas .

Fast forward to 2024, and European banking stocks are largely beating big U.S. banks this year. Shares in many, such as Germany’s largest lender Deutsche Bank , have hit multiyear highs .

A long-only version of Basswood’s European banks and financials strategy—which doesn’t bet on stocks falling—has returned approximately 18% on an annualised basis since it was launched in 2021, before fees and expenses, Lindenbaum said.

The industry’s turnaround reflects years spent cutting costs and jettisoning bad loans, plus tougher operating rules that lifted capital levels. That meant banks were primed to profit when benchmark interest rates turned positive in 2022.

On a key measure of profitability, return on equity, the continent’s 20 largest banks overtook U.S. counterparts last year for the first time in more than a decade, Deutsche Bank analysts say.

Reflecting their improved health, European banks could spend almost as much as 120 billion euros, or nearly $130 billion, on dividends and share buybacks this year, according to Bank of America analysts.

If bank mergers pick up, that could mean takeover offers at big premiums for investors in smaller lenders. European banks were so weak for so long, dealmaking stalled. Acquisitive larger banks like BBVA could reap the rewards of greater scale and cost efficiencies, assuming they don’t overpay.

“European banks, in general, are cheaper, better capitalised, more profitable and more shareholder friendly than they have been in many years. It’s not surprising there’s a lot of new investor interest in identifying the winners in the sector,” said Gustav Moss, a partner at the activist investor Cevian Capital, which has backed institutions including UBS .

As central banks move to cut interest rates, bumper profits could recede, but policy rates aren’t likely to return to the negative levels banks endured for almost a decade. Stock prices remain modest too, with most far below the book value of their assets.

Among the biggest winners are investors in UniCredit . Shares in the Italian lender have more than quadrupled since Andrea Orcel became chief executive in 2021, reaching their highest levels in more than a decade.

Under the former UBS banker, UniCredit has boosted earnings and started handing large sums back to shareholders , after convincing the European Central Bank the business was strong enough to make large payouts.

Orcel said European banks are increasingly attracting investors like hedge funds with a long-term view, and with more varied portfolios, like pension funds.

He said that investor-relations staff initially advised him that visiting U.S. investors was important to build relationships—but wasn’t likely to bear fruit, given how they viewed European banks. “Now Americans ask you for meetings,” Orcel said.

UniCredit is the second-largest position in Phoenix-based Smead Capital’s $126 million international value fund. It started investing in August 2022, when UniCredit shares traded around €10. They now trade at about €35.

Cole Smead , the firm’s chief executive, said the stock has further to run, partly because UniCredit can now consider buying rivals on the cheap.

Sentiment has shifted so much that for some investors, who figure the biggest profits are to be made betting against the consensus, it might even be time to pull back. A recent Bank of America survey found regional investors had warmed to European banks, with 52% of respondents judging the sector attractive.

And while bets on banks are now paying off, trying to bottom-fish in European banking stocks has burned plenty of investors over the past decade. Investments have tied up money that could have made far greater returns elsewhere.

Deutsche Bank, for instance, underwent years of scandals and big losses before stabilising under Chief Executive Christian Sewing . Rewarding shareholders, he said, is now the bank’s priority.

U.S. private-equity firm Cerberus Capital Management built stakes in Deutsche Bank and domestic rival Commerzbank in 2017, only to sell a chunk when shares were down in 2022. The investor struggled to make changes at Commerzbank.

A Cerberus spokesman said it remains “bullish and committed to the sector,” with bank investments in Poland and France. It retains shares in both Deutsche and Commerzbank, and is an investor in another German lender, the unlisted Hamburg Commercial Bank.

Similarly, Capital Group also invested in both Deutsche Bank and Commerzbank, only to sell roughly 5% stakes in both banks in 2022—at far below where they now trade. Last month, Capital Group disclosed buying shares again in Deutsche Bank, lifting its holding above 3%. A spokeswoman declined to comment.

U.S.-based Pzena, which manages some $64 billion in assets, has backed banks such as UBS and U.K.-listed HSBC , NatWest and Barclays .

Pzena reckoned balance sheets, capital positions and profitability would all eventually improve, either through higher interest rates or as business models shifted. Still, some changes took longer than expected. “I don’t think anyone would have thought the ECB would keep rates negative for eight or nine years,” said portfolio manager Miklos Vasarhelyi.

Some Pzena investments date as far back as 2009 and 2010, Vasarhelyi said. “We’ve been waiting for this to turn for a long time.”

This stylish family home combines a classic palette and finishes with a flexible floorplan

Consumers are going to gravitate toward applications powered by the buzzy new technology, analyst Michael Wolf predicts