Investors Were Burned by European Banks for Years—Until Now

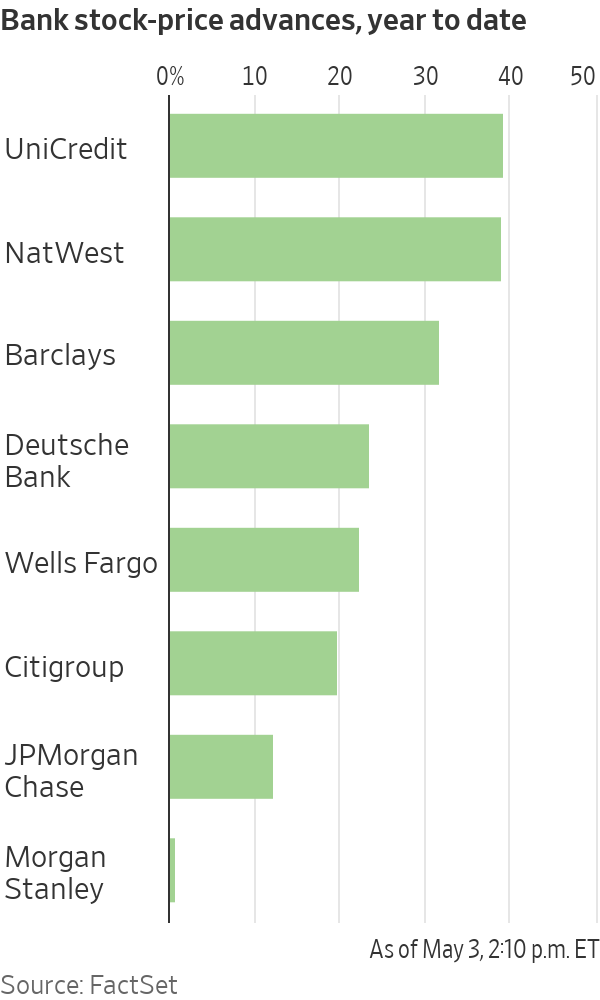

Shares in European banks such as UniCredit have been on a tear

4 min

4 min

After years in the doldrums, European banks have cleaned up their balance sheets, cut costs and started earning more on loans.

The result: Stock prices have surged and lenders are preparing to hand back some $130 billion to shareholders this year. Even dealmaking within the sector, long a taboo topic, is back, with BBVA of Spain resurrecting an approach for smaller rival Sabadell .

The resurgence is enriching a small group of hedge funds and others who started building contrarian bets on European lenders when they were out of favour. Beneficiaries include hedge-fund firms such as Basswood Capital Management and so-called value investors such as Pzena Investment Management and Smead Capital Management.

It is also bringing in new investors, enticed by still-depressed share prices and promising payouts.

“There’s still a lot of juice left to squeeze,” said Bennett Lindenbaum, co-founder of Basswood, a hedge-fund firm based in New York that focuses on the financial sector.

Basswood began accumulating positions around 2018. European banks were plagued by issues including political turmoil in Italy and money-laundering scandals . Meanwhile, negative interest rates had hammered profits.

Still, Basswood’s team figured valuations were cheap, lenders had shored up capital and interest rates wouldn’t stay negative forever. The firm set up a European office and scooped up stock in banks such as Deutsche Bank , UniCredit and BNP Paribas .

Fast forward to 2024, and European banking stocks are largely beating big U.S. banks this year. Shares in many, such as Germany’s largest lender Deutsche Bank , have hit multiyear highs .

A long-only version of Basswood’s European banks and financials strategy—which doesn’t bet on stocks falling—has returned approximately 18% on an annualised basis since it was launched in 2021, before fees and expenses, Lindenbaum said.

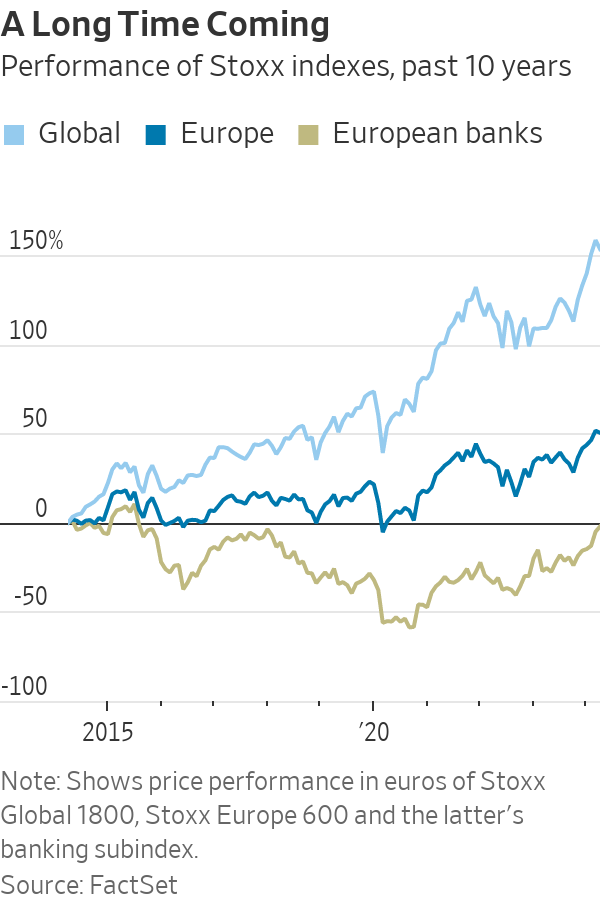

The industry’s turnaround reflects years spent cutting costs and jettisoning bad loans, plus tougher operating rules that lifted capital levels. That meant banks were primed to profit when benchmark interest rates turned positive in 2022.

On a key measure of profitability, return on equity, the continent’s 20 largest banks overtook U.S. counterparts last year for the first time in more than a decade, Deutsche Bank analysts say.

Reflecting their improved health, European banks could spend almost as much as 120 billion euros, or nearly $130 billion, on dividends and share buybacks this year, according to Bank of America analysts.

If bank mergers pick up, that could mean takeover offers at big premiums for investors in smaller lenders. European banks were so weak for so long, dealmaking stalled. Acquisitive larger banks like BBVA could reap the rewards of greater scale and cost efficiencies, assuming they don’t overpay.

“European banks, in general, are cheaper, better capitalised, more profitable and more shareholder friendly than they have been in many years. It’s not surprising there’s a lot of new investor interest in identifying the winners in the sector,” said Gustav Moss, a partner at the activist investor Cevian Capital, which has backed institutions including UBS .

As central banks move to cut interest rates, bumper profits could recede, but policy rates aren’t likely to return to the negative levels banks endured for almost a decade. Stock prices remain modest too, with most far below the book value of their assets.

Among the biggest winners are investors in UniCredit . Shares in the Italian lender have more than quadrupled since Andrea Orcel became chief executive in 2021, reaching their highest levels in more than a decade.

Under the former UBS banker, UniCredit has boosted earnings and started handing large sums back to shareholders , after convincing the European Central Bank the business was strong enough to make large payouts.

Orcel said European banks are increasingly attracting investors like hedge funds with a long-term view, and with more varied portfolios, like pension funds.

He said that investor-relations staff initially advised him that visiting U.S. investors was important to build relationships—but wasn’t likely to bear fruit, given how they viewed European banks. “Now Americans ask you for meetings,” Orcel said.

UniCredit is the second-largest position in Phoenix-based Smead Capital’s $126 million international value fund. It started investing in August 2022, when UniCredit shares traded around €10. They now trade at about €35.

Cole Smead , the firm’s chief executive, said the stock has further to run, partly because UniCredit can now consider buying rivals on the cheap.

Sentiment has shifted so much that for some investors, who figure the biggest profits are to be made betting against the consensus, it might even be time to pull back. A recent Bank of America survey found regional investors had warmed to European banks, with 52% of respondents judging the sector attractive.

And while bets on banks are now paying off, trying to bottom-fish in European banking stocks has burned plenty of investors over the past decade. Investments have tied up money that could have made far greater returns elsewhere.

Deutsche Bank, for instance, underwent years of scandals and big losses before stabilising under Chief Executive Christian Sewing . Rewarding shareholders, he said, is now the bank’s priority.

U.S. private-equity firm Cerberus Capital Management built stakes in Deutsche Bank and domestic rival Commerzbank in 2017, only to sell a chunk when shares were down in 2022. The investor struggled to make changes at Commerzbank.

A Cerberus spokesman said it remains “bullish and committed to the sector,” with bank investments in Poland and France. It retains shares in both Deutsche and Commerzbank, and is an investor in another German lender, the unlisted Hamburg Commercial Bank.

Similarly, Capital Group also invested in both Deutsche Bank and Commerzbank, only to sell roughly 5% stakes in both banks in 2022—at far below where they now trade. Last month, Capital Group disclosed buying shares again in Deutsche Bank, lifting its holding above 3%. A spokeswoman declined to comment.

U.S.-based Pzena, which manages some $64 billion in assets, has backed banks such as UBS and U.K.-listed HSBC , NatWest and Barclays .

Pzena reckoned balance sheets, capital positions and profitability would all eventually improve, either through higher interest rates or as business models shifted. Still, some changes took longer than expected. “I don’t think anyone would have thought the ECB would keep rates negative for eight or nine years,” said portfolio manager Miklos Vasarhelyi.

Some Pzena investments date as far back as 2009 and 2010, Vasarhelyi said. “We’ve been waiting for this to turn for a long time.”

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

The voices reshaping how Australians think about money — and why credibility matters more than reach.

6 min

The best financial advice many Australians are receiving right now is not coming from licensed advisers charging by the hour. It is coming through a phone screen, in the ten minutes between work and dinner, from creators who have built credibility the hard way: by being right, being transparent, and being specific in a space where vagueness has always been the easy default.

This is not a ranking by follower count. Follower count is a measure of distribution, not of quality. What follows is a ranking by substance — credentials, accuracy, community depth, and the quality of what an audience actually learns from following these accounts. The distinction matters, because the Australians acting on this content are making real financial decisions with real money.

1- Queenie Tan – Corporate Authorised Representative; Co-Founder & Director, Invest With Queenie & Billroo

There are finance influencers who talk about building wealth, and there are those who document it in real time with receipts. Queenie Tan belongs firmly in the second category. Starting from a $400-per-week income, Tan built her net worth past $1 million while publishing the actual numbers — income, savings rate, investment decisions — for an audience of more than 400,000 across platforms.

She is a Corporate Authorised Representative, co-founder of the personal finance app Billroo, and the author of a book that has become a practical reference for young Australians navigating ETFs, superannuation and property. What separates her from the crowded field of money educators is precision: she does not talk in principles when she can talk in percentages.

2- Alan Kohler – Editor-in-Chief, Eureka Report; Editor-in-Chief, InvestSMART Group; ABC News finance presenter, host of Inside Business.

If Queenie Tan represents the new wave of personal finance creators, Alan Kohler represents something the new wave will spend decades trying to build: institutional credibility that has survived multiple economic cycles. As Editor-in-Chief of the Eureka Report and InvestSMART Group, and a decades-long presence on ABC News, Kohler has spent more than thirty years making financial analysis accessible without dumbing it down.

His coverage of RBA decisions, market movements and economic policy is cited by podcasters, journalists and fund managers alike. He is not chasing virality. He does not need to.

3- Aleks Nikolic – Corporate lawyer; host, Big Swinging Stocks podcast

Most finance creators address the mechanics of money. Aleks Nikolic addresses the psychology — and that distinction explains why her following is as loyal as it is. Operating as Broke Girl Wealth across Instagram, TikTok and YouTube, Nikolic covers ETFs, crypto and investment strategy, but her real differentiator is a willingness to discuss the emotional architecture of financial decision-making.

Shame around debt. Fear around market volatility. The limiting beliefs that stop people acting on what they already know. In a space where confidence is routinely performed, her candour is a genuine competitive advantage.

4- Bryce Leske & Alec Renehan – Equity Mates Media

Equity Mates did not build a following. They built a media company. What began as a podcast by two friends learning to invest has grown into Australia’s most established investing media brand, covering ASX stocks, ETFs, global markets and fund manager interviews across podcast, social and YouTube.

The longevity is the credential. Equity Mates has operated through multiple market cycles, a global pandemic, and a generational shift in how Australians engage with investing — and its audience has grown through all of it. When the hosts speak, their listeners know they have been paying attention for years.

5- The Lazy CEO – CEO & Founder, Showpo; Shark Tank Australia investor

The metric that matters most on social media is not followers — it is engagement, because engagement signals trust. Jane Lu, known as The Lazy CEO, maintains an engagement rate of approximately 1.15 per cent on Instagram, which is exceptional for a finance account of his size. Her 242,000-plus followers are not passive consumers: they ask questions, share experiences and apply what they read.

Her content focuses on business finance and wealth building, and the active comment sections are the clearest possible evidence that her audience does not merely scroll past.

6- Tash Invests – Founder, Tash Lends; Forbes Australia 30 Under 30

Tash Invests built her following on a premise that sounds simple but is rarer in practice than it should be: she publishes the actual numbers. Not approximations or ranges or anonymised case studies — her salary, her savings rate, her portfolio value, her net worth, updated and on the record.

Having bought her first property at twenty-two and grown her documented net worth past $1 million, she has become the primary reference point for young Australians trying to understand what building wealth on a moderate income genuinely looks like. The specificity is the product.

7- David Scutt – APAC Market Analyst at StoneX Group

The authority of most finance social media content rests on research and reading. David Scutt‘s authority rests on having done the job. A former Treasury Dealer at Arab Bank and the Commonwealth Bank, former ASX Business Supervisor, and former Global Markets Editor at Business Insider Australia and anchor at ausbiz TV, Scutt now brings that direct market experience to his role as APAC Market Analyst at StoneX Group, rather than relying on secondary commentary.

When he discusses foreign exchange movements or ASX dynamics, it is not because he has read about them. It is because he has traded them.

8- Meddy Demars – Investing & crypto content creator

The gap Meddy Demars fills is specific and underserviced: connecting global macroeconomic events to the practical reality of Australian investors. When the US Federal Reserve adjusts interest rates, when inflation data moves, when commodity prices shift — most Australian finance content either ignores the local implications or translates them poorly.

Demars, operating across TikTok and Instagram from Sydney, does the translation well: explaining what global conditions mean for Australian stocks, savings rates and investment portfolios in terms that are accessible without being condescending.

9- Simran Kaur – Founder, Friends That Invest

Friends That Invest is arguably the most successful community-building exercise in Australian personal finance, and Simran Kaur is the reason why. The New Zealand-based creator — whose audience is predominantly Australian — built a podcast, a book and a social media presence around a single insight: that the personal finance world was not speaking to young women, and that the consequences of that gap were significant.

The measurable cultural shift that followed — women engaging with investing concepts in communities that had not previously existed — is the kind of impact that most financial literacy programmes aim for and rarely achieve.

10- Effie Zahos – Money Editor at 9News

Effie Zahos is one of Australia’s most recognised financial commentators, appearing regularly across 9News, A Current Affair, Today and Today Extra as 9News Money Editor. Her role puts everyday money questions, from mortgage rates to cost-of-living pressures, in front of a national broadcast audience.

Before television, she spent years as editor of Money magazine, building the editorial foundation for her current commentary. She is also Director and Money Commentator at InvestSMART, an ambassador for Canstar, and a published author, with her financial advice available in print as well as on screen.

That combination, decades of editorial experience, an active broadcast presence, and a body of published work, is what makes her commentary carry weight beyond any single platform or post.

From gorilla encounters in Uganda to a reimagined Okavango retreat, Abercrombie & Kent elevates its African journeys with two spectacular lodge transformations.

Many of the most-important events have slipped from our collective memories. But their impacts live on.