What to do with a redundancy payout

Make sure you plan your next move carefully to make the most of your payout

3 min

3 min

You wouldn’t really call a redundancy a career highlight given you’re losing your job. But you’re being compensated for that loss with a lump sum of money – in some cases up to a year’s salary or more.

Experts agree that a redundancy is not necessarily the career death knell it may at first appear.

For many, a redundancy and the payout that comes with it, can be the opportunity for a new start; perhaps a career overhaul, the chance to start a business, a slide into early retirement or the opportunity to boost your superannuation or pay down your mortgage. It could even be a long-awaited extended overseas holiday.

Read more stories like this in the launch issue of Kanebridge Quarterly magazine. Order your copy here

The opportunity a redundancy brings really depends on where you’re at in life, your age – and the amount of money you receive.

“It can very much be a re-start,” says Steve Mickenbecker, money expert at finance comparison site, Canstar. “People (who get a redundancy) tend to re-visit life goals, they ask themselves ‘What do I want to do? What do I value?’. The beauty is you’re being paid a sum that gives you some breathing space to work this out.”

What you do with your redundancy payout will depend on whether you need to live on the money while you look for another job. If you’re on the job market, you may need to make the money last an uncertain amount of time.

If this is the case, the first step should be to make a personal budget, which you can do using online tools and calculators, or with the help of a money coach or financial advisor. Beyond that, your options are simple – invest it or spend it – says Noel Whitaker, a finance columnist and author of Retirement Made Simple. However, the best financial roadmap will vary from person to person.

“I would start by talking to an advisor or your accountant at the outset who can explain the tax implications associated with a redundancy payout, which can be complicated,” Whitaker says. “The best thing you can do regardless of which option you take is to stay as flexible as possible. For instance, you can pay down your mortgage, or you can put your money into your mortgage off-set account, if your loan has one, so you can still access it should you need it.”

He says age also plays a factor. If you are older, you may want to put it in your super knowing you won’t be losing access to it for long, an option that is less attractive to someone in their 30s, for instance, who will not be able to access that money for several decades more.

Bryan Ashenden, the head of financial literacy and advocacy at wealth management company, BT, breaks down the figures on investing versus super.

“With an investment, you will get the benefit of not only the dividend or return, but also capital growth depending on how you invest the money,” Ashenden says. “For example, a $20,000 investment may generate a four per cent income return (or $800 per annum) but may also provide a capital growth of five per cent per annum (or $1000). So, after one year, your $20,000 investment is worth $21,000 and your $800 income return could either be re-invested or perhaps used towards repaying some of your home loan principal or interest.

“If invested via super, with the same rates of return, the $800 income return would be worth $680 after tax, but because it is locked in the super system until you access it, it can be reinvested (with the $1000 capital growth), meaning you have $21,680 as a net investment after one year.”

The added benefit of investing via super, he says, is that when you access the funds after the age of 60, the money comes back to you tax free. For some, the temptation to invest in a small business venture could also be alluring. But that could be a high risk option.

“There are a lot of challenges (to small business) in today’s environment,” says Small Business Association of Australia CEO Anne Nalder. “It’s not a booming period, with inflation tipped to go close to eight per cent by the end of the year and interest rates also going up.

“If you are going to invest in a small business, look at the potential growth areas and go into something you’re good at, familiar with and passionate about.”

Ultimately, while taking a holiday is a ‘sunk cost’ it could be just the refresher you need before making your next move.

This stylish family home combines a classic palette and finishes with a flexible floorplan

Just 55 minutes from Sydney, make this your creative getaway located in the majestic Hawkesbury region.

A sharp rebound in tourism in Europe’s sunbelt powers its economic rebound as core manufacturing centres struggle to recover

3 min

Europe’s economy has a north-south divide—and now it’s the poorer south that is powering the region’s return to growth.

Southern Europe, which for decades has had lower growth, productivity and wealth than the north, powered an upside-down recovery on the continent at the start of the year. Buoyant tourism revenue around the Mediterranean helped to offset sluggishness in Europe’s manufacturing heartlands.

The south’s transformation from laggard into growth engine reflects both a rapid rebound in visitor numbers from the collapse during the Covid-19 pandemic and a series of blows the continent’s large manufacturing sector has suffered, from surging energy prices to trade conflicts.

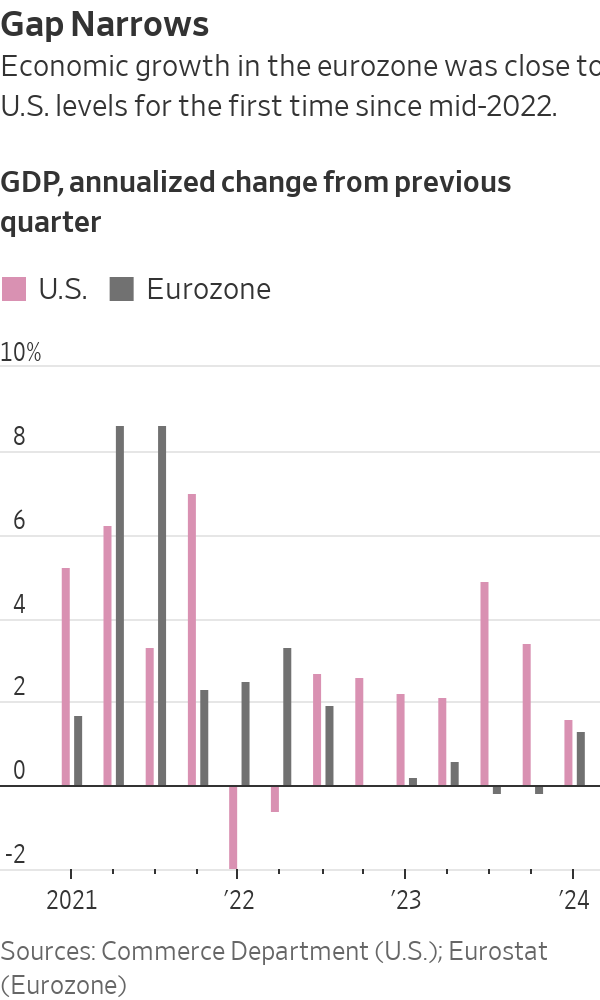

Now growth in the south is more than offsetting the north’s manufacturing malaise: As a whole, the eurozone economy grew at an annualised rate of 1.3% in the first quarter, ending nearly 18 months of economic stagnation in a sign that the currency area is recovering from the damage done by Russia’s invasion of Ukraine.

It was the eurozone’s strongest performance since the third quarter of 2022, and approached the U.S. economy’s 1.6% first-quarter growth rate, which was a slowdown from a racy pace of 3.4% at the end of last year.

In the 2010s, Germany helped to drag the continent out of its debt crisis thanks to strong exports of cars and capital goods. Between 2021 and 2023, Italy, Spain, Greece and Portugal contributed between a quarter and half of the European Union’s annual growth, according to a report last year by French credit insurer Coface —a trend now confirmed and amplified in the latest data.

In the first quarter, Spain was the fastest-growing of the big eurozone economies. It and Portugal recorded growth of 0.7% in the three months through the end of March from the previous quarter, while Italy’s economy grew by 0.3%. France and Germany both grew by 0.2%, the latter rebounding from a 0.5% quarter-on-quarter contraction at the end of last year.

This means Germany’s economy has grown by 0.3% in total since the end of 2019, compared with 8.7% for the U.S., 4.6% for Italy and 2.2% for France, according to UniCredit data.

In Spain, strong growth “seems to have been entirely due to strong tourism numbers,” said Jack Allen-Reynolds, an economist with Capital Economics. Tourism accounts for around 10% of the economies of Spain, Italy, Greece and Portugal.

The euro rose by about a quarter-cent against the dollar, to $1.0725, after the latest growth and inflation data were published.

The recovery comes as the European Central Bank signals it is preparing to reduce interest rates in June after a historic run of increases since mid-2022 that took it the key rate to 4%. Inflation in the eurozone remained at 2.4% in April, while underlying inflation cooled slightly, from 2.9% to 2.7%, according to separate data published Tuesday.

“The ECB hawks will point to the strong GDP number as [an] argument that ECB can take its rates lower gradually,” said Kamil Kovar, senior economist at Moody’s Analytics.

The eurozone economy has flatlined since late 2022 as Russia’s attack on its neighbor sent food and energy prices soaring in Europe and sapped business and household confidence. Gross domestic product fell in both the third and fourth quarters of last year, meeting a definition of recession widely used in Europe, but not in the U.S.

Southern Europe is one of only a handful of regions where international tourist arrivals returned to pre pandemic levels last year, according to United Nations data. Tourism revenue across the EU was one-quarter higher in the three months through the end of last June than in the same period in 2019, according to Coface data.

The recovery in international tourism was “notably driven by the arrival of many Americans who…were able to take advantage of favorable exchange rates,” Coface analysts wrote. “On the other hand, the end of the zero-Covid policy in China has initiated a gradual return of Chinese tourists, although remaining below 2019 levels.”

In Portugal, the number of foreign tourists hit a record of more than 18 million last year, up 11% compared with the prepandemic year of 2019, official data showed in January. American tourists in particular have returned to Europe in force.

Tourist numbers in Asia Pacific and the Americas continued to lag 2019 levels by 35% and 10% last year, respectively, the data show.

It is unclear how much further the tourism boom can run, but economists expect the region’s economic recovery to strengthen later this year as cooling inflation boosts household spending power and lower energy costs aid factory output.

Recent surveys point to an improved outlook for growth. Consumer confidence has risen to its highest level in two years, and a leading business-sentiment index has shown steady improvement from the start of 2024.

“We think that the combination of a robust labor market, comparatively strong wage hikes and lower inflation compared with last year will finally lead to a moderate recovery in consumer spending in the next few quarters,” said Andreas Rees , an economist with UniCredit in Frankfurt.

This stylish family home combines a classic palette and finishes with a flexible floorplan

Consumers are going to gravitate toward applications powered by the buzzy new technology, analyst Michael Wolf predicts