Big Tech Stops Doing Stupid Stuff

This year it might be smart to invest in companies that think a little smaller

3 min

3 min Jeff Bezos, Wally Funk, Oliver Daemen, and Mark Bezos walk near the booster to pose for a picture after flying into space in the Blue Origin New Shepard rocket on July 20, 2021 in Van Horn, Texas. Mr. Bezos and the crew were the first human spaceflight for the company. (Photo by Joe Raedle/Getty Images)")

The era of moonshots is (mostly) over. This year tech companies are taking a more earthly approach.

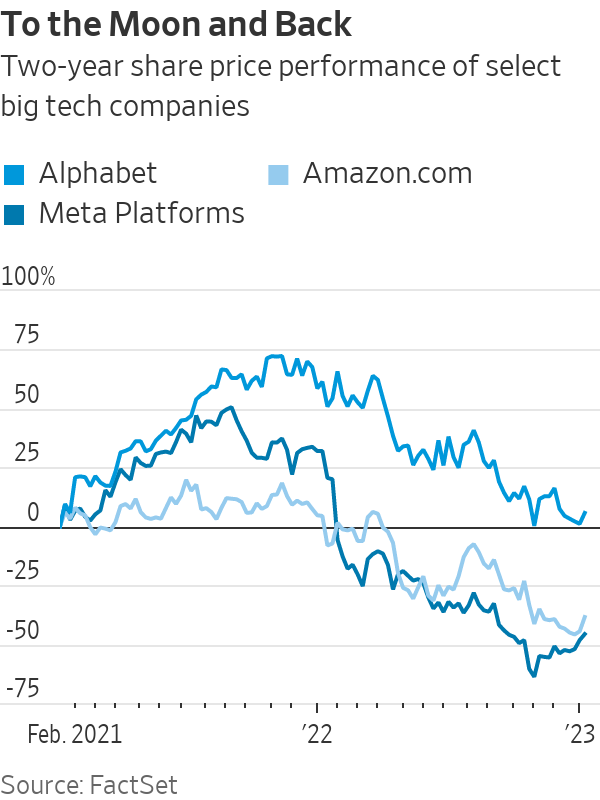

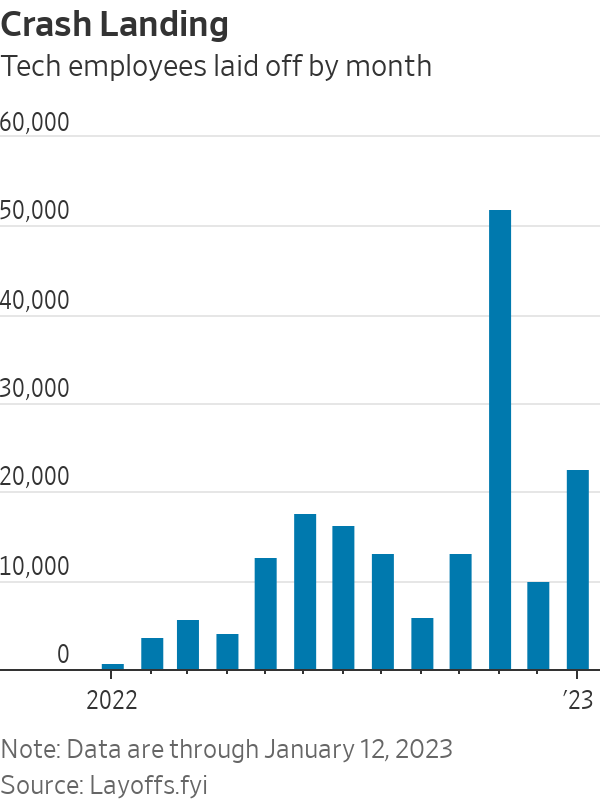

Stock charts both explain the change in boardroom sentiment and tell the story following an epic Covid-fuelled rise and fall. The tech-heavy Nasdaq fell 33% last year—its worst performance since 2008. Big tech, which spent the past several years spending on big dreams, is starting to think smaller. Last year more than 1,000 tech companies laid off employees, resulting in over 150,000 lost jobs, a tally by layoffs.fyi shows. It is an eye- popping number that could actually get worse: More than 23,000 tech workers have already been let go this year as of Jan. 13, the same tracker shows.

Many of these workers were newly hired under the mistaken assumption that booming pandemic demand would become the new normal. But a good percentage were legacy employees working on projects that, given today’s market environment, range from fiscally irresponsible to projects that fall well outside their parent company’s wheelhouse.

Meta Platforms and Amazon.com are the most high-profile examples, having cut a combined 29,000 workers so far. Meta is still reeling from an online advertising slump and the many billions of dollars that Chief Executive Officer Mark Zuckerberg is throwing at a new virtual world dubbed the metaverse. Amazon is coping with a retail slowdown in part by scaling back spending in unprofitable business areas such as its Alexa-controlled electronics products.

Meta Chief Technology Officer Andrew Bosworth said in an internal memo late last year that his company had “solved too many problems by adding headcount,” according to a recent newsletter published by the Verge. He reportedly added that headcount comes with overhead, which “makes everything slower.”

Despite its much-touted virtual ambitions, Meta said in a blog post last month that it is still devoting 80% of its total investment dollars to improving its own legacy business. In the Verge’s recent interview, Mr. Bosworth acknowledged that Meta is “changing our investment strategy” to the extent that some projects have to demonstrate value sooner to justify their high burn.

The ax also seems to be falling at the original moonshot factory: The Wall Street Journal reported that Google-parent Alphabet is laying off more than 200 employees at its Verily Life Sciences unit, plus another 40 at its robotics software company, Intrinsic. Both are part of Alphabet’s Other Bets segment, which racked up $5.9 billion in operating losses over the past four quarters while generating barely $1 billion in revenue.

Those cuts are unlikely to be the last at the Google parent, which added more than 30,000 new employees in the first nine months of 2022, even as its own advertising business started slowing.

Smaller tech companies are feeling the burn too. Redfin CEO Glenn Kelman told the Journal recently that if he could jump back in time 18 months, he would advise companies looking for profits to just “stop doing stupid stuff.”

He speaks from experience: The real-estate brokerage laid off 13% of its staff and shut down its automated home-flipping business late last year after deeming the operation too risky and expensive to continue. That followed a second quarter in which its so-called iBuying business had swelled to account for over 40% of its overall revenue. Channeling an old playbook for the new year, Mr. Kelman said in his company’s third-quarter report that Redfin “will have more cash and sell more properties” by focusing on its online audience and on better brokerage services.

Competitor Zillow gave up on its own iBuying business a year earlier than Redfin for similar reasons. It has since refocused on finding better ways to help its customers buy and sell other people’s homes. It is now using artificial intelligence to do such things as helping apartment hunters view available listings on New York City buildings they pass by and helping sellers generate floor plans for online listings based on photos. Zillow is also bundling its technology into an updated product to bolster traditional agents’ businesses.

A sector that has long worked to disrupt is now focusing on enhancing what already exists. In ride-share, Uber Technologies has now added taxi bookings to its platform in many cities, essentially feeding business to a competitor (but not without taking a small cut, of course). In Britain, Uber users can also book trains, buses and rental cars through its app. With Uber Explore, users across several cities can even book restaurant reservations and experiences.

Reinventing the wheel is so last year. The best tech investments of 2023 might be companies content to spend their coin greasing it.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The Federal Budget may have softened some of its proposed tax reforms, but it has exposed a bigger issue: too many families are relying on wealth structures that no longer reflect the realities of modern life.

3 min

For many Australians, the 2026 Federal Budget initially felt like a direct challenge to the way wealth is created, held and transferred between generations.

The headlines were immediate: changes to capital gains tax, reforms to discretionary trusts, restrictions on negative gearing and increased scrutiny of investment structures. Unsurprisingly, affluent families, business owners and investors began asking the same question:

Is the way we hold our wealth still fit for purpose?

In recent days, the government has announced several significant amendments following industry consultation and public feedback, including exempting testamentary trusts from the proposed 30 per cent minimum tax and expanding capital gains tax concessions for small businesses.

The backdown is welcome. But it also highlights something much bigger.

This Budget has accelerated a conversation that many Australian families have been postponing for years.

The conversation is not really about tax. It is about wealth stewardship.

For decades, Australians have built wealth through businesses, property, investments and careful long-term planning. Yet many families have not revisited the legal structures surrounding those assets in years, sometimes decades.

We often see clients who have spent years building significant wealth, only to discover their legal arrangements no longer reflect their current circumstances.

Their children are now adults. They may own multiple properties.

They may have sold a business, entered a second marriage, become grandparents or accumulated digital assets that did not exist when their original estate plans were prepared.

The trust that distributes income may need to be reconsidered. The bucket company may no longer be so attractive.

The Budget has simply exposed a reality that already existed: wealth structures cannot remain static while life continues to evolve.

Importantly, trusts themselves are not the issue.

Trusts are legitimate planning tools that provide flexibility, protection and continuity. When used appropriately, they allow families to adapt to changing circumstances over time.

And neither is tax the issue, really. Getting the fundamentals right is more important for long-term, sustainable wealth than a few favourable tax treatments around the edges.

The real issue is complacency.

Too often, families create structures and assume the job is done. It isn’t.

Estate planning is no longer a document you sign once and file away in a drawer. It is an ongoing process that should evolve alongside your life.

We are also seeing a broader shift in how Australians define wealth itself. It is no longer just the family home and an investment portfolio.

Modern wealth includes businesses, digital assets, cryptocurrency, intellectual property, frequent flyer points and increasingly complex family arrangements.

At the same time, Australians are living longer than ever before, meaning wealth may need to support multiple generations simultaneously. This creates new responsibilities and new risks.

How do you help your children enter the property market without exposing family wealth to relationship breakdowns?

How do you structure wealth so that it remains a source of opportunity rather than future conflict?

These are the questions families should be asking now.

The recent debate surrounding testamentary trusts also serves as an important reminder that policy decisions can have unintended consequences for vulnerable Australians. It is encouraging that the government has listened to feedback and clarified its position.

But the lesson remains: the wealth landscape is changing.

Increasingly, governments, regulators and tax authorities are paying closer attention to how wealth is held and transferred. That means families cannot afford to adopt a “set-and-forget” approach to their structures.

The families who will be best placed for the future are not necessarily those with the greatest wealth.

They are the families with the greatest clarity. Clarity around ownership, succession and governance. And clarity around how wealth will transition from one generation to the next.

Ultimately, preserving wealth is not about avoiding change.

It is about preparing for it.

Because the greatest risk is not change itself.

It is losing the ability to respond to it.

Anthony Hunt is Co-Founder of Wealth Lawyers and former COO of Westpac Private Bank. He advises business owners, investors and affluent Australian families on wealth protection, succession planning and intergenerational wealth transfer

Three-Michelin-starred chef Massimiliano Alajmo will host an intimate Mediterranean sailing aboard Crystal Serenity, redefining fine dining at sea.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.