Many Boards Are Playing Catch-Up on ESG and Green Issues

Company board directors say ESG efforts have brought about real benefits, but the political backlash has had an impact

5 min

5 min

Many corporate board directors aren’t confident about their ability—or their board’s—to oversee sustainability and social impact issues, even as companies pursue such goals and regulators want more disclosures on environmental, social and governance impact.

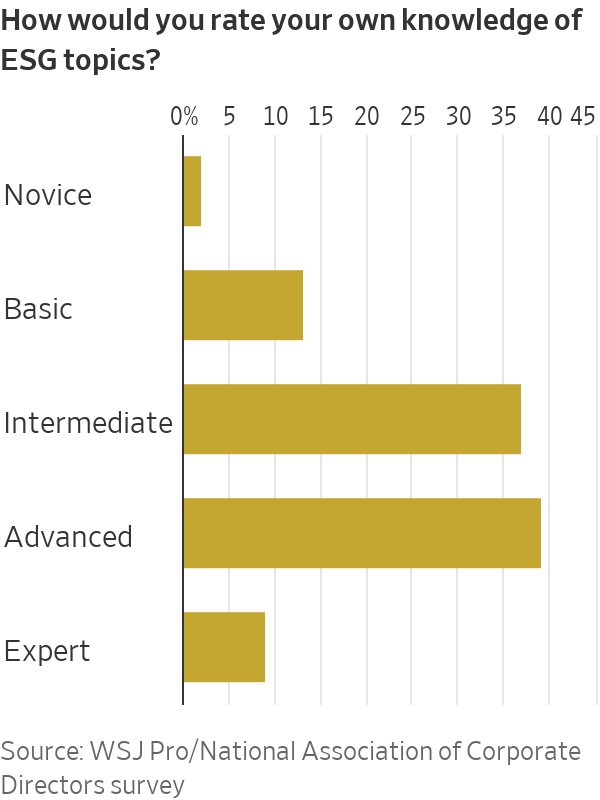

Eighty-three percent of directors surveyed said ESG topics were critical knowledge for directors, but less than half considered themselves to have “advanced” or “expert” level knowledge, according to a survey of board directors conducted in July by WSJ Pro in collaboration with the National Association of Corporate Directors.Directors of larger firms and listed companies expressed higher confidence, as did those in the energy industry.Respondents relied on external advisers to build their knowledge.

Other findings were that most believed sustainability efforts had brought real benefits and said ESG engagement with investors had been mostly positive. Directors also said the anti-ESG movement had an impact. They also reported that while about half of big companies had ESG targets—many linked to executive compensation—smaller, private companies lagged behind.

The survey’s 506 respondents covered a range of company sizes and included public, private and not-for-profit organizations from many sectors, with a concentration in financial services, industry, tech and energy. They said their ESG maturity level was across the spectrum: 4% self-identified as industry leaders, 27% as well developed, 36% as somewhat developed, 28% as early stage and 5% hadn’t started with ESG. Overall respondents rated their own ESG expertise slightly higher than that of their fellow board members.

Training up on sustainability

“As a board member, if you’re hoping that ESG is just a fad that will pass with time, we have enough data now from the last 2½ decades to know ESG is here to stay and boards need to be ready,” said Kristin Campbell, general counsel and chief ESG officer of Hilton Worldwide Holdings and board director at ODP and Regency Centers.

Campbell said boards must evaluate ESG as part of the company’s long-term strategy, otherwise activists, regulators, customers or someone else might do it for them, perhaps in a way that will be painful operationally or harmful to their reputation. “It’s that classic story of either you’re at the table or you’re on the menu,” said Campbell.

Alan Smith—responsible for the strategic management of the Church of England’s £10.1 billion (equivalent to $12.6 billion) perpetual endowment fund—said many boards had brushed up on ESG knowledge with in-house training, e-learning packages or advisers to run workshops. A former senior adviser at HSBC on climate and ESG risk and current First Church Estates Commissioner, Smith said he also found it helpful to see projects, such as offshore-wind farms, and speak to their operators in person.

“I think an integrated approach to board director education—of which one important part is getting on the ground and in the mud or on the boat—is very important,” he said.

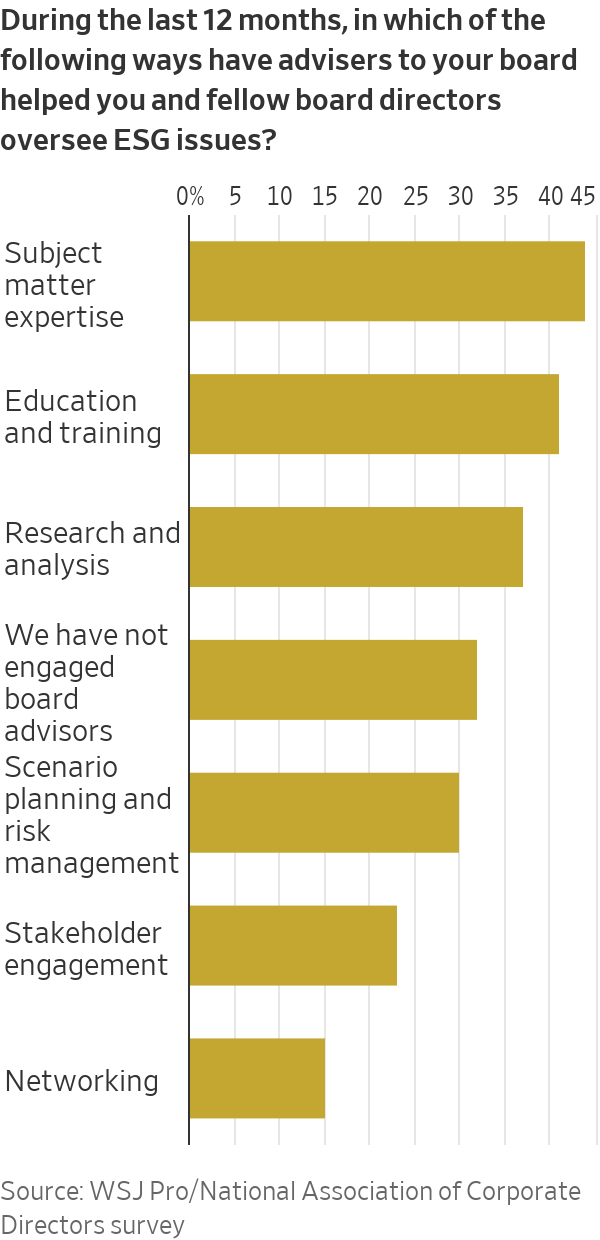

More than two thirds of directors said their organisations brought in external advisers to complement or build board’s ESG skills, with most advisers providing subject matter expertise (44%), education and training (41%), or research and analysis (37%).

“What we know about ESG will change today and will probably change tomorrow,” Hilton’s Campbell said. “It’s the job of an external adviser to know what’s going to happen next week and next year, which is useful in keeping the board ahead of the game.”

Stakeholder engagement

Overall, investors were the most influential stakeholders on board decisions related to ESG strategy, followed by company executives, regulators and customers. For public companies investors were most influential, followed by regulators, while directors of private businesses ranked their customers as top with investors in second place.

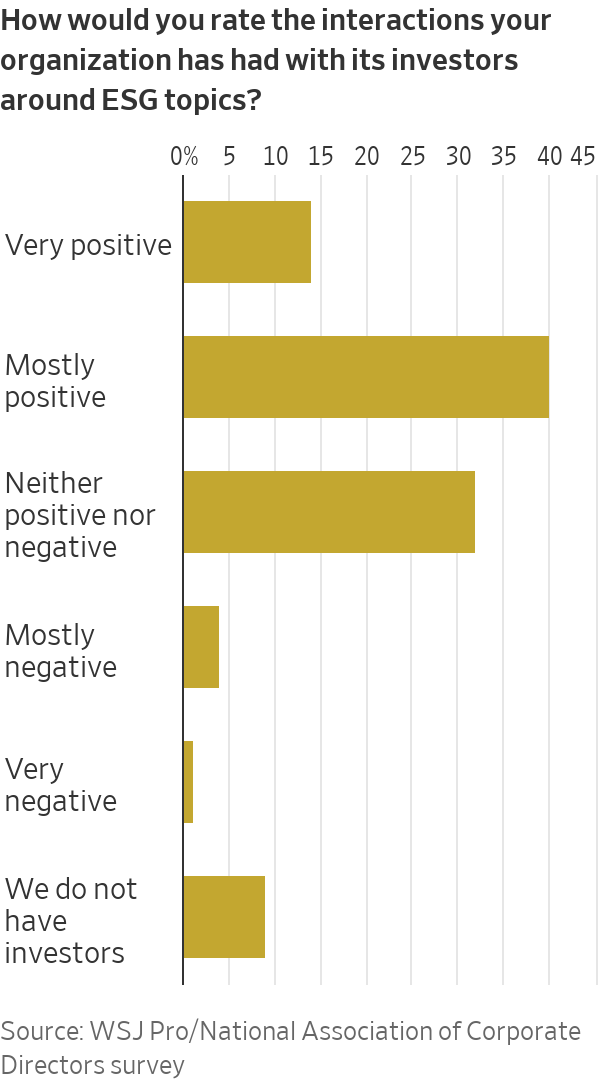

Respondents ranked their ESG-related interactions with investors as largely positive or neutral. Seventy-one percent of directors of organisations with investors said their largest ones had engaged with the board over the past 12 months on ESG topics.

However, public and private businesses approached this engagement quite differently. Private company investors most often engaged with the full board or directly with management, whereas public company investors worked most often with individual directors or sometimes with the full board, but rarely with management.

Anti-ESG impact

The survey also examined the impact of the rising anti-ESG movement in the U.S. Many boards started their ESG journey in 2020, but, particularly in the last six to 12 months, the extent of the political backlash in the U.S. has made it more complicated, said Smith. “You had a wind that was giving companies and boards energy, and now you have a countervailing wind of political backlash,” Smith said.

As the pressure has mounted, there have been numerous reports of green-hushing—when a company scales back what it says about its climate and social initiatives in corporate communications. The survey found evidence to support this: 7% of directors said their company no longer publicly communicates about its ESG activities, and 14% said their board and management no longer use the term ESG when referring to relevant activities.

Respondents report substantive changes too. One in five said their companies are reassessing their approach to ESG, 12% said they have deprioritised ESG as a critical business issue, and 15% of directors, primarily in smaller private businesses, believe ESG is negatively affecting their business decisions and strategy.

Despite those changes, half of respondents believe ESG will continue to be an important driver of their business decisions and strategy. Nearly as many say their board and management remain committed to ESG as an opportunity for growth and a driver of long-term risk reduction.

Driving ESG performance

While most respondents said ESG is critical knowledge for directors, only 37% of their organisations have set a climate-impact reduction target, although that was 54% for large organisations. Nine out of 10 of those companies with a target said their boards monitored their progress toward those goals and four out of five believed they were achievable.

To encourage management to hit targets, over one quarter of respondents said their company had linked executive pay to ESG goals, and a further 29% were considering doing so in the next 12 months.

“If we’re going to be more serious about ESG and building it into a company’s long-term strategy then I think it needs to be tied to executive compensation like any other [key performance indicator],” Campbell said.

Nearly a fifth of directors surveyed said reducing the impact of climate change is a priority regardless of financial performance. Almost half said it is a priority but not at the cost of financial performance, while the remaining third said it isn’t a priority at all.

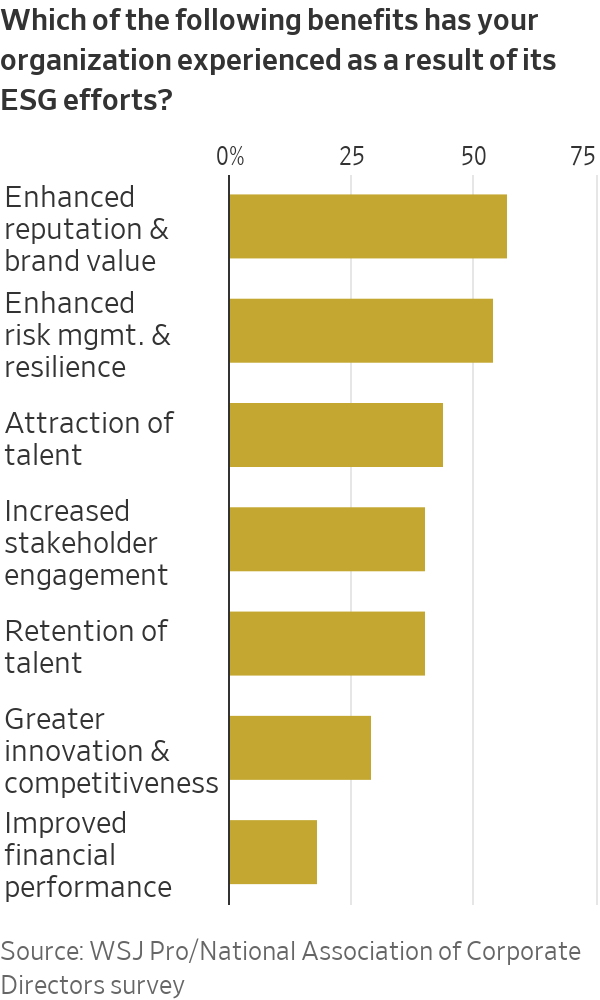

Many directors report real benefits from their ESG efforts. In particular it has enhanced their company’s reputation and brand value (57%), risk management and resilience (54%), and ability to attract and retain talent (44% and 40%, respectively).

Climate change was talked about more frequently in 43% of the boardrooms, while in 31% it actually decreased. The topic was discussed at most or every board meeting for 29% of respondents, 36% said it came up at some meetings, and 23% said it was rarely talked about. Only 11%—primarily small, private companies—hadn’t discussed it at all.

Smith said it was particularly important for smaller companies to keep climate change front of mind: “Those that say they aren’t doing anything yet are paradoxically the ones that may be hit first because they’re downstream of big companies setting more immediate net zero carbon neutral targets.”

As well as calling it a business differentiator for small businesses, Smith said a focus on climate impact reduction was “a survival mechanism.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

Limited to 630 units, Lamborghini’s latest Urus Capsule pushes personalisation further than ever, blending hybrid performance with over 70 bespoke design combinations.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

3 minFor decades, Australia has leaned into its reputation as the lucky country. But luck, as it turns out, is not an economic strategy.

What once looked like resilience now appears increasingly fragile. Beneath the surface of rising property values and steady headline growth, the Australian economy is showing signs of strain that can no longer be ignored.

Recent data paints a sobering picture. Australia has recorded one of the largest declines in real household disposable income per capita among advanced economies.

Wages have failed to keep pace with inflation, meaning many Australians are working harder for less. On a per capita basis, income growth has stalled and, at times, reversed.

And yet, on paper, things still look relatively solid. GDP is growing. Unemployment remains low. But that growth is increasingly being driven by population expansion rather than productivity.

More people are contributing to output, but not necessarily improving living standards.

That distinction matters.

For years, Australia’s economic success rested on a powerful combination: a once-in-a-generation mining boom, a credit-fuelled housing market, strong migration and a property sector that rarely faltered. Between 1991 and 2020, the country avoided recession entirely, building enormous wealth in the process.

But much of that wealth is tied to property. Around two-thirds of household wealth sits in real estate, inflated by leverage and sustained by demand. It has worked, until now.

The problem is the supply side of the economy has not kept up.

Housing supply is falling behind population growth. Rental vacancies are near record lows.

Construction firms are collapsing at an elevated rate. At the same time, massive infrastructure pipelines are competing with residential projects for labour and materials, pushing costs higher and delaying delivery.

The result is a system under pressure from all angles.

Despite near full employment, productivity growth has stagnated for years. In simple terms, Australians are putting in more hours without generating more output per hour. The economy is running faster, butgoing nowhere.

Meanwhile, government spending continues to expand. Public debt is approaching $1 trillion, with spending now accounting for a record share of GDP.

The gap between spending and revenue has been filled by borrowing for decades, adding further pressure to an already stretched system.

This is where the uncomfortable question emerges.

Has Australia become too reliant on a model driven by rising property values, expanding credit and population growth?

As asset prices rise, households feel wealthier and borrow more. Banks lend more. Governments collect more revenue. Migration fuels demand. The cycle reinforces itself.

But when productivity stalls and debt outpaces real income, the system begins to depend on constant expansion just to stay stable.

It is not a collapse scenario. But it is not particularly stable either.

Nowhere is this more evident than in housing.

The National Housing Accord targets 1.2 million new homes over five years, yet current completion rates are well below that pace. With approvals falling and construction costs rising, the gap between supply and demand is widening, not narrowing.

Housing is also one of the largest contributors to inflation, with costs rising sharply across rents, construction and utilities. Yet the private sector, from small investors to major developers, is struggling to make projects stack up in the current environment.

This brings the policy debate into sharper focus.

Tax settings such as negative gearing and capital gains concessions have undoubtedly boosted demand over the past two decades. But they have also supported supply. Removing them may ease prices briefly, but risks deepening the supply shortage over time.

That is the paradox.

Policies designed to make housing more affordable can, in practice, make the shortage worse if they discourage development. The optics may appeal, but the economics are far less forgiving.

It is also worth remembering that most property investors are not institutional players. The majority own just one investment property. They are, in many cases, ordinary Australians using real estate as their primary wealth-building tool.

Undermining that system without replacing it with a viable alternative risks unintended consequences, from reduced supply to higher rents and increased inflation.

So where does that leave Australia?

At a crossroads.

The country can continue to rely on population growth and rising asset prices to drive economic activity. Or it can shift towards a model built on productivity, innovation and sustainable growth.

The latter is harder. It requires structural reform, long-term thinking and political discipline.

But it is also the only path that leads to genuine, lasting prosperity.

The question is no longer whether Australia has been lucky.

It is whether it can evolve before that luck runs out.

Paul Miron is the Co-Founder & Fund Manager of Msquared Capital.

Powerhouse real estate couple Avi Khan and Kaylea Sayer welcome their daughter while balancing record-breaking careers, proving success and family can grow side by side.

Records keep falling in 2025 as harbourfront, beachfront and blue-chip estates crowd the top of the market.