Well Into Adulthood and Still Getting Money From Their Parents

Nearly 60% of parents provide financial help to their adult kids, a new study finds

4 min

4 min

Parents have always supported their children into adulthood, from funding weddings to buying a home. Now the financial umbilical cord extends much later into adulthood.

About 59% of parents said they helped their young adult children financially in the past year, according to a report released Thursday by the Pew Research Center that focused on adults under age 35. (This question hadn’t been asked in prior surveys.) More young adults are also living with their parents. Among adults under age 25, 57% live with their parents, up from 53% in 1993.

Parental support is continuing later in life because younger people now take longer to reach many adult milestones—and getting there is more expensive than it has been for past generations, economists and researchers said. There is also a larger wealth gap between older Americans and younger ones, giving some parents more means and reason to help. In short, adulthood no longer means moving off the parental payroll.

“That transition has gotten later and later, for a lot of different reasons. Now it’s age 25, 30, 35, 40,” said Sarah Behr, founder of Simplify Financial Planning in San Francisco.

Kami Loukipoudis, a 39-year-old director of design, and husband Adam Stojanik, a 39-year-old high-school teacher, knew they would need parental assistance to buy in New York’s expensive home market.

“We could pay a mortgage, but that down payment was the absolute crusher,” Stojanik said. “The idea of trying to save up on our own—as long as we were paying rents in NY, would’ve taken 300 years.”

Loukipoudis’s mother gave them the money for a 10% down payment on a two-bedroom apartment in the New York borough of Queens.

The young-adult allowance

Adult children aren’t necessarily getting larger checks from their parents, but they are staying on the parental payroll for longer than previous generations, according to Marla Ripoll, professor of economics at the University of Pittsburgh who studied the trend by analysing payments from parents to adult children over a 20-year span.

Ripoll found that 14% of adult children receive a transfer of money from their parents at least once in any given year, and roughly half get financial help at some point within that period. Those rates have been stable for years. What has changed is that the transfers now continue for much longer, she found. This longer-term help might be a drag on social mobility, as it becomes even harder for young people from lower-income families to catch up, researchers said.

Of the young adult children who said they received financial help from a parent in the past year, most said they put it toward day-to-day household expenses, such as phone bills and subscriptions to streaming services like Netflix, according to the Pew survey.

The amount of money and the frequency of help varies by age; those on the older end of the 18-to-34 cohort are far likelier to say they are completely financially independent from their parents compared with younger adult children, as many in the latter group are completing their education. Nearly a third of young adult children between the ages of 30 and 34 say they still get parental help.

Heather McAfee, a 33-year-old physical therapist in Austin, Texas, said she lived at home between 2019 and 2021; otherwise she wouldn’t have been able to make progress paying down her student loans while rent prices in her area remained so high. The plan worked—she has since reduced her student-debt balance from $83,000 to $15,000.

“It helped tremendously,” she said. “I didn’t have to take out more loans to pay for apartment living or anything like that. That stress was gone.”

Setting limits on financial help

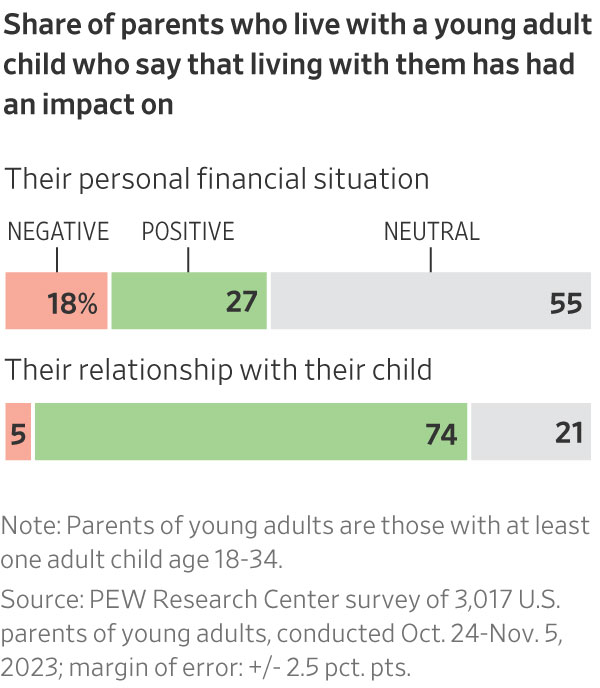

A little more than half of parents surveyed said that having their adult children home brought them closer together or improved their relationship, but nearly 20% said it dented their personal finances.

Financial advisers often find themselves in the tricky position of speaking to both ends of the equation: adult children who need assistance and the parents determined to help children well into middle age, within limits.

Whereas previous generations would step into a greater sense of financial independence in their early 20s, young adult children today are often unable to reach similar markers of such independence—living on their own or buying their first home, for example—without greater financial resources.

Families typically don’t set concrete rules around when financial help will happen and what the money is used for, which can result in surprises down the road, Behr said.

In one case, Behr’s clients received the down payment they needed to purchase a condo from a generous mother-in-law. Years later, that same mother-in-law told them she expected a payout once the couple sold the home.

The hand-me-down payment

Down-payment help from parents—a given for many first-time home buyers—is growing thanks to higher home prices and elevated mortgage rates.

About a fifth of first-time home buyers said they got help from a relative or friend when pulling together the money needed for a down payment, according to a 2023 survey of home buyers and sellers from the National Association of Realtors. And 38% of home buyers under age 30 received help with the down payment from their parents, according to a survey this spring by Redfin.

Wealthy families often go further than helping with the down payment. They become a true bank of mom and dad and write a mortgage. The Internal Revenue Service sets minimum levels of interest for such loans, which remain significantly cheaper than current mortgage rates.

Timothy Burke, chief executive at National Family Mortgage, which facilitates such loans, said parents are often frustrated on behalf of their house-hunting children. High interest rates and the cutthroat housing market are holding their children back from reaching a milestone the parents themselves were more easily able to access.

Mei Chao, a 41-year-old stay-at-home mom, and her husband, William Chao, a 44-year-old information-technology specialist, bought their first house as a couple in 2017. They relied on financial help from her husband’s two sisters and his mother to help them bridge a gap in their house-buying timeline. While they waited to sell William’s Manhattan condo, they used the money from the family to purchase the new house in Queens.

The structure of the agreements got tricky. After selling the condo in Manhattan, Mei and her husband were able to repay his sisters in full. But they didn’t have enough money left over from the sale to do the same for Mei’s mother-in-law. So they kept the mother-in-law’s name on the deed to the house—a concession Mei said they were both more than happy to make.

“Ultimately, it all worked out. I’m glad his mother pushed us,” Mei said. “Without her help, I could not say we would have this home.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The Federal Budget may have softened some of its proposed tax reforms, but it has exposed a bigger issue: too many families are relying on wealth structures that no longer reflect the realities of modern life.

3 min

For many Australians, the 2026 Federal Budget initially felt like a direct challenge to the way wealth is created, held and transferred between generations.

The headlines were immediate: changes to capital gains tax, reforms to discretionary trusts, restrictions on negative gearing and increased scrutiny of investment structures. Unsurprisingly, affluent families, business owners and investors began asking the same question:

Is the way we hold our wealth still fit for purpose?

In recent days, the government has announced several significant amendments following industry consultation and public feedback, including exempting testamentary trusts from the proposed 30 per cent minimum tax and expanding capital gains tax concessions for small businesses.

The backdown is welcome. But it also highlights something much bigger.

This Budget has accelerated a conversation that many Australian families have been postponing for years.

The conversation is not really about tax. It is about wealth stewardship.

For decades, Australians have built wealth through businesses, property, investments and careful long-term planning. Yet many families have not revisited the legal structures surrounding those assets in years, sometimes decades.

We often see clients who have spent years building significant wealth, only to discover their legal arrangements no longer reflect their current circumstances.

Their children are now adults. They may own multiple properties.

They may have sold a business, entered a second marriage, become grandparents or accumulated digital assets that did not exist when their original estate plans were prepared.

The trust that distributes income may need to be reconsidered. The bucket company may no longer be so attractive.

The Budget has simply exposed a reality that already existed: wealth structures cannot remain static while life continues to evolve.

Importantly, trusts themselves are not the issue.

Trusts are legitimate planning tools that provide flexibility, protection and continuity. When used appropriately, they allow families to adapt to changing circumstances over time.

And neither is tax the issue, really. Getting the fundamentals right is more important for long-term, sustainable wealth than a few favourable tax treatments around the edges.

The real issue is complacency.

Too often, families create structures and assume the job is done. It isn’t.

Estate planning is no longer a document you sign once and file away in a drawer. It is an ongoing process that should evolve alongside your life.

We are also seeing a broader shift in how Australians define wealth itself. It is no longer just the family home and an investment portfolio.

Modern wealth includes businesses, digital assets, cryptocurrency, intellectual property, frequent flyer points and increasingly complex family arrangements.

At the same time, Australians are living longer than ever before, meaning wealth may need to support multiple generations simultaneously. This creates new responsibilities and new risks.

How do you help your children enter the property market without exposing family wealth to relationship breakdowns?

How do you structure wealth so that it remains a source of opportunity rather than future conflict?

These are the questions families should be asking now.

The recent debate surrounding testamentary trusts also serves as an important reminder that policy decisions can have unintended consequences for vulnerable Australians. It is encouraging that the government has listened to feedback and clarified its position.

But the lesson remains: the wealth landscape is changing.

Increasingly, governments, regulators and tax authorities are paying closer attention to how wealth is held and transferred. That means families cannot afford to adopt a “set-and-forget” approach to their structures.

The families who will be best placed for the future are not necessarily those with the greatest wealth.

They are the families with the greatest clarity. Clarity around ownership, succession and governance. And clarity around how wealth will transition from one generation to the next.

Ultimately, preserving wealth is not about avoiding change.

It is about preparing for it.

Because the greatest risk is not change itself.

It is losing the ability to respond to it.

Anthony Hunt is Co-Founder of Wealth Lawyers and former COO of Westpac Private Bank. He advises business owners, investors and affluent Australian families on wealth protection, succession planning and intergenerational wealth transfer

Here’s how they are looking at artificial intelligence, interest rates and economic pressures.

MAISON de SABRÉ’s new Spring Harvest Collection turns everyday produce into collectible leather charms and introduces fresh silhouettes in its cult Bucket bag family.