A Gilded Age Is Fading for Luxury Brands

The latest results from Louis Vuitton owner LVMH show that luxury shoppers are sobering up after years of heavy spending

3 min

3 min

The end of easy money is catching up with luxury brands. It took a long time, so the skills needed to protect their profit margins may be a bit rusty.

Shares in the world’s biggest luxury company, LVMH Moët Hennessy Louis Vuitton, fell 6% Wednesday after it reported a slowdown in sales for the third quarter the previous evening. LVMH grew sales by 9% for the three months through September compared with a year ago. That sounds impressive, but the business was growing at almost double this pace in the second quarter.

Demand for luxury goods has slowed for most products and in all major regions. One surprise was a 14% drop in sales at LVMH’s wines and spirits divisions. Shipments of cognac brands such as Hennessy have been weak in the U.S. all year as cash from pandemic stimulus checks runs out, but the trend is getting worse.

The slowdown is no longer limited to “aspirational” shoppers, as the industry lingo frames less wealthy buyers. Sales of LVMH’s expensive watch and jewellery brands were weaker than analysts expected. And wealthy European consumers who were spending freely on luxury goods early this summer turned cautious in the third quarter.

Investors knew that a slowdown was coming, but not how big it would be. After Wednesday’s share-price drop, LVMH has lost a quarter of its market value in roughly six months. The slump may be more severe at weaker rivals like Burberry or Gucci owner Kering, whose stocks also fell Wednesday. Recently, the entire luxury industry has fallen out of fashion with shareholders, who at the start of the year expected a bigger surge in Chinese demand after the country lifted all pandemic restrictions.

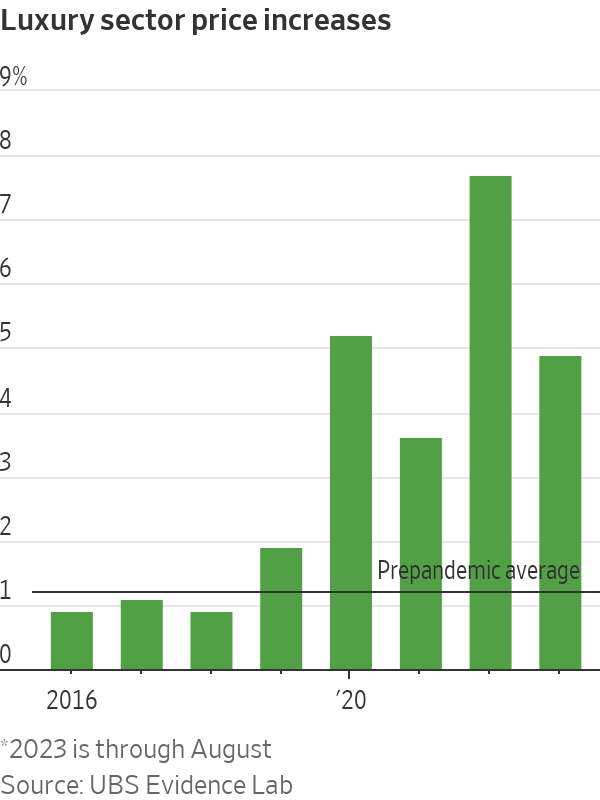

With business probably as good as it can get in China, there is no obvious place the industry can turn to for new growth. Weaker demand for luxury goods will damp brands’ ability to raise prices. Last year, exceptionally strong sales helped them lift prices by 8% on average, according to UBS estimates. This pricing power has been a big draw for investors, and boosted profit margins, but it is probably over for now. In the four years leading up to the pandemic, prices rose only 1.2% annually on average.

Luxury companies face a balancing act with their multibillion-dollar advertising budgets and store-rollout plans. They may need to save cash to protect margins. At the same time, they must continue to spend on advertising to maintain their trademark desirability.

Some perspective is necessary, though: Today, LVMH’s fashion-and-leather-goods division, its main profit driver, is 80% larger than it was in the third quarter of 2019, before the pandemic. The industry has had an amazing run and is expected to grow in 2024. Still, some of the sheen that made it particularly attractive to investors in recent years has faded.

Last month, LVMH was even dethroned as Europe’s most valuable company by Novo Nordisk, the Danish pharmaceutical company behind weight-loss drug Ozempic. Leaner times ahead.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

From office parties to NYE fireworks, here are the bottles that deserve pride of place in the ice bucket this season.

Australia’s housing market rebounded sharply in 2025, with lower-value suburbs and resource regions driving growth as rate cuts, tight supply and renewed competition reshaped the year.