As Generation X Approaches Retirement, Reality Still Bites

The ‘forgotten generation,’ born between 1965 and 1980, launched their careers at the start of a massive shift in how Americans work.

7 min

7 min

The oldest members of Gen X are turning 60 next year. Many can’t afford to stop working any time soon.

Born between 1965 and 1980, Gen Xers launched their careers at the start of a massive shift in how Americans work. Companies moved from pensions that promise steady income after years of service, to plans such as 401(k)s that place employees’ retirement destiny in their own hands.

Some Gen Xers were hit hard in their prime working years during the 2008 financial crisis. Others are still paying off student debt. Their children are increasingly living at home well into adulthood, while their own aging parents often require care. Few believe they can rely on Social Security to make ends meet later in life.

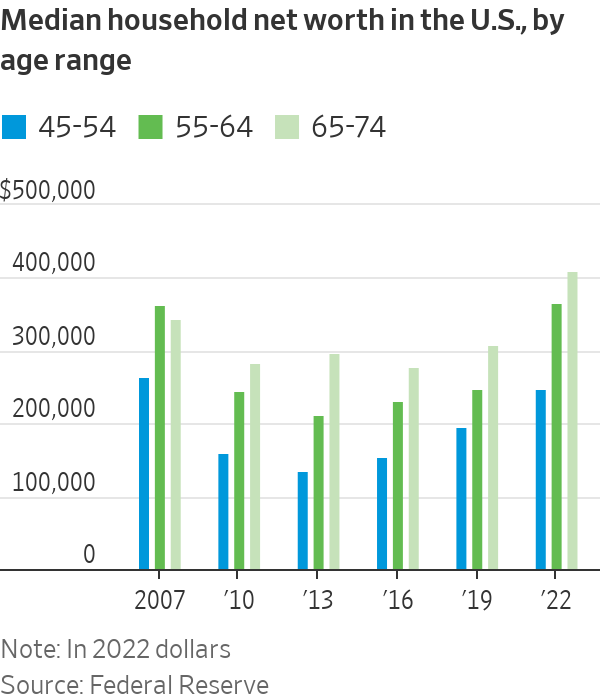

By some measures, Gen Xers are worse off financially than their baby boomer predecessors. The median household net worth of Gen Xers between 45 and 54 years old was about $250,000 in 2022, about 7% lower than that of baby boomers at the same age in 2007, according to inflation-adjusted Federal Reserve data. That was the only age group that experienced a drop in median wealth over the 15-year period.

David Bryan, 55, earns about $35,000 a year as a school-bus driver and lives on Tybee Island, Ga. He doesn’t own property and has about $100,000 in retirement savings from his previous jobs as a railroad conductor and a researcher at a college foundation.

It’s a different life than that of his parents, who worked for decades for the sheriff’s department and the post office and received steady pension checks when they retired.

“As long as my body will let me, it’s better I keep working,” said Bryan.

The roughly 65 million Americans in Gen X are sometimes referred to as the “forgotten generation,” sandwiched between the larger and louder baby boomer and millennial generations. They are also called the “latchkey generation,” often coming home from school as children to an empty house. Goldman Sachs Asset Management in a recent report called Gen X the “‘401(k) experiment’ generation.”

For decades, employers often supported loyal workers in old age through traditional pensions with set payouts for life. The advent of the 401(k) system pushed the responsibility on to the individual—and Gen X was caught squarely in the transition.

“Gen X is the first generation where they were mostly expected to figure out their retirement on their own,” said Jeremy Horpedahl , an economics professor at the University of Central Arkansas and director of the Arkansas Center for Research in Economics.

The early champions of the 401(k) never thought that it would become the dominant way most Americans save for retirement. It is named for a line in the tax code changed in 1978 that gave executives a tax-free way to defer compensation from bonuses or stock options. Human-resources executives and economists jumped on the 401(k) as a way to encourage saving for rank-and-file employees.

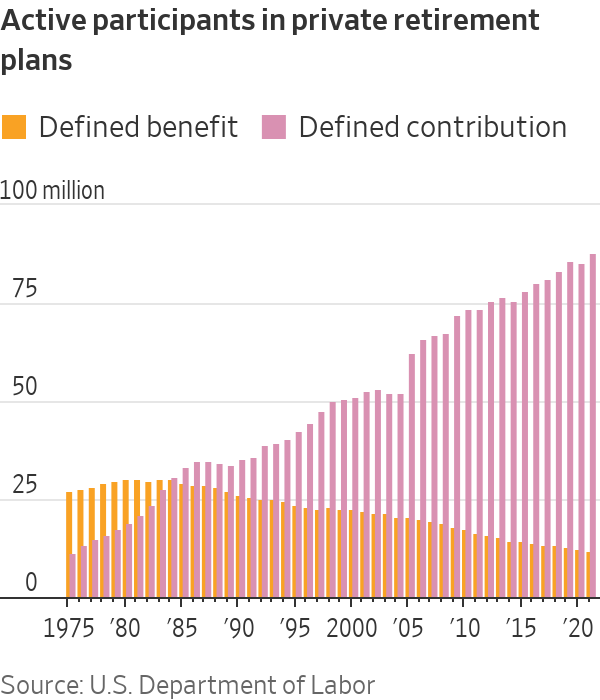

By the mid-1980s, the number of active participants in defined-contribution retirement plans—such as 401(k)s—overtook those in defined-benefit plans—such as traditional pension plans—in the private sector. Now, private pensions are rare.

When Gen Xers entered the workforce, the 401(k) was a new concept. Features such as automatically enrolling employees in a workplace plan and automatically increasing contributions every year didn’t become commonplace until later.

Other common private retirement savings tools were also introduced in the last half-century. The individual retirement account—a tax-deferred investment vehicle—was authorised in 1974, while the Roth IRA—funded with posttax money, but tax-free when withdrawn—was established in 1997.

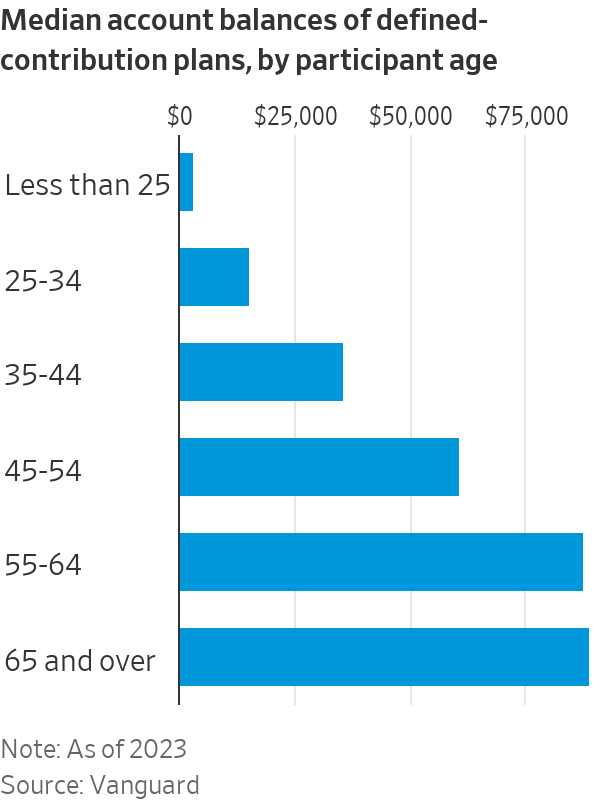

Gen Xers between 45 and 54 years old had a median account balance of roughly $60,000 in defined-contribution retirement plans at Vanguard Group in 2023, according to the firm. For most Americans, that is well below the target some financial experts recommend of having roughly six times one’s salary saved for retirement by age 50.

John Kotrides, a 54-year-old living near Charlotte, N.C., had contributed to 401(k)s ever since he started his career in banking about three decades ago. But whenever he moved to a different employer, he usually cashed out his 401(k) because there was a more urgent expense, such as a home repair or moving costs.

Keeping the money invested in the stock market didn’t seem worth it after witnessing crashes like the bursting of the dot-com bubble. Retirement seemed far away.

“You no longer have a generation of people whose employer took you from your first job into your retirement,” he said. “When we were offered 401(k)s, I don’t think that was a great deal.”

Kotrides says he doesn’t have much in retirement assets, besides the home he owns, where he lives with his wife and two daughters, who are 12 and 20 years old. After quitting his job as a mortgage lender during the pandemic, he now works as a bartender part-time and earns most of his money making social-media content, mostly nostalgic videos about the 1970s through 1990s. He likes having more time to spend with his family.

“This is basically my retirement plan,” he said. “I truly assume that I’ll continue to work to provide for my family as long as I need to.”

Even those who have benefited from the 401(k) system say it hasn’t been easy.

Scott Zibel, a 56-year-old in Leominster, Mass., started putting money in a 401(k) when he began working at a grocery store at 15. His father encouraged him to contribute. The account grew as he continued working at the store through college and became a manager. In his early 30s, he became an English teacher and expects to receive a pension after retiring.

When the stock market crashed in 2020 at the onset of the Covid pandemic, he and his wife pulled the money in his wife’s 401(k) out of the market and into a money-market fund. Now they have reinvested the money, but put a greater portion of it into bonds than before.

“I’m grateful for the 401(k), but there’s no guarantees as well,” he said, estimating his household retirement savings at a little over $1 million.

Zibel feels prepared for retirement but says he has to live frugally to save. He has driven the same car for 12 years and has avoided pricey expenses such as new carpeting for his 30-year-old home.

“My wife and I have done so much planning for the future with our money, it’s made living in the now difficult,” he said.

For some Gen Xers, the 2008 financial crisis was a hit that took years to recover from.

Around 2007, Darling “Diva” Moore was at the peak of her career as a managing partner at a title company in West Palm Beach, Fla. Then the housing market collapsed and her company went under. She couldn’t make rent on her apartment and had to crash with her significant other at the time, sometimes turning to sleeping on the beach or in the car.

“The Great Recession changed everything for us,” said Moore, who is 57. “After that, I don’t know how many Gen Xers trusted that system.”

After settling in Denver, more than two years went by before she landed a new job. She went back to school, getting an online bachelor’s degree in business management and master’s degree in human relations and organisation development. Now she is self-employed as a career counsellor.

As she is approaching her 60s, Moore is trying to locate money she contributed to various 401(k)s from jobs earlier in her career. Whenever she switched jobs, she didn’t rollover her balance to an IRA or new 401(k), so those accounts are scattered across plan providers. “In the ‘90s, they didn’t make it easy to find out where that money is,” she said.

She is also contending with student debt from a for-profit associates-degree program she completed in her 20s that has swelled to nearly $90,000 from around $27,000 due to interest.

More than a quarter of U.S. households led by Gen Xers between the ages of 45 and 54 had education loans in 2022, compared with about 15% of baby boomers at the same age in 2007, according to Fed data.

Soaring tuition costs, sky-high rents and other inflationary pressures for Gen Z are also Gen X’s problem. Many Gen Xers have forked over tens of thousands of dollars for their children to attend college. Young people are also increasingly living with parents, or relying on them for financial support, well into adulthood .

Pamela Likos’s 21-year-old son lives at home with her in the suburbs of Madison, Wis., while another son and daughter are at college.

“My kids are still definitely not grown and flown,” Likos said.

Some Gen Xers are simultaneously caring for aging parents, who are living longer than previous generations.

Likos isn’t in that situation yet, but her stepmother, who has Alzheimer’s, and her father are in their 80s.

“I need my parents to hang on healthwise for another five to 10 years because we are not ready to help financially, really,” she said.

Likos, who is 54, was the first person in her family to go to college, but didn’t work for about two decades after she got married and became a stay-at-home mom. When she got divorced about seven years ago, she found herself with no savings of her own and no resume to apply for jobs. She got a license to work as an esthetician for a few years and now is remarried. From her divorce, Likos received about half of her ex-husband’s 401(k), which comprises most of her plan for retirement.

The youngest members of Gen X are in their mid-40s, offering more time to boost savings ahead of retirement. Tyler Bond, the research director at the National Institute on Retirement Security, wonders if there will be diverging retirement experiences between the older and younger ends of the cohort.

“The older Gen Xers simply may not have time,” he said.

Avery Nesbitt, a 44-year-old operations manager in the Atlanta area, isn’t waiting for retirement to go on nice vacations or buy a new car because he wants to enjoy them now—and he doesn’t expect to be able to save up a cushy nest egg for later in life. If the Covid pandemic taught him anything, it was that anything can happen.

He and his wife have contributed modestly to employer-sponsored retirement accounts but didn’t feel like they could afford to save more. They own a home, where they live with their two children. That makes up the bulk of their wealth. He said he has put more money into life-insurance policies than in retirement accounts.

“I fully expect to work until I die,” Nesbitt said. “It is what it is.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

The voices reshaping how Australians think about money — and why credibility matters more than reach.

6 min

The best financial advice many Australians are receiving right now is not coming from licensed advisers charging by the hour. It is coming through a phone screen, in the ten minutes between work and dinner, from creators who have built credibility the hard way: by being right, being transparent, and being specific in a space where vagueness has always been the easy default.

This is not a ranking by follower count. Follower count is a measure of distribution, not of quality. What follows is a ranking by substance — credentials, accuracy, community depth, and the quality of what an audience actually learns from following these accounts. The distinction matters, because the Australians acting on this content are making real financial decisions with real money.

1- Queenie Tan – Corporate Authorised Representative; Co-Founder & Director, Invest With Queenie & Billroo

There are finance influencers who talk about building wealth, and there are those who document it in real time with receipts. Queenie Tan belongs firmly in the second category. Starting from a $400-per-week income, Tan built her net worth past $1 million while publishing the actual numbers — income, savings rate, investment decisions — for an audience of more than 400,000 across platforms.

She is a Corporate Authorised Representative, co-founder of the personal finance app Billroo, and the author of a book that has become a practical reference for young Australians navigating ETFs, superannuation and property. What separates her from the crowded field of money educators is precision: she does not talk in principles when she can talk in percentages.

2- Alan Kohler – Editor-in-Chief, Eureka Report; Editor-in-Chief, InvestSMART Group; ABC News finance presenter, host of Inside Business.

If Queenie Tan represents the new wave of personal finance creators, Alan Kohler represents something the new wave will spend decades trying to build: institutional credibility that has survived multiple economic cycles. As Editor-in-Chief of the Eureka Report and InvestSMART Group, and a decades-long presence on ABC News, Kohler has spent more than thirty years making financial analysis accessible without dumbing it down.

His coverage of RBA decisions, market movements and economic policy is cited by podcasters, journalists and fund managers alike. He is not chasing virality. He does not need to.

3- Aleks Nikolic – Corporate lawyer; host, Big Swinging Stocks podcast

Most finance creators address the mechanics of money. Aleks Nikolic addresses the psychology — and that distinction explains why her following is as loyal as it is. Operating as Broke Girl Wealth across Instagram, TikTok and YouTube, Nikolic covers ETFs, crypto and investment strategy, but her real differentiator is a willingness to discuss the emotional architecture of financial decision-making.

Shame around debt. Fear around market volatility. The limiting beliefs that stop people acting on what they already know. In a space where confidence is routinely performed, her candour is a genuine competitive advantage.

4- Bryce Leske & Alec Renehan – Equity Mates Media

Equity Mates did not build a following. They built a media company. What began as a podcast by two friends learning to invest has grown into Australia’s most established investing media brand, covering ASX stocks, ETFs, global markets and fund manager interviews across podcast, social and YouTube.

The longevity is the credential. Equity Mates has operated through multiple market cycles, a global pandemic, and a generational shift in how Australians engage with investing — and its audience has grown through all of it. When the hosts speak, their listeners know they have been paying attention for years.

5- The Lazy CEO – CEO & Founder, Showpo; Shark Tank Australia investor

The metric that matters most on social media is not followers — it is engagement, because engagement signals trust. Jane Lu, known as The Lazy CEO, maintains an engagement rate of approximately 1.15 per cent on Instagram, which is exceptional for a finance account of his size. Her 242,000-plus followers are not passive consumers: they ask questions, share experiences and apply what they read.

Her content focuses on business finance and wealth building, and the active comment sections are the clearest possible evidence that her audience does not merely scroll past.

6- Tash Invests – Founder, Tash Lends; Forbes Australia 30 Under 30

Tash Invests built her following on a premise that sounds simple but is rarer in practice than it should be: she publishes the actual numbers. Not approximations or ranges or anonymised case studies — her salary, her savings rate, her portfolio value, her net worth, updated and on the record.

Having bought her first property at twenty-two and grown her documented net worth past $1 million, she has become the primary reference point for young Australians trying to understand what building wealth on a moderate income genuinely looks like. The specificity is the product.

7- David Scutt – APAC Market Analyst at StoneX Group

The authority of most finance social media content rests on research and reading. David Scutt‘s authority rests on having done the job. A former Treasury Dealer at Arab Bank and the Commonwealth Bank, former ASX Business Supervisor, and former Global Markets Editor at Business Insider Australia and anchor at ausbiz TV, Scutt now brings that direct market experience to his role as APAC Market Analyst at StoneX Group, rather than relying on secondary commentary.

When he discusses foreign exchange movements or ASX dynamics, it is not because he has read about them. It is because he has traded them.

8- Meddy Demars – Investing & crypto content creator

The gap Meddy Demars fills is specific and underserviced: connecting global macroeconomic events to the practical reality of Australian investors. When the US Federal Reserve adjusts interest rates, when inflation data moves, when commodity prices shift — most Australian finance content either ignores the local implications or translates them poorly.

Demars, operating across TikTok and Instagram from Sydney, does the translation well: explaining what global conditions mean for Australian stocks, savings rates and investment portfolios in terms that are accessible without being condescending.

9- Simran Kaur – Founder, Friends That Invest

Friends That Invest is arguably the most successful community-building exercise in Australian personal finance, and Simran Kaur is the reason why. The New Zealand-based creator — whose audience is predominantly Australian — built a podcast, a book and a social media presence around a single insight: that the personal finance world was not speaking to young women, and that the consequences of that gap were significant.

The measurable cultural shift that followed — women engaging with investing concepts in communities that had not previously existed — is the kind of impact that most financial literacy programmes aim for and rarely achieve.

10- Effie Zahos – Money Editor at 9News

Effie Zahos is one of Australia’s most recognised financial commentators, appearing regularly across 9News, A Current Affair, Today and Today Extra as 9News Money Editor. Her role puts everyday money questions, from mortgage rates to cost-of-living pressures, in front of a national broadcast audience.

Before television, she spent years as editor of Money magazine, building the editorial foundation for her current commentary. She is also Director and Money Commentator at InvestSMART, an ambassador for Canstar, and a published author, with her financial advice available in print as well as on screen.

That combination, decades of editorial experience, an active broadcast presence, and a body of published work, is what makes her commentary carry weight beyond any single platform or post.

A 30-metre masterpiece unveiled in Monaco brings Lamborghini’s supercar drama to the high seas, powered by 7,600 horsepower and unmistakable Italian design.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”