Brazil Is Key to Slowing Global Warming. But Its Carbon Market Has Struggled.

A new attempt to create a regulated cap-and-trade system that is seen as critical to corporate competitiveness and economic resilience faces political headwinds

5 min

5 min

With Brazil struggling in its efforts to create a regulated carbon market, the country’s new president is moving to scrap his predecessor’s approach and start anew. But success is still far from guaranteed.

The administration of President Luiz Inácio Lula da Silva is putting the finishing touches on a proposal laying the groundwork for a new, regulated cap-and-trade system, which he is expected to send to Congress later this month. The approach is starkly different from that of his right-wing predecessor Jair Bolsonaro, who last year issued a decree relying on the private sector to establish the basis for a carbon market, which never happened.

In either case, the system would set emission caps for certain industries and allow some companies to temporarily offset their excess pollution by buying allowances from those that cut more emissions than required. One credit would amount to one metric ton of carbon dioxide either removed from or prevented from being emitted into the atmosphere. Over time, the cap would be lowered to reduce emissions.

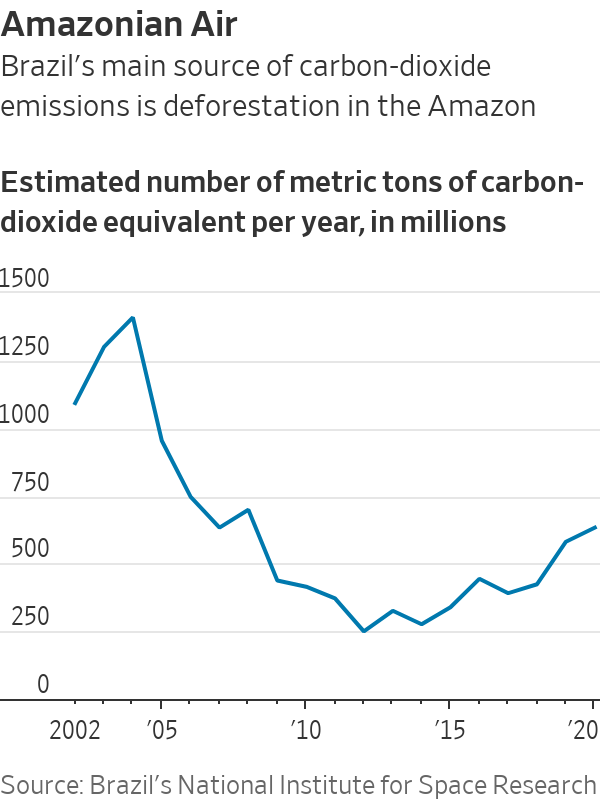

Financing carbon-capture projects such as reforestation could also generate carbon credits. Proponents say it is a way to protect the Amazon rainforest and other biomes, an approach that could also become an income stream to millions of impoverished residents currently making money off deforestation.

Yet despite broad support from exporters, who deem a regulated carbon market necessary to maintain key consumer markets overseas and attract investment, the initiative faces significant political hurdles at home and may not be enough to tackle the deforestation that is responsible for nearly half of the nation’s carbon footprint.

Brazil prides itself on getting nearly half of its energy and almost all of its electricity from renewable sources. It also already has an active market in voluntary carbon credits, where corporations buy credits from certified environmental projects to offset their emissions to meet self-imposed targets. But all that may still not be enough in a world increasingly worried about climate change.

“There is a global green arms race. Do we want to just sit on our achievements and watch while the tortoise outruns us?” said Gustavo Pinheiro, coordinator of the low-carbon economy portfolio at the nonprofit Institute for Climate and Society. “We need to price rising emissions,” he said, “and a regulated market is the least traumatic way to do it.”

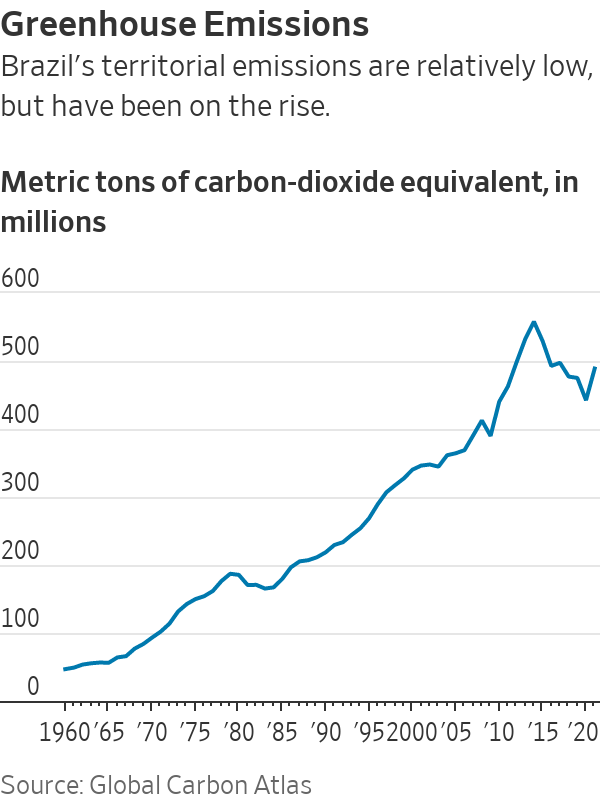

As home to nearly 60% of the Amazon rainforest, Brazil is crucial to slowing global warming. Brazil was responsible for about 1.3% of global carbon-dioxide emissions in 2021, according to European Union data, and its population, economy and footprint are expected to grow, pushing the country further away from its commitments in the 2015 Paris global climate agreement and underscoring the need for a regulated carbon market. A cap-and-trade system could also beef up the country’s troubled economy, as global trade increasingly requires cleaner supply chains, some experts say.

“Having a regulated carbon market would be good for the overall economy, [and] would put our corporations in a better position to compete,” said Luiz Gustavo Bezerra, a partner at law firm Tauil & Chequer, which is associated with Mayer Brown.

Local exporters say they could benefit from regulation compatible with rules already in place in key overseas markets, which increasingly demand low-carbon supply chains. For example, a local regulated carbon market could help exporters avoid the carbon border adjustment mechanism the EU plans to charge on some imported products from 2026.

Brazil is one of the largest exporters of iron used to make steel for a range of things, such as home appliances, vehicles and wind turbines. Iron-ore exporter Vale, which aims to have net-zero emissions by 2050 and uses an internal price of $50 per metric ton for its greenhouse-gas emissions, said in emailed answers that initiatives to price carbon are “important for the competitiveness of Brazilian industry.”

The nation is also a major global supplier of soybeans, corn and beef, products often associated with deforestation. Farming group Roncador, a producer of grains and beef, said it is worried about increasing global restrictions to products lacking environmental certificates.

“Since Brazil still doesn’t have a regulated [carbon] market, we are developing our own research and have developed our own protocol to ensure our activities have a positive impact on the environment,” the group’s Chief Executive Pelerson Penido Dalla Vecchia said.

Exporters also hope a regulated market would help repair Brazil’s abysmal environmental reputation, a product of its history of deforestation. “We have great expectations that the government will better regulate carbon markets,” said Antônio Queiroz, vice president of innovation, technology and sustainable development at Braskem, one of the world’s largest petrochemical companies.

A regulated market could also help lure green-economy investments, according to lawyer Bezerra: “We are always approached by private-equity firms looking for areas in Brazil to invest in reforestation or forest preservation.”

The country could earn up to $120 billion through 2030 on carbon credits, assuming an “optimistic scenario” of $100 a metric ton of carbon, according to a study by the Brazilian division of the International Chamber of Commerce and local carbon consulting firm WayCarbon. While that price is multiples of current voluntary market credits—lately valued at about $1—the EU credits have recently been trading around €82 a metric ton, equivalent to $88, according to OPIS.

Brazil has a goal of reforesting an area bigger than Pennsylvania, said Ana Toni, head of the National Secretariat for Climate Change: “How many countries have that?”

But carbon-capture projects based on forest preservation are typically traded in the so-called voluntary markets, often not covered by government regulation. Many have come under scrutiny recently after failing to fulfil their promises. For example, a Wall Street Journal investigation into a reforestation project in Peru found little of the money designated for rainforest preservation actually reached locals.

Despite these and other problems that bedevil this form of credit, Brazil’s Ministry of Development, Industry, Trade and Services said its proposal will allow credits from the voluntary market to be used, to a certain extent, in the new regulated one.

The da Silva administration plans to have a carbon market operating in a couple of years, Toni said. But da Silva lacks a majority in Congress, and in any case is expected to give priority to major fiscal and tax legislation ahead of the carbon-market bill.

And in a sign of the difficulties ahead, lawmakers recently passed legislation to weaken the Environmental Ministry led by sustainability advocate Marina Silva, who is backing the effort to create a regulated carbon market.

Annie Groth, head of advocacy and policy at Biofílica Ambipar Environment, a developer of carbon projects in the Amazon and other biomes, said there is hope that carbon legislation could be approved before the United Nations Climate Change Conference in Dubai beginning Nov. 30.

But she cautioned, “It’s the most optimistic scenario.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

Hand-built in Melbourne and limited to just 10 cars a year, the Zeigler/Bailey Z/B 4.4 is reshaping what a modern collector car can be.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.