China’s Small Businesses Are Hit Hard as Economic Recovery Falters

Beijing pushes banks to extend loans to small businesses, with limited success

5 min

5 min area, Beijing, China. (Photo by DeAgostini/Getty Images)")

China’s small businesses are cutting staff, struggling to pay off debt and nervous about the future. Their plight paints a grim picture of the country’s flagging recovery.

The country’s small and medium-size enterprises are crucial to the economy; they employed around 233 million people by the end of 2018, which was the last time this data was made public. But official data, recent disclosures from lenders and interviews with small-business owners show that many of these companies are suffering.

“The biggest problem for small and micro enterprises now is survival,” said Ji Shaofeng, the founder of a micro loan trade association based in China’s eastern Jiangsu province.

The struggles of China’s small businesses make clear how far the country has to go before it fully recovers from a series of lockdowns, which were part of Beijing’s strict response to the coronavirus.

When the government finally brought an end to its strict zero-Covid policy late last year, many economists expected a strong recovery. It hasn’t arrived. Consumer spending, factory orders and exports are among many indicators showing signs that the recovery is losing steam.

A recent survey of manufacturing purchasing managers in China showed a second consecutive month of contraction for small companies. China’s small-enterprise purchasing managers index is now at 47.9; a reading below 50 shows business activity is slowing.

Scott Yang, a wine and tea seller in Wenzhou, a city in China’s wealthy Zhejiang province, said many local business owners he knows are laying off employees and trying to cut costs, in response to a drop in factory orders.

Small enterprises started to add jobs at the end of the first quarter, when there was still some optimism about a recovery. But a PMI subindex showed employment at small enterprises was 48.7 in May, meaning these companies are either cutting staff or not replacing those who leave.

Huang Yiwen, who sells furniture online in Foshan, in southern China’s Guangdong province, said his business has been hurt by the weak property market, since new-home buyers are a reliable source of demand for furniture makers. Annual home sales fell to a six-year low in 2022, after a slump in the property sector that also led to debt defaults by some of China’s largest developers.

“It’s so hard to sell,” said Huang, regarding furniture.

Less than 40% of small and medium-size enterprises are operating at full capacity, which means producing all of the goods they can, according to the latest survey conducted by the China Association of Small and Medium Enterprises, which sends questionnaires to 3,000 SMEs in the country every month.

Economists warn that the problems facing small businesses can’t be isolated from the wider economy. Because small businesses are such a major source of employment, particularly in large cities, their struggles reflect—and could worsen—wider economic strains.

“If SMEs do not recover, it will be difficult for urban areas to create enough employment and income, which will have a significant impact on low- and middle-income families,” said Dan Wang, chief economist of Hang Seng Bank (China).

Chinese government officials are becoming uneasy about the economy and are planning a series of moves to stimulate growth, The Wall Street Journal recently reported. That could include billions of dollars of infrastructure spending and a loosening of rules in the property sector.

So far, Beijing’s attempts to prop up small businesses have focused mainly on making it easier for them to get funding. That has had limited success.

Since early 2020, Chinese regulators have pushed banks and other financial institutions to extend loans to small businesses that were hurt by the pandemic. In some parts of the country, local divisions of China’s central bank have sought to help small businesses by establishing teams to answer funding-related questions, as well as visiting factories and farms to assess their needs. The government has provided other targeted-relief measures such as tax exemptions and temporary rent reductions.

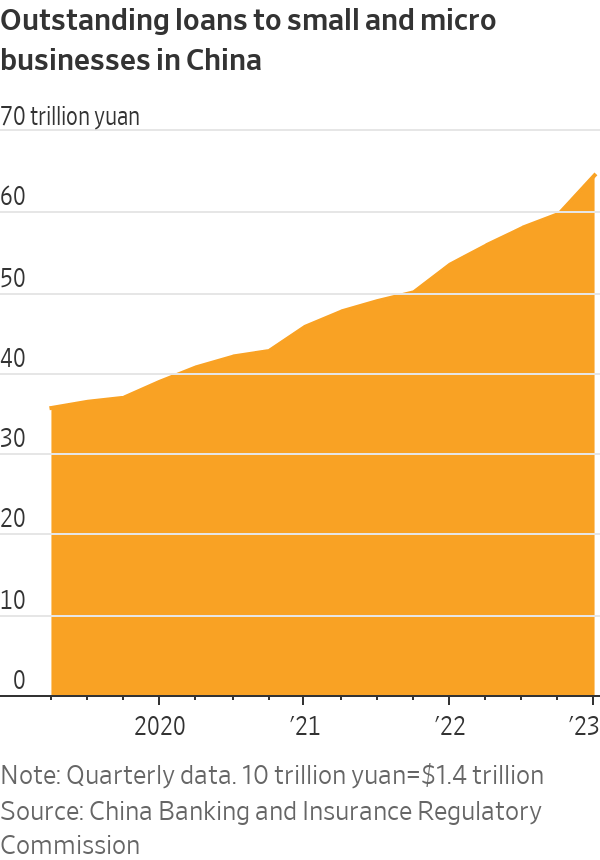

The total outstanding balance of loans to small and micro enterprises has been climbing, reaching the equivalent of $9 trillion at the end of March, according to data from China’s banking regulator.

Many small businesses in China don’t want to secure new financing unless it helps them clear previous debts. Yang, the wine seller, said that while financing is relatively cheap and easy to get, most local businesses he knows are borrowing only to stay afloat and not to expand.

Lufax, a Chinese internet-lending platform that caters mostly to small-business owners, said last month that about 5.7% of the total loans it facilitated were more than 30 days past due at the end of March. Its loan-delinquency rates, which are higher for unsecured loans, have risen for six consecutive quarters.

MYbank, an internet lender that serves small businesses, said in its latest annual report that the balance of its loans that were more than 30 days past due more than doubled last year. The company, an affiliate of the Chinese fintech giant Ant Group, said the impact of the pandemic and weak consumption last year caused many small- and micro-business owners to face continuous pressure.

Many commercial banks have given borrowers more time to repay their loans, extending their forbearance for small businesses to this year. Small businesses whose loans were due in the fourth quarter of 2022 will have until the end of this month to repay, according to a notice from the central bank and a group of regulators.

Chinese banks have allowed some small businesses to roll over their loans, but if these small businesses are unable to repay in the future, they will eventually have to be recognized as bad loans, said Jay Guo, a former banker and current dean at the Ningbo China Institute for Supply Chain Innovation.

“It only makes sense to extend loans if the economy rebounds and SMEs are able to sell their goods,” said Guo.

Ji, of the micro loan trade association, said that while some sectors such as tourism and catering have rebounded in the past few months, small businesses in manufacturing, trade and other industries are still under pressure as demand remains well below where it used to be.

Small businesses are falling victim to a vicious cycle that is affecting the wider economy, said Xiangrong Yu, chief China economist at Citigroup. The poor performance of some private companies is leading to a loss of confidence, and that low confidence is making it hard for those companies to do better, he said.

“Lack of confidence is both a symptom of the problem and the root cause of the problem,” said Yu.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

Limited to 630 units, Lamborghini’s latest Urus Capsule pushes personalisation further than ever, blending hybrid performance with over 70 bespoke design combinations.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

3 minFor decades, Australia has leaned into its reputation as the lucky country. But luck, as it turns out, is not an economic strategy.

What once looked like resilience now appears increasingly fragile. Beneath the surface of rising property values and steady headline growth, the Australian economy is showing signs of strain that can no longer be ignored.

Recent data paints a sobering picture. Australia has recorded one of the largest declines in real household disposable income per capita among advanced economies.

Wages have failed to keep pace with inflation, meaning many Australians are working harder for less. On a per capita basis, income growth has stalled and, at times, reversed.

And yet, on paper, things still look relatively solid. GDP is growing. Unemployment remains low. But that growth is increasingly being driven by population expansion rather than productivity.

More people are contributing to output, but not necessarily improving living standards.

That distinction matters.

For years, Australia’s economic success rested on a powerful combination: a once-in-a-generation mining boom, a credit-fuelled housing market, strong migration and a property sector that rarely faltered. Between 1991 and 2020, the country avoided recession entirely, building enormous wealth in the process.

But much of that wealth is tied to property. Around two-thirds of household wealth sits in real estate, inflated by leverage and sustained by demand. It has worked, until now.

The problem is the supply side of the economy has not kept up.

Housing supply is falling behind population growth. Rental vacancies are near record lows.

Construction firms are collapsing at an elevated rate. At the same time, massive infrastructure pipelines are competing with residential projects for labour and materials, pushing costs higher and delaying delivery.

The result is a system under pressure from all angles.

Despite near full employment, productivity growth has stagnated for years. In simple terms, Australians are putting in more hours without generating more output per hour. The economy is running faster, butgoing nowhere.

Meanwhile, government spending continues to expand. Public debt is approaching $1 trillion, with spending now accounting for a record share of GDP.

The gap between spending and revenue has been filled by borrowing for decades, adding further pressure to an already stretched system.

This is where the uncomfortable question emerges.

Has Australia become too reliant on a model driven by rising property values, expanding credit and population growth?

As asset prices rise, households feel wealthier and borrow more. Banks lend more. Governments collect more revenue. Migration fuels demand. The cycle reinforces itself.

But when productivity stalls and debt outpaces real income, the system begins to depend on constant expansion just to stay stable.

It is not a collapse scenario. But it is not particularly stable either.

Nowhere is this more evident than in housing.

The National Housing Accord targets 1.2 million new homes over five years, yet current completion rates are well below that pace. With approvals falling and construction costs rising, the gap between supply and demand is widening, not narrowing.

Housing is also one of the largest contributors to inflation, with costs rising sharply across rents, construction and utilities. Yet the private sector, from small investors to major developers, is struggling to make projects stack up in the current environment.

This brings the policy debate into sharper focus.

Tax settings such as negative gearing and capital gains concessions have undoubtedly boosted demand over the past two decades. But they have also supported supply. Removing them may ease prices briefly, but risks deepening the supply shortage over time.

That is the paradox.

Policies designed to make housing more affordable can, in practice, make the shortage worse if they discourage development. The optics may appeal, but the economics are far less forgiving.

It is also worth remembering that most property investors are not institutional players. The majority own just one investment property. They are, in many cases, ordinary Australians using real estate as their primary wealth-building tool.

Undermining that system without replacing it with a viable alternative risks unintended consequences, from reduced supply to higher rents and increased inflation.

So where does that leave Australia?

At a crossroads.

The country can continue to rely on population growth and rising asset prices to drive economic activity. Or it can shift towards a model built on productivity, innovation and sustainable growth.

The latter is harder. It requires structural reform, long-term thinking and political discipline.

But it is also the only path that leads to genuine, lasting prosperity.

The question is no longer whether Australia has been lucky.

It is whether it can evolve before that luck runs out.

Paul Miron is the Co-Founder & Fund Manager of Msquared Capital.

As the season turns, Handpicked Wines’ latest Pinot Noir and Chardonnay releases reveal how subtle shifts in place shape what ends up in the glass.

Margot Robbie and Jacob Elordi star in an adaptation of the classic novel that respects the romance’s slow burn.