Get Ready for the Richcession

Well-off Americans could get hurt more than usual in the next downturn

3 min

3 min

Economic downturns are usually horrible for poor people, bad for the middle class and an inconvenience for the rich. But if the economy enters a recession in 2023, or even if it manages to narrowly evade one, it might be the well-heeled who take a bigger hit than usual.

Call it the richcession.

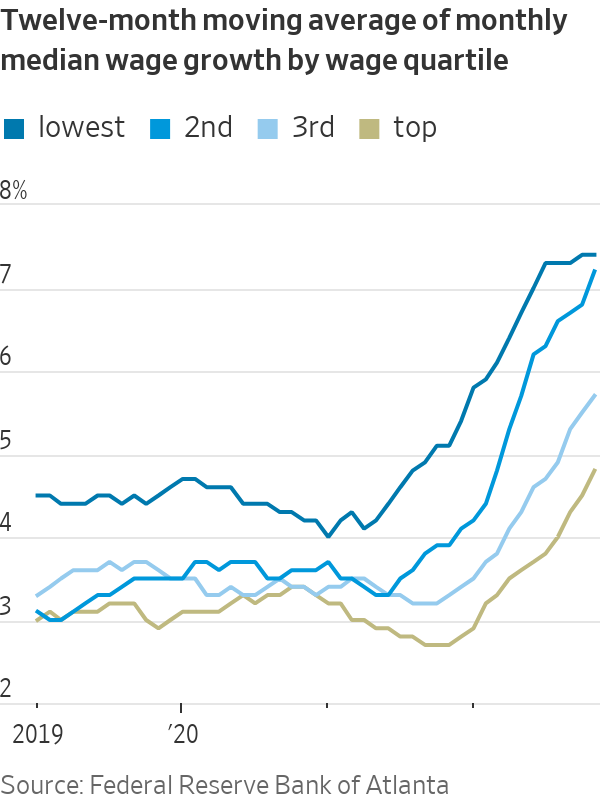

Other than a small number of ascetics, nobody likes being poor. Doing without, living with so little savings that setbacks such as illness or job loss can be debilitating, is an ever-present source of stress. But for many poorer people, the years since the Covid crisis struck have been a bit easier financially than the years that preceded it. Several rounds of government relief helped them weather the early stages of the pandemic, and now a tight job market is providing them with wage gains that are reducing inflation’s bite. Federal Reserve figures show that the net worth of households in the bottom fifth by income was 42% higher in the third quarter than at the end of 2019, and up 17% from the end of 2021.A wage tracker developed by the Federal Reserve Bank of Atlanta shows that the 12-month moving average of annualised monthly wage growth for workers in the bottom quartile by income was 7.4% as of November.

With the important caveat that they were starting off from much higher bases, percentage gains for the rich have been more muted. Household net worth for the top fifth was 22% higher in the third quarter than before the pandemic, and was down 7.1% from the end of 2021—a consequence of the falling stock market. Paychecks haven’t risen as much, either, with the Atlanta Fed measure showing average annualized monthly wage growth for workers in the top quartile was 4.8%.

Recent layoffs have also inordinately affected higher-income workers. Many of the tech companies that have made headlines with layoff announcements pay extremely well. Securities filings show that the median worker at Facebook parent Meta Platforms made $295,785 in 2021, for example, while the median worker at Twitter made $232,626. And layoffs at those places where the typical worker is less well paid, such as Amazon.com, have largely been aimed at white-collar workers.

The consolation for higher-income workers who are laid off is that it should be relatively easier for them to find new work than it is for poorer people who lose their jobs. That is because the job skills of the more highly educated are generally more transferable than the skills of other workers. But they will still be in for a period of belt tightening, and they might not get paid quite so well at their new jobs as they were at their old ones.

Meanwhile, even though big-company layoffs have been making headlines, so far they haven’t made much of a dent in overall employment statistics. This is in part because industries that aren’t as well-represented in the stock market, and that typically employ more lower- and middle-income workers, are still straining to hire workers. In November the leisure and hospitality sector was 980,000 jobs short of its February 2020 employment level. Employment in healthcare and social assistance only recovered to its prepandemic levels in September. This is a job category that, in part because of the needs of an ageing population, grew even when overall U.S. unemployment shot higher after the 2008 financial crisis. To return to its growth trend over the decade preceding the pandemic, it would need to add about 1.1 million jobs.

That need for workers—especially as more Americans engage in services such as dining out—is part of why even among those economists expecting a recession in the coming year, many don’t think the job market will take a severe hit. This makes poorer Americans better positioned than usual to handle a weak economy. Not only are their finances in relatively good condition, they might be less likely to experience severe job losses.

Heading into the new year, businesses that cater to the well-off might be in for disappointment, while those that favour the hoi polloi over the hoity-toity might do better. And if there is a recession, the economy could be on much more equal footing as it begins to recover than is usually the case.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

From warmer neutrals to tactile finishes, Australian homes are moving away from stark minimalism and towards spaces that feel more human.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.