It Just Had an Energy Crisis, Now Europe Faces a Food Shock

Food prices continue to rise at a rapid pace, surprising central banks and pressuring debt-laden governments

4 min

4 min

LONDON—Fresh out of an energy crisis, Europeans are facing a food-price explosion that is changing diets and forcing consumers across the region to tighten their belts—literally.

This is happening even though inflation as a whole is falling thanks to lower energy prices, presenting a new policy challenge for governments that deployed billions in aid last year to keep businesses and households afloat through the worst energy crisis in decades.

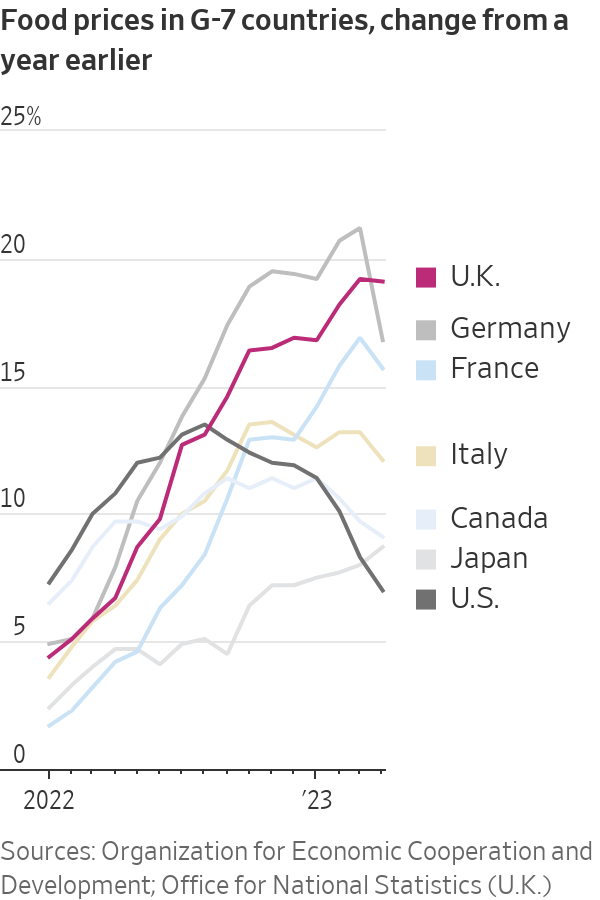

New data on Wednesday showed inflation in the U.K. fell sharply in April as energy prices cooled, following a similar pattern around Europe and in the U.S. But food prices were 19.3% higher than a year earlier.

The continued surge in food prices has caught central bankers off guard and pressured governments that are still reeling from the cost of last year’s emergency support to come to the rescue. And it is pressuring household budgets that are also under strain from rising borrowing costs.

In France, households have cut their food purchases by more than 10% since the invasion of Ukraine, while their purchases of energy have fallen by 4.8%.

In Germany, sales of food fell 1.1% in March from the previous month, and were down 10.3% from a year earlier, the largest drop since records began in 1994. According to the Federal Information Centre for Agriculture, meat consumption was lower in 2022 than at any time since records began in 1989, although it said that might partly reflect a continuing shift toward more plant-based diets.

Food retailers’ profit margins have contracted because they can’t pass on the entire price increases from their suppliers to their customers. Markus Mosa, chief executive of the Edeka supermarket chain, told German media that the company had stopped ordering products from several large suppliers because of rocketing prices.

A survey by the U.K.’s statistics agency earlier this month found that almost three-fifths of the poorest 20% of households were cutting back on food purchases.

“This is an access problem,” said Ludovic Subran, chief economist at insurer Allianz, who previously worked at the United Nations World Food Program. “Total food production has not plummeted. This is an entitlement crisis.”

Food accounts for a much larger share of consumer spending than energy, so a smaller rise in prices has a greater impact on budgets. The U.K.’s Resolution Foundation estimates that by the summer, the cumulative rise in food bills since 2020 will have amounted to 28 billion pounds, equivalent to $34.76 billion, outstripping the rise in energy bills, estimated at £25 billion.

“The cost of living crisis isn’t ending, it is just entering a new phase,” Torsten Bell, the research group’s chief executive, wrote in a recent report.

Food isn’t the only driver of inflation. In the U.K., the core rate of inflation—which excludes food and energy—rose to 6.8% in April from 6.2% in March, its highest level since 1992. Core inflation was close to its record high in the eurozone during the same month.

Still, Bank of England Gov. Andrew Bailey told lawmakers Tuesday that food prices now constitute a “fourth shock” to inflation after the bottlenecks that jammed supply chains during the Covid-19 pandemic, the rise in energy prices that accompanied Russia’s invasion of Ukraine, and surprisingly tight labor markets.

Europe’s governments spent heavily on supporting households as energy prices soared. Now they have less room to borrow given the surge in debt since the pandemic struck in 2020.

Some governments—including those of Italy, Spain and Portugal—have cut sales taxes on food products to ease the burden on consumers. Others are leaning on food retailers to keep their prices in check. In March, the French government negotiated an agreement with leading retailers to refrain from price rises if it is possible to do so.

Retailers have also come under scrutiny in Ireland and a number of other European countries. In the U.K., lawmakers have launched an investigation into the entire food supply chain “from farm to fork.”

“Yesterday I had the food producers into Downing Street, and we’ve also been talking to the supermarkets, to the farmers, looking at every element of the supply chain and what we can do to pass on some of the reduction in costs that are coming through to consumers as fast as possible,” U.K. Treasury Chief Jeremy Hunt said during The Wall Street Journal’s CEO Council Summit in London.

The government’s Competition and Markets Authority last week said it would take a closer look at retailers.

“Given ongoing concerns about high prices, we are stepping up our work in the grocery sector to help ensure competition is working well,” said Sarah Cardell, who heads the CMA.

Some economists expect that added scrutiny to yield concrete results, assuming retailers won’t want to tarnish their image and will lean on their suppliers to keep prices down.

“With supermarkets now more heavily under the political spotlight, we think it more likely that price momentum in the food basket slows,” said Sanjay Raja, an economist at Deutsche Bank.

It isn’t entirely clear why food prices have risen so fast for so long. In world commodity markets, which set the prices received by farmers, food prices have been falling since April 2022. But raw commodity costs are just one part of the final price. Consumers are also paying for processing, packaging, transport and distribution, and the size of the gap between the farm and the dining table is unusually wide.

The BOE’s Bailey thinks one reason for the bank having misjudged food prices is that food producers entered into longer-term but relatively expensive contracts with fertilizer, energy and other suppliers around the time of Russia’s invasion of Ukraine in their eagerness to guarantee availability at a time of uncertainty.

But as the pressures being placed on retailers suggest, some policy makers suspect that an increase in profit margins may also have played a role. Speaking to lawmakers, Bailey was wary of placing any blame on food suppliers.

“It’s a story about rebuilding margins that were squeezed in the early part of last year,” he said.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

A long-standing cultural cruise and a new expedition-style offering will soon operate side by side in French Polynesia.

Warmer minimalism, tactile materials and wellness focused layouts are redefining luxury interiors as homeowners design for comfort, connection and lasting appeal.