Well Into Adulthood and Still Getting Money From Their Parents

Nearly 60% of parents provide financial help to their adult kids, a new study finds

4 min

4 min

Parents have always supported their children into adulthood, from funding weddings to buying a home. Now the financial umbilical cord extends much later into adulthood.

About 59% of parents said they helped their young adult children financially in the past year, according to a report released Thursday by the Pew Research Center that focused on adults under age 35. (This question hadn’t been asked in prior surveys.) More young adults are also living with their parents. Among adults under age 25, 57% live with their parents, up from 53% in 1993.

Parental support is continuing later in life because younger people now take longer to reach many adult milestones—and getting there is more expensive than it has been for past generations, economists and researchers said. There is also a larger wealth gap between older Americans and younger ones, giving some parents more means and reason to help. In short, adulthood no longer means moving off the parental payroll.

“That transition has gotten later and later, for a lot of different reasons. Now it’s age 25, 30, 35, 40,” said Sarah Behr, founder of Simplify Financial Planning in San Francisco.

Kami Loukipoudis, a 39-year-old director of design, and husband Adam Stojanik, a 39-year-old high-school teacher, knew they would need parental assistance to buy in New York’s expensive home market.

“We could pay a mortgage, but that down payment was the absolute crusher,” Stojanik said. “The idea of trying to save up on our own—as long as we were paying rents in NY, would’ve taken 300 years.”

Loukipoudis’s mother gave them the money for a 10% down payment on a two-bedroom apartment in the New York borough of Queens.

The young-adult allowance

Adult children aren’t necessarily getting larger checks from their parents, but they are staying on the parental payroll for longer than previous generations, according to Marla Ripoll, professor of economics at the University of Pittsburgh who studied the trend by analysing payments from parents to adult children over a 20-year span.

Ripoll found that 14% of adult children receive a transfer of money from their parents at least once in any given year, and roughly half get financial help at some point within that period. Those rates have been stable for years. What has changed is that the transfers now continue for much longer, she found. This longer-term help might be a drag on social mobility, as it becomes even harder for young people from lower-income families to catch up, researchers said.

Of the young adult children who said they received financial help from a parent in the past year, most said they put it toward day-to-day household expenses, such as phone bills and subscriptions to streaming services like Netflix, according to the Pew survey.

The amount of money and the frequency of help varies by age; those on the older end of the 18-to-34 cohort are far likelier to say they are completely financially independent from their parents compared with younger adult children, as many in the latter group are completing their education. Nearly a third of young adult children between the ages of 30 and 34 say they still get parental help.

Heather McAfee, a 33-year-old physical therapist in Austin, Texas, said she lived at home between 2019 and 2021; otherwise she wouldn’t have been able to make progress paying down her student loans while rent prices in her area remained so high. The plan worked—she has since reduced her student-debt balance from $83,000 to $15,000.

“It helped tremendously,” she said. “I didn’t have to take out more loans to pay for apartment living or anything like that. That stress was gone.”

Setting limits on financial help

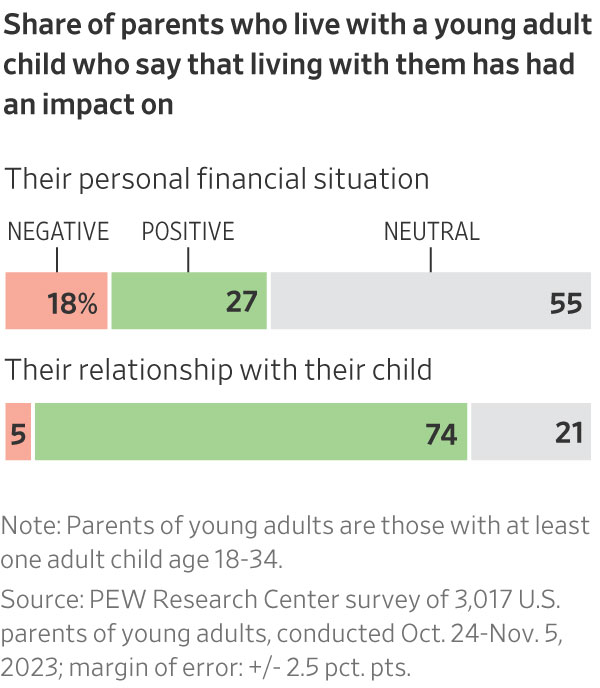

A little more than half of parents surveyed said that having their adult children home brought them closer together or improved their relationship, but nearly 20% said it dented their personal finances.

Financial advisers often find themselves in the tricky position of speaking to both ends of the equation: adult children who need assistance and the parents determined to help children well into middle age, within limits.

Whereas previous generations would step into a greater sense of financial independence in their early 20s, young adult children today are often unable to reach similar markers of such independence—living on their own or buying their first home, for example—without greater financial resources.

Families typically don’t set concrete rules around when financial help will happen and what the money is used for, which can result in surprises down the road, Behr said.

In one case, Behr’s clients received the down payment they needed to purchase a condo from a generous mother-in-law. Years later, that same mother-in-law told them she expected a payout once the couple sold the home.

The hand-me-down payment

Down-payment help from parents—a given for many first-time home buyers—is growing thanks to higher home prices and elevated mortgage rates.

About a fifth of first-time home buyers said they got help from a relative or friend when pulling together the money needed for a down payment, according to a 2023 survey of home buyers and sellers from the National Association of Realtors. And 38% of home buyers under age 30 received help with the down payment from their parents, according to a survey this spring by Redfin.

Wealthy families often go further than helping with the down payment. They become a true bank of mom and dad and write a mortgage. The Internal Revenue Service sets minimum levels of interest for such loans, which remain significantly cheaper than current mortgage rates.

Timothy Burke, chief executive at National Family Mortgage, which facilitates such loans, said parents are often frustrated on behalf of their house-hunting children. High interest rates and the cutthroat housing market are holding their children back from reaching a milestone the parents themselves were more easily able to access.

Mei Chao, a 41-year-old stay-at-home mom, and her husband, William Chao, a 44-year-old information-technology specialist, bought their first house as a couple in 2017. They relied on financial help from her husband’s two sisters and his mother to help them bridge a gap in their house-buying timeline. While they waited to sell William’s Manhattan condo, they used the money from the family to purchase the new house in Queens.

The structure of the agreements got tricky. After selling the condo in Manhattan, Mei and her husband were able to repay his sisters in full. But they didn’t have enough money left over from the sale to do the same for Mei’s mother-in-law. So they kept the mother-in-law’s name on the deed to the house—a concession Mei said they were both more than happy to make.

“Ultimately, it all worked out. I’m glad his mother pushed us,” Mei said. “Without her help, I could not say we would have this home.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

The voices reshaping how Australians think about money — and why credibility matters more than reach.

6 min

The best financial advice many Australians are receiving right now is not coming from licensed advisers charging by the hour. It is coming through a phone screen, in the ten minutes between work and dinner, from creators who have built credibility the hard way: by being right, being transparent, and being specific in a space where vagueness has always been the easy default.

This is not a ranking by follower count. Follower count is a measure of distribution, not of quality. What follows is a ranking by substance — credentials, accuracy, community depth, and the quality of what an audience actually learns from following these accounts. The distinction matters, because the Australians acting on this content are making real financial decisions with real money.

1- Queenie Tan – Corporate Authorised Representative; Co-Founder & Director, Invest With Queenie & Billroo

There are finance influencers who talk about building wealth, and there are those who document it in real time with receipts. Queenie Tan belongs firmly in the second category. Starting from a $400-per-week income, Tan built her net worth past $1 million while publishing the actual numbers — income, savings rate, investment decisions — for an audience of more than 400,000 across platforms.

She is a Corporate Authorised Representative, co-founder of the personal finance app Billroo, and the author of a book that has become a practical reference for young Australians navigating ETFs, superannuation and property. What separates her from the crowded field of money educators is precision: she does not talk in principles when she can talk in percentages.

2- Alan Kohler – Editor-in-Chief, Eureka Report; Editor-in-Chief, InvestSMART Group; ABC News finance presenter, host of Inside Business.

If Queenie Tan represents the new wave of personal finance creators, Alan Kohler represents something the new wave will spend decades trying to build: institutional credibility that has survived multiple economic cycles. As Editor-in-Chief of the Eureka Report and InvestSMART Group, and a decades-long presence on ABC News, Kohler has spent more than thirty years making financial analysis accessible without dumbing it down.

His coverage of RBA decisions, market movements and economic policy is cited by podcasters, journalists and fund managers alike. He is not chasing virality. He does not need to.

3- Aleks Nikolic – Corporate lawyer; host, Big Swinging Stocks podcast

Most finance creators address the mechanics of money. Aleks Nikolic addresses the psychology — and that distinction explains why her following is as loyal as it is. Operating as Broke Girl Wealth across Instagram, TikTok and YouTube, Nikolic covers ETFs, crypto and investment strategy, but her real differentiator is a willingness to discuss the emotional architecture of financial decision-making.

Shame around debt. Fear around market volatility. The limiting beliefs that stop people acting on what they already know. In a space where confidence is routinely performed, her candour is a genuine competitive advantage.

4- Bryce Leske & Alec Renehan – Equity Mates Media

Equity Mates did not build a following. They built a media company. What began as a podcast by two friends learning to invest has grown into Australia’s most established investing media brand, covering ASX stocks, ETFs, global markets and fund manager interviews across podcast, social and YouTube.

The longevity is the credential. Equity Mates has operated through multiple market cycles, a global pandemic, and a generational shift in how Australians engage with investing — and its audience has grown through all of it. When the hosts speak, their listeners know they have been paying attention for years.

5- The Lazy CEO – CEO & Founder, Showpo; Shark Tank Australia investor

The metric that matters most on social media is not followers — it is engagement, because engagement signals trust. Jane Lu, known as The Lazy CEO, maintains an engagement rate of approximately 1.15 per cent on Instagram, which is exceptional for a finance account of his size. Her 242,000-plus followers are not passive consumers: they ask questions, share experiences and apply what they read.

Her content focuses on business finance and wealth building, and the active comment sections are the clearest possible evidence that her audience does not merely scroll past.

6- Tash Invests – Founder, Tash Lends; Forbes Australia 30 Under 30

Tash Invests built her following on a premise that sounds simple but is rarer in practice than it should be: she publishes the actual numbers. Not approximations or ranges or anonymised case studies — her salary, her savings rate, her portfolio value, her net worth, updated and on the record.

Having bought her first property at twenty-two and grown her documented net worth past $1 million, she has become the primary reference point for young Australians trying to understand what building wealth on a moderate income genuinely looks like. The specificity is the product.

7- David Scutt – APAC Market Analyst at StoneX Group

The authority of most finance social media content rests on research and reading. David Scutt‘s authority rests on having done the job. A former Treasury Dealer at Arab Bank and the Commonwealth Bank, former ASX Business Supervisor, and former Global Markets Editor at Business Insider Australia and anchor at ausbiz TV, Scutt now brings that direct market experience to his role as APAC Market Analyst at StoneX Group, rather than relying on secondary commentary.

When he discusses foreign exchange movements or ASX dynamics, it is not because he has read about them. It is because he has traded them.

8- Meddy Demars – Investing & crypto content creator

The gap Meddy Demars fills is specific and underserviced: connecting global macroeconomic events to the practical reality of Australian investors. When the US Federal Reserve adjusts interest rates, when inflation data moves, when commodity prices shift — most Australian finance content either ignores the local implications or translates them poorly.

Demars, operating across TikTok and Instagram from Sydney, does the translation well: explaining what global conditions mean for Australian stocks, savings rates and investment portfolios in terms that are accessible without being condescending.

9- Simran Kaur – Founder, Friends That Invest

Friends That Invest is arguably the most successful community-building exercise in Australian personal finance, and Simran Kaur is the reason why. The New Zealand-based creator — whose audience is predominantly Australian — built a podcast, a book and a social media presence around a single insight: that the personal finance world was not speaking to young women, and that the consequences of that gap were significant.

The measurable cultural shift that followed — women engaging with investing concepts in communities that had not previously existed — is the kind of impact that most financial literacy programmes aim for and rarely achieve.

10- Effie Zahos – Money Editor at 9News

Effie Zahos is one of Australia’s most recognised financial commentators, appearing regularly across 9News, A Current Affair, Today and Today Extra as 9News Money Editor. Her role puts everyday money questions, from mortgage rates to cost-of-living pressures, in front of a national broadcast audience.

Before television, she spent years as editor of Money magazine, building the editorial foundation for her current commentary. She is also Director and Money Commentator at InvestSMART, an ambassador for Canstar, and a published author, with her financial advice available in print as well as on screen.

That combination, decades of editorial experience, an active broadcast presence, and a body of published work, is what makes her commentary carry weight beyond any single platform or post.

By improving sluggish performance or replacing a broken screen, you can make your old iPhone feel new agai

Limited to 630 units, Lamborghini’s latest Urus Capsule pushes personalisation further than ever, blending hybrid performance with over 70 bespoke design combinations.