Why China’s Middle Class Is Losing Its Confidence

The country’s economic miracle created an optimistic middle class. A slowdown has left it shaken.

5 min

5 min

Three years ago, everything seemed to be going right for Blake Xu.

The 33-year-old entrepreneur and his family had built a portfolio of properties during China’s real-estate boom. His wife was expecting their first child. He had just sold an apartment, and put almost half of the proceeds into the stock market.

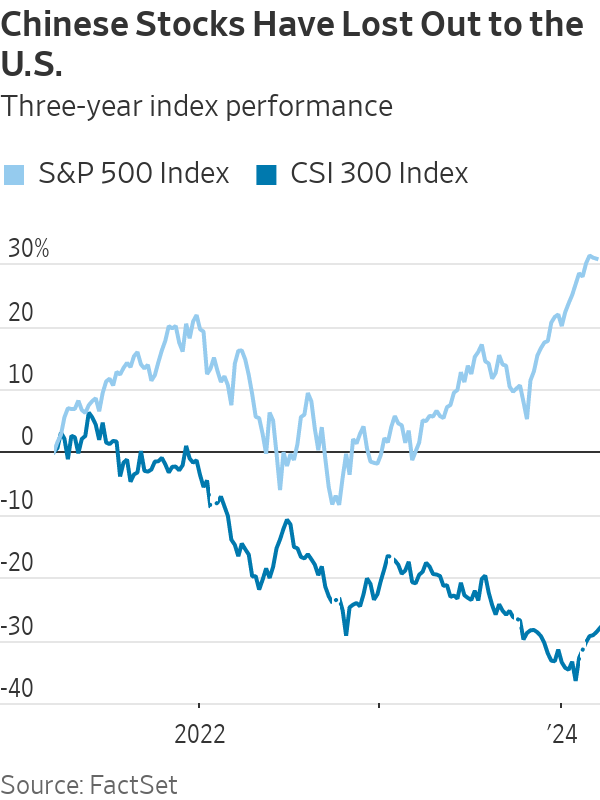

Since then, the property market has entered a years long downturn, the country’s benchmark CSI 300 stock index has lost around a third of its value and the economy has become increasingly vulnerable, suffering from moribund consumer confidence, weak private-sector investment and sky-high youth unemployment.

Xu has already pulled almost all of his money out of China’s stock market. His next exit may be from China itself. undefined undefined “I don’t know where the future path lies,” said Xu, who lives in Shanghai. “Once our child grows a little older, we intend to send him abroad, and perhaps we will also go.” undefined undefined For most of their lives, China’s new generation of middle-class citizens could take a booming economy for granted. But the property rout, the stock-market slump and the wider economic downturn have forced them to confront a difficult question: Are China’s boom years over for good?

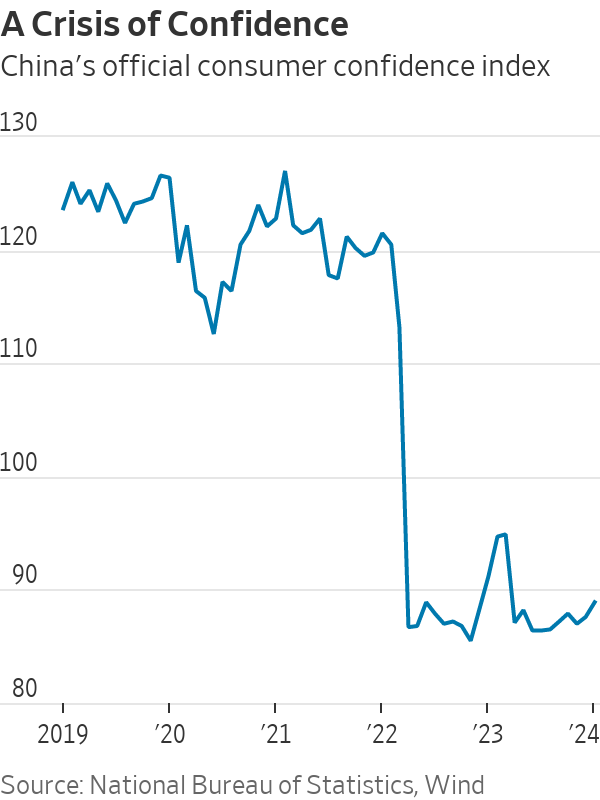

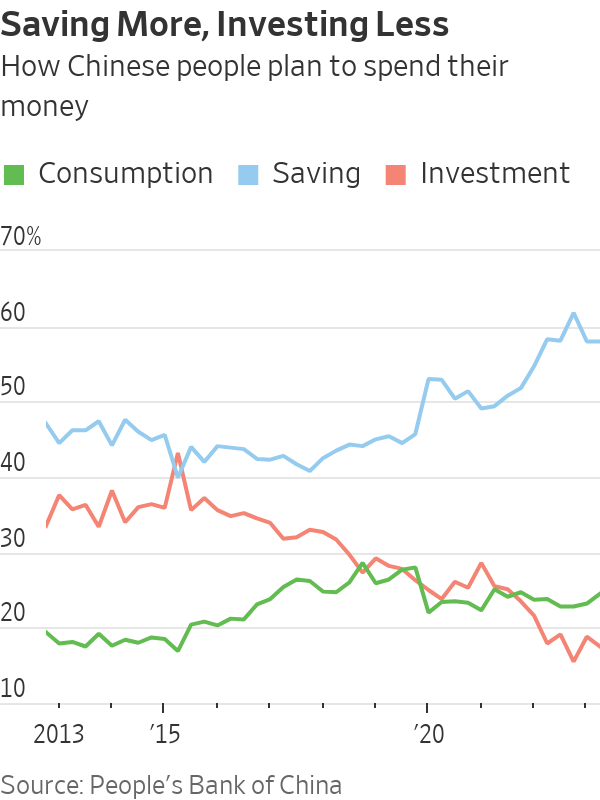

Chinese citizens are spending less, saving more and shying away from risky investments. Household savings in the country reached $19.83 trillion by February, the highest figure on record, according to data from the central bank. Consumer confidence is near its lowest level in decades.

The increasing sense of nervousness among China’s city-dwellers and white-collar workers could be a major problem for Beijing. China’s government has for years derived legitimacy from its reputation for sound economic management. undefined undefined Now, that reputation looks increasingly shaky.

Finding an exit strategy

Hugo Chen, 30, was born during the early stages of China’s remarkable economic transformation, which came after former leader Deng Xiaoping rolled back the worst excesses of Maoism and opened the doors to global trade.

Chen, who was raised in the wealthy coastal city of Shenzhen, studied for a master’s degree in the U.K. He moved back to China in 2017 to work in finance and, like many Chinese citizens, decided to play the stock market. He also bought bonds and invested in insurance products.

But last year, he made a decision: no more Chinese shares.

Chen, a banker, had previously helped an insurance company manage its money. He knew more than most about investing—and China no longer seemed like a smart place to invest money.

By the end of 2023, the CSI 300 index had fallen for three years in a row. Even worse, stocks in the U.S., Japan and elsewhere had surged. It was supposed to be China’s century , but the economy and the stock market were losing ground to those in other countries.

“Becoming poor is one thing. Becoming poor while others get rich is another,” said Chen.

He shifted most of his investments into funds that buy U.S. stocks.

China has more than 220 million individual investors, meaning stock-market moves can have a big impact on the national psyche. These small investors once had a reputation as gamblers. After the slump of the past few years, they have scaled back their bets and increasingly shifted to safer assets such as money-market funds.

The real-estate sector has done even more damage to confidence. What started as an attempt by Beijing to rein in excessive debt in the sector around three years ago has morphed into a multiyear crisis, pushing dozens of developers to the brink of collapse and pulling the rug out from under one of China’s main drivers of economic growth.

The price of existing homes in China’s most developed cities fell 6.3% in February compared with the same month last year— the biggest year-over-year decline on record.

Xu, the entrepreneur, sold a second property in a process he described as extremely painful. But he has no regrets: The money will give him the flexibility he needs to leave the country if things get worse, he said.

“Emotionally, I hope for the best for this country,” said Xu. “However, if this team of leaders stays, to be frank, I have to have an exit strategy, as the outlook is worrisome.”

That is precisely the kind of sentiment that will unsettle officials in Beijing. Although China’s government keeps a tight grip on power, it is acutely sensitive to the public mood.

China’s population has a history of public displays of dissent, including public protests against banks and companies . Beijing has tolerated at least a degree of dissent, as long as its citizens follow one overriding principle: Don’t blame the central government.

But some people in the country do blame Beijing for the current economic troubles, pointing to policy U-turns on internet companies, private education and real estate, and a strict approach to containing Covid-19 that has dealt lasting damage to confidence in the country.

The shift toward low investment and high savings is fuelling a vicious cycle, where the economic slump erodes confidence levels and, in turn, low confidence worsens the downturn, said Yasheng Huang, professor of global economics and management with MIT Sloan School of Management and a fellow at the Wilson Center.

“When a society settles on a particular psychology, it’s not easy to shift,” he said.

From hope to fear

Scarlett Hu, 37, remembers how it felt to be back in China in 2014. She had just returned from studying abroad, and took a job in Shanghai’s luxury-goods sector.

“At that time everyone in the society was full of hope. There was this promising sentiment around,” said Hu. “When we went out to relax after work, we believed that tomorrow would be better and let’s have fun today.”

Hu bought an apartment in Shanghai in 2017 and started buying mutual funds that invest in the stock market in 2020, before the birth of her son. She hoped the money would help pay for his education. At the time, it seemed like a smart bet: The real-estate market was booming, and stocks were nearing a record high, cheered on by China’s bullish state media.

Her apartment has now lost 15% of its value, and her mutual-fund portfolio is down 35%.

“Now we talk about concrete plans and measures to secure a more certain future, focusing on ways to enhance our sense of security. You don’t feel that kind of ambition any more,” she said.

China’s government has taken steps to tackle the downturn, including easing lending rules for battered real-estate firms, cutting borrowing rates and pledging to resolve the debt problems of local governments. But Beijing appears reluctant to adopt the sort of direct stimulus Western governments embraced in the wake of Covid-19, when direct payments to consumers helped get spending back on track.

In early March, Chinese Premier Li Qiang said the government was targeting growth of around 5% for 2024, and there have been recent signs of improvement.

But economists think Beijing will find it difficult to hit this growth target, and some people in the country worry that things are about to get worse.

A 40-year-old equity analyst based in Beijing said she lost her job last August when the consulting firm she worked for closed. She has two children to care for, her husband’s income is unstable, and she is bracing herself for more pain to come.

“Everyone is saying that this year might still be the best in the next decade, so we should be prepared for a long period of hardship,” she said.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

The voices reshaping how Australians think about money — and why credibility matters more than reach.

6 min

The best financial advice many Australians are receiving right now is not coming from licensed advisers charging by the hour. It is coming through a phone screen, in the ten minutes between work and dinner, from creators who have built credibility the hard way: by being right, being transparent, and being specific in a space where vagueness has always been the easy default.

This is not a ranking by follower count. Follower count is a measure of distribution, not of quality. What follows is a ranking by substance — credentials, accuracy, community depth, and the quality of what an audience actually learns from following these accounts. The distinction matters, because the Australians acting on this content are making real financial decisions with real money.

1- Queenie Tan – Corporate Authorised Representative; Co-Founder & Director, Invest With Queenie & Billroo

There are finance influencers who talk about building wealth, and there are those who document it in real time with receipts. Queenie Tan belongs firmly in the second category. Starting from a $400-per-week income, Tan built her net worth past $1 million while publishing the actual numbers — income, savings rate, investment decisions — for an audience of more than 400,000 across platforms.

She is a Corporate Authorised Representative, co-founder of the personal finance app Billroo, and the author of a book that has become a practical reference for young Australians navigating ETFs, superannuation and property. What separates her from the crowded field of money educators is precision: she does not talk in principles when she can talk in percentages.

2- Alan Kohler – Editor-in-Chief, Eureka Report; Editor-in-Chief, InvestSMART Group; ABC News finance presenter, host of Inside Business.

If Queenie Tan represents the new wave of personal finance creators, Alan Kohler represents something the new wave will spend decades trying to build: institutional credibility that has survived multiple economic cycles. As Editor-in-Chief of the Eureka Report and InvestSMART Group, and a decades-long presence on ABC News, Kohler has spent more than thirty years making financial analysis accessible without dumbing it down.

His coverage of RBA decisions, market movements and economic policy is cited by podcasters, journalists and fund managers alike. He is not chasing virality. He does not need to.

3- Aleks Nikolic – Corporate lawyer; host, Big Swinging Stocks podcast

Most finance creators address the mechanics of money. Aleks Nikolic addresses the psychology — and that distinction explains why her following is as loyal as it is. Operating as Broke Girl Wealth across Instagram, TikTok and YouTube, Nikolic covers ETFs, crypto and investment strategy, but her real differentiator is a willingness to discuss the emotional architecture of financial decision-making.

Shame around debt. Fear around market volatility. The limiting beliefs that stop people acting on what they already know. In a space where confidence is routinely performed, her candour is a genuine competitive advantage.

4- Bryce Leske & Alec Renehan – Equity Mates Media

Equity Mates did not build a following. They built a media company. What began as a podcast by two friends learning to invest has grown into Australia’s most established investing media brand, covering ASX stocks, ETFs, global markets and fund manager interviews across podcast, social and YouTube.

The longevity is the credential. Equity Mates has operated through multiple market cycles, a global pandemic, and a generational shift in how Australians engage with investing — and its audience has grown through all of it. When the hosts speak, their listeners know they have been paying attention for years.

5- The Lazy CEO – CEO & Founder, Showpo; Shark Tank Australia investor

The metric that matters most on social media is not followers — it is engagement, because engagement signals trust. Jane Lu, known as The Lazy CEO, maintains an engagement rate of approximately 1.15 per cent on Instagram, which is exceptional for a finance account of his size. Her 242,000-plus followers are not passive consumers: they ask questions, share experiences and apply what they read.

Her content focuses on business finance and wealth building, and the active comment sections are the clearest possible evidence that her audience does not merely scroll past.

6- Tash Invests – Founder, Tash Lends; Forbes Australia 30 Under 30

Tash Invests built her following on a premise that sounds simple but is rarer in practice than it should be: she publishes the actual numbers. Not approximations or ranges or anonymised case studies — her salary, her savings rate, her portfolio value, her net worth, updated and on the record.

Having bought her first property at twenty-two and grown her documented net worth past $1 million, she has become the primary reference point for young Australians trying to understand what building wealth on a moderate income genuinely looks like. The specificity is the product.

7- David Scutt – APAC Market Analyst at StoneX Group

The authority of most finance social media content rests on research and reading. David Scutt‘s authority rests on having done the job. A former Treasury Dealer at Arab Bank and the Commonwealth Bank, former ASX Business Supervisor, and former Global Markets Editor at Business Insider Australia and anchor at ausbiz TV, Scutt now brings that direct market experience to his role as APAC Market Analyst at StoneX Group, rather than relying on secondary commentary.

When he discusses foreign exchange movements or ASX dynamics, it is not because he has read about them. It is because he has traded them.

8- Meddy Demars – Investing & crypto content creator

The gap Meddy Demars fills is specific and underserviced: connecting global macroeconomic events to the practical reality of Australian investors. When the US Federal Reserve adjusts interest rates, when inflation data moves, when commodity prices shift — most Australian finance content either ignores the local implications or translates them poorly.

Demars, operating across TikTok and Instagram from Sydney, does the translation well: explaining what global conditions mean for Australian stocks, savings rates and investment portfolios in terms that are accessible without being condescending.

9- Simran Kaur – Founder, Friends That Invest

Friends That Invest is arguably the most successful community-building exercise in Australian personal finance, and Simran Kaur is the reason why. The New Zealand-based creator — whose audience is predominantly Australian — built a podcast, a book and a social media presence around a single insight: that the personal finance world was not speaking to young women, and that the consequences of that gap were significant.

The measurable cultural shift that followed — women engaging with investing concepts in communities that had not previously existed — is the kind of impact that most financial literacy programmes aim for and rarely achieve.

10- Effie Zahos – Money Editor at 9News

Effie Zahos is one of Australia’s most recognised financial commentators, appearing regularly across 9News, A Current Affair, Today and Today Extra as 9News Money Editor. Her role puts everyday money questions, from mortgage rates to cost-of-living pressures, in front of a national broadcast audience.

Before television, she spent years as editor of Money magazine, building the editorial foundation for her current commentary. She is also Director and Money Commentator at InvestSMART, an ambassador for Canstar, and a published author, with her financial advice available in print as well as on screen.

That combination, decades of editorial experience, an active broadcast presence, and a body of published work, is what makes her commentary carry weight beyond any single platform or post.

From snow-dusted valleys to festival-filled autumns, Bhutan reveals itself as a rare destination where culture, nature and spirituality unfold year-round.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.