Your Old Clothes Are Worth Billions

Secondhand apparel retail is a booming business, but turning a profit is harder than it sounds

3 min

3 min

Closets are full of unworn clothes ready for purging, thrifting is in vogue , and everybody’s looking for a good deal these days. It all sounds like a golden business opportunity—if anyone can figure it out.

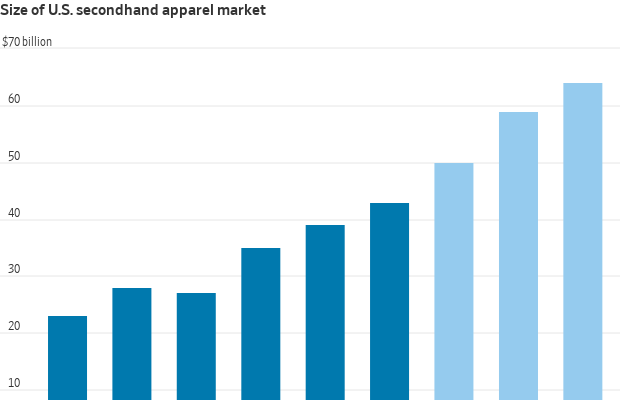

Americans on average throw away some 70 pounds of clothes a year, and thrifting is becoming more popular by the day—particularly among younger consumers. The U.S. secondhand apparel market was worth about $43 billion last year, according to an annual market report from the online apparel reseller ThredUp . It estimates that the market could grow about 11% a year on average through 2028. The market is fragmented, with about 74% of thrift stores being independently run, according to a report from Piper Sandler.

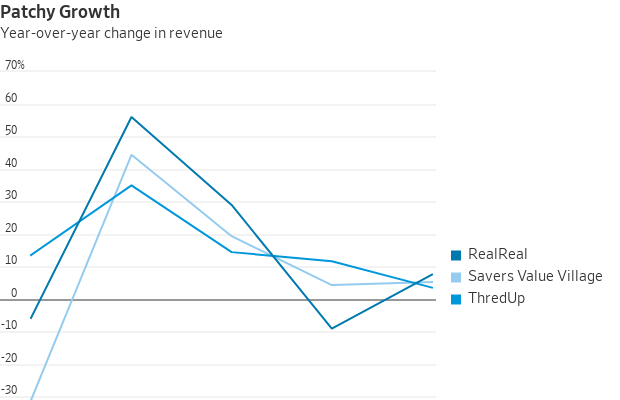

Companies specialising in thrift, though, are struggling to stitch together a compelling investment case. Shares of the online seller ThredUp and the bricks-and-mortar thrift-store chain Savers Value Village are each down around 29% year to date. The luxury online resale platform RealReal has fared better, but in large part thanks to a debt exchange it announced in late February to address liquidity concerns. ThredUp and RealReal are both down significantly from their peaks a few years back.

This could simply be air coming out of highly inflated expectations. ThredUp and the RealReal made their debuts with much fanfare in 2021 and 2019, respectively. Savers listed last year with a lofty valuation. But sales growth for all three companies has slowed, and they are all growing slower than the overall market.

Nonprofits such as Goodwill control a sizeable portion of the secondhand market, with a steady supply of donations, and eBay dominates the resale market online. ThredUp and RealReal’s bet is that consignors and buyers would be willing to pay a premium for a more convenient selling and buying experience. Sellers need only mail in or drop off their goods, and the platforms do the work of photographing, pricing and tagging each item by size, brand, colour and condition so that items are easily searchable. For RealReal, there is an extra human step of making sure the products aren’t fakes. A single-item distribution system is difficult to recreate and is therefore a powerful moat, says Dylan Carden, an equity analyst at William Blair, referring to ThredUp.

But the expensive process also means profitability is distant: Neither ThredUp nor RealReal is expected to turn a profit on the basis of generally accepted accounting principles for the next four years, according to analyst estimates polled by Visible Alpha.

Balancing the quantity of supply with quality has been difficult. ThredUp last year introduced fees that are subtracted from the payout customers receive if their items are sold on the platform. The change is meant to encourage consumers to send in high volumes of high-quality clothes. RealReal last year tweaked its commission structure to motivate consignors to send in expensive items priced above $100.

While these moves could attract higher quality, they might also divert consignors to platforms such as Poshmark and eBay, where selling involves more work but potentially higher payout. Notably, both of those marketplaces have authentication features for high-end items, and eBay has been trying to simplify sellers’ listing process through generative AI .

Meanwhile, the bricks-and-mortar Savers comes with the promise of a more efficient shopping experience than nonprofits. Piper Sandler estimates that its sales per store is nearly twice that of Goodwill and more than six times that of the Salvation Army. But the retailer faces similar quality challenges.

Only about half the items that Savers gets actually end up on the sales floor, and of those about half actually are sold, according to a company filing. Savers receives all of its items—whether directly or indirectly—by paying nonprofits by the pound for donated products. Savers has previously said that it might be able to snag higher-quality donations by placing its drop-off trailers—known as GreenDrop—near locations frequented by wealthier shoppers.

While Savers has been profitable for the past three years, same-store sales have unexpectedly slowed in recent quarters, and its investment case is highly dependent on new-store growth. This remains a risk. Previous management had trouble opening up stores because they weren’t able to procure enough supplies of secondhand clothing, notes Peter Keith, equity analyst at Piper Sandler, who is still confident about the company’s ability to expand.

Much like that shirt you only wore once, secondhand-apparel sellers so far hold more promise than substance.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

Automobili Lamborghini and Babolat have expanded their collaboration with five new colourways for the ultra-exclusive BL.001 racket, limited to just 50 pieces worldwide.

A haven for hedge-fund titans and Hollywood grandees, Greenwich is one of the world’s most expensive residential enclaves, where eye-watering prices meet unapologetic grandeur.