The Art Market Is Tanking. Sotheby’s Has Even Bigger Problems.

The auction house, owned by highly leveraged billionaire Patrick Drahi, is pushing off payments, awaiting a financial lifeline from an Abu Dhabi fund

10 min

10 min

The art market is grinding through a rough patch, and no one is feeling the pain more than Sotheby’s.

The sales downturn, driven in part by China’s economic slowdown, wars and volatile U.S. elections, has hit at a crunchtime for the auction house’s highly leveraged billionaire owner, Patrick Drahi , who is fighting fires amid restructuring in his broader telecom empire, Altice .

Sotheby’s had been riding a rollicking art market wave in recent years, bringing in at least $7 billion in sales annually and setting record-level prices for trophies by Gustav Klimt and René Magritte.

Now, amid signs cash is running low, it is pushing off payments to its art shippers and conservators by as much as six months. Several former and current employees said Sotheby’s this spring gave senior staffers IOUs instead of their incentive pay. And at a meeting this month of higher-ranking executives, some executives expressed worries about whether the company would be able to keep paying its employees on time, according to a person familiar with the discussion.

Drahi has at the same time been under pressure to slash the crushing debt of roughly $60 billion at Altice. The conglomerate’s French arm is now going through restructuring talks with creditors, with the U.S. arm expected to enter restructuring talks later. Some Wall Street analysts had hoped Drahi might sell part of Sotheby’s to help bolster Altice.

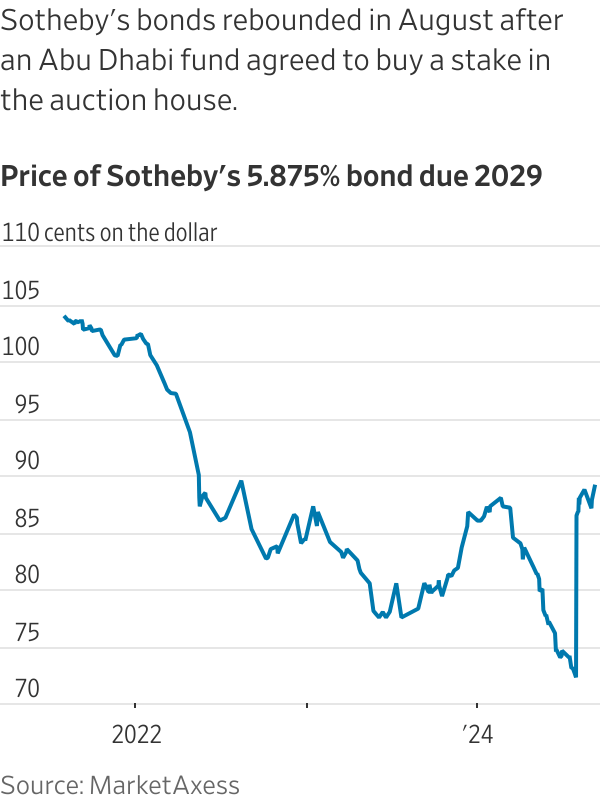

Sotheby’s itself carries $1.8 billion in debt, almost double the level it had before the Franco-Israeli billionaire purchased it in 2019. The value of its bonds swooned in the first half of the year as investors worried that declining sales and higher interest rates would choke off the company’s cash flow.

The auction house received a lifeline with a $1 billion deal to sell a stake to Abu Dhabi sovereign-wealth fund ADQ , announced Aug. 9 but not expected to close until later this year. At the time, Drahi said he would contribute an undisclosed amount as part of the deal.

As it awaits the funds, Sotheby’s is toeing a high-wire act with an uncertain outcome.

Charles Stewart , Sotheby’s chief executive, dismissed fears about Sotheby’s financial standing as overblown, and the company disputed the meeting with higher-ranking executives occurred. Stewart said the company’s bonds, which have rebounded in price since the ADQ rescue was announced, are proof that Sotheby’s has smoothed over any worries. He said the ADQ investment will position the house for growth moving forward. “It’s a massive credit positive,” he said.

A Sotheby’s spokeswoman said: “Under Mr. Drahi’s ownership, Sotheby’s is significantly larger, more diversified and more profitable than ever before. During this period, we have invested hundreds of millions to enhance our facilities, technology and expand our offerings to clients.”

ADQ declined to comment.

The crisis at Sotheby’s comes at a time when the entire art market is reeling . Over the past year, collectors who see art as a financial asset have winced as higher interest rates and inflation made it more expensive to trade art. Contemporary art buyers have also suffered sticker shock after years of paying ever-higher prices for emerging artists—who may never pay off. Some smaller galleries, who rely on collectors to vouch for unknown artists, have shuttered, while dealers have reported lacklustre sales at art fairs.

Those factors have hurt collectors’ overall confidence. “I don’t feel like there’s a bunch of collectors waiting out there to save the day this time,” said Dallas collector Howard Rachofsky.

Growing debt load

Drahi, 61 years old, is famous for taking on a mountain of debt to build telecommunications empire Altice, which operates in the U.S. and Europe. He borrowed from Wall Street when interest rates were low, but now that rates have risen sharply, he has started selling off chunks of his companies to lower his debt burden. Last month, his Altice UK sold a 24.5% stake in its BT Group to the Indian international investment arm of Bharti Enterprises in a deal valued at roughly $4 billion.

Drahi used a similar high-debt strategy to buy Sotheby’s in 2019 for $2.7 billion. Drahi issued $1.1 billion in new bonds and loans to finance the deal, and separately also assumed some portion of Sotheby’s existing $1 billion debt.

He has since spent lavishly, including signing a deal to pay at least $100 million for New York’s Breuer building, a Madison Avenue showpiece once home to the Whitney Museum of American Art and temporarily used by both the Metropolitan Museum of Art and Frick Collection. The company is planning to move in at the end of next year and to lease out part of its current glassy headquarters closer to the East River in Manhattan. Sotheby’s has spent tens of millions more to renovate new luxury-retail-style spaces in Paris and Hong Kong.

Drahi also expanded Sotheby’s ability to auction multimillion-dollar homes by buying a chunk of real-estate seller Concierge, and added RM Sotheby’s, an entity that sells high-end cars.

At the same time, the owner has pulled funds out of the company via dividends. In total since the purchase, Sotheby’s has paid out $1.2 billion of dividends to a parent company controlled by Drahi, according to New Street Research.

The ballooning debt didn’t draw much attention during flush years when an influx of newly wealthy collectors from across China, Russia, the Middle East and even the world of cryptocurrency were clamouring after Sotheby’s offerings.

That changed when the market cooled. Sotheby’s told its bondholders the auction portion of the business had a loss of $115 million in the first half of the year, compared to a $3 million profit in the first half of 2023, according to a copy of Sotheby’s unaudited financials for the first half of the year reviewed by The Wall Street Journal.

Rival Christie’s, owned by luxury magnate François Pinault , has also taken a hit, with its auction sales dropping nearly a quarter during the first half of the year.

Sotheby’s adjusted operating free cash flow fell to $144 million in the 12 months ended June 30, a 43% decline from the same time last year, according to data from New Street Research. The figure measures whether a company is making enough money to pay its bills and turn a profit.

Credit rating firm Moody’s Investors Service in February knocked down the ratings for Sotheby’s bonds to B3, one of its lowest categories of junk debt, specifically citing the dividends paid out. “The downgrade also reflects governance considerations, particularly the company’s decision to continue dividend payments out of its credit group in 2023 despite its operating performance deterioration,” Moody’s said in its decision. S&P downgraded the debt into deep junk territory in June.

Stewart said the company’s credit rating has been lower since the Drahi purchase. He said its updates to bondholders revolve around its auction performance only and don’t include fees from the company’s real-estate holdings or financial-services arm, which Stewart said remain in the black. He declined to divulge the company’s full financial figures.

Stewart also said the dividends remain in the Sotheby’s ecosystem and aren’t being redirected to shore up Drahi or his other businesses.

Drahi’s arrival

Sotheby’s was flush with cash but lagging behind Christie’s in 2018 when Tad Smith, the auction house’s then-CEO, suggested to his board that it find a buyer. The company had been public for three decades, but Smith believed the demands for public shareholder returns hampered its ability to go toe-to-toe with the bigger and privately held Christie’s.

In early 2019, the board let Smith make overtures to prospective buyers, including an entity connected to Abu Dhabi’s royal family that expressed interest, according to a person familiar with the negotiations. Drahi moved more quickly and emerged as the winner.

At first, the art establishment didn’t know much about Drahi. The self-made billionaire was born in Morocco, educated in France and has homes in Switzerland and Israel. He was familiar to Sotheby’s staffers in their Tel Aviv office but wasn’t widely known in art circles.

At the time, he was a traditional collector of 19th- and 20th-century artists rather than trendier, contemporary ones, owning pieces by Pablo Picasso, Henri Matisse and Marc Chagall. But he didn’t sit on major museum boards or pop up regularly on the art-fair circuit.

The Sotheby’s purchase marked Drahi’s first foray into luxury. The art world wondered if he would manage a house that started off auctioning books in London in 1744 the same way he ran his broadband communications companies, where he was known for aggressively cutting costs and using debt to fuel ambitious expansions.

Drahi told Sotheby’s he saw the company as an investment for his family, regularly dismissing rumors he was teeing up Sotheby’s to be resold. In 2021, Sotheby’s promoted his son Nathan, then 26, to run Sotheby’s operations in Asia, a key market.

As part of the sale, Sotheby’s divided its various endeavors—such as its real-estate arm and its financial services arm, which lends against people’s art collections—into affiliated but separate entities from the main unit, which handles Sotheby’s auctions and private art sales.

Stewart said Drahi’s move was intended to keep each division nimble.

The art-world ecosystem noticed Drahi’s arrival in other ways. Soon after the sale, a network of smaller companies that auction houses typically enlist to conserve, frame, crate and ship its art around the world said they got word that the house would be lengthening its pay schedules, from a typical month to two or more. One conservator said payments started to arrive six months after a job was completed.

Sotheby’s also started paying sellers more slowly than its rivals. In the past, both Sotheby’s and Christie’s asked winning bidders to pay for their pieces within 30 business days of a sale, and then paid sellers five days later. Sotheby’s changed its contracts to allow it to pay sellers 15 days later, according to sellers familiar with the house’s contracts. The move allowed the house to hold the funds in its coffers longer.

Sotheby’s said its processing deadlines have been in place for many years to allow the company to adequately process payments.

Pay for top talent

When the pandemic hit, Drahi and his management team reoriented the company to sell art online, a pivot Sotheby’s is credited with embracing faster than its rivals.

Sotheby’s also started laying off staff during the lockdown, and continued to do so after the pandemic. When the ever-swirling calendar of fairs and museum openings and biennials got under way again, advisers including Philip Hoffman of the Fine Art Group said they noticed fewer Sotheby’s staffers turned up. The company would send one or two rainmakers, not a whole team.

Stewart confirmed the pandemic-related staff cuts “like many other companies” and winnowed travel were meant to make the company more efficient, though he said it remains “mission critical” to put its top specialists in front of collectors.

Drahi needed Sotheby’s key dealmakers to remain in place. High-end art deals at auction houses are wrangled primarily by a handful of executives and specialists able to cultivate an air-kiss closeness with collectors. They also must be able to discern a fake Picasso from a real one, and price it to sell well in good markets and bad.

In 2021, Drahi revised the incentive pay program for these top performers. In exchange for accepting an immediate pay cut of up to 20%, employees were told they could expect a cash payout in three years based on the company’s performance and representing up to half of their total compensation.

Some powerful executives still left, dealing a blow to the auction house. Patti Wong , Sotheby’s former international chairman for Asia, now works as a private adviser, and Brooke Lampley , its former global chairman of fine art, is now a senior director at the blue-chip gallery Gagosian.

When the delayed payout came due, staff were told in conference calls—some say last fall and others say in March—that it needed to be postponed; enrollees were issued promissory notes this spring instead, according to several former and current specialists. Specialists said they now are hoping to get paid by year’s end with a portion of the Abu Dhabi funds.

The company disputed the description of the incentive program but declined to give further details.

New fees for sellers

In February, Sotheby’s shocked the art world when it fundamentally restructured the way it collects fees for works that it auctions.

Both Sotheby’s and Christie’s, in efforts to bring sellers to their doors, often waived their fees. They even shared with sellers increasingly fatter slices of the fees they charge buyers—which can add up to roughly 27% to a work’s winning price.

At the same time, buyers have bristled over the fees they pay. Rachofsky, the Dallas collector, said he has long agitated that “auction fees are unsustainably high.”

Sotheby’s new fee plan, which went live in late May, now charges buyers a flat 20% for anything it sells for $6 million or less, and 10% for anything it sells for more. For sellers, Sotheby’s charges a fee of 10% on the first $500,000 of anything it sells for $5 million or less. Terms for larger deals continue to be negotiated.

Christie’s and smaller house Phillips said they also charge an undisclosed seller’s commission, but their fee is negotiable.

Stewart said the goal is to create a system that is “simpler and fairer.”

It’s too soon to tell if Sotheby’s new fee structure will help or hamper its effort to win consignments. Sotheby’s has landed the prized estate of the season, an estimated $200 million collection amassed by Palm Beach beauty mogul Sydell Miller that includes a Claude Monet water lily scene estimated to sell for $60 million. The collection will headline the November sales.

Art adviser Anthony Grant said one of his collectors reasons that Sotheby’s might hustle harder to find bidders for each work now that they’re charging sellers a fee to do so. But Grant said he worries the change could also steer sellers of midmarket pieces to other houses who may not charge them extra for anything.

“It’s one more thing that’s gotten harder for them,” he said of Sotheby’s, where he once worked.

Asia is expected to play a crucial role in Sotheby’s prospects. In recent years, newly wealthy bidders in Asia—spanning mainland China to Seoul to Singapore—have been relied upon to mop up art at the highest levels even when collectors elsewhere held back. Now, China’s economy has slowed, sparking fears about its buyers’ willingness to splurge on blue-chip art.

Instead of scaling back, the major auction houses are all doubling down on the region. Sotheby’s and Christie’s both just opened luxurious new spaces in Hong Kong. Sotheby’s Maison space in Hong Kong’s Central neighborhood, opened in late July, said it has already had 300,000 visitors.

This month, on the eve of what was supposed to be its inaugural fall sale series in Hong Kong, the house announced it was pushing back these sales to November. Advisers who work in the region said the move left the impression that the house had failed to gather enough marquee material.

Sotheby’s said the calendar shift gives it more time to organise shows and a sale lineup, and said the delay wasn’t because the art was too tough to source. It cited its plan to sell an estimated $30 million Mark Rothko from 1954, “Untitled (Yellow and Blue),” in Hong Kong later this year.

Collector and dealer Hong Gyu Shin initially consigned an Oscar Wilde manuscript of “The Picture of Dorian Gray” to Sotheby’s to offer in its Hong Kong sales, he said, but he later changed his mind. He said he wanted the auction house to revel in the piece, which contains Wilde’s own handwritten edits, and he wanted to brainstorm the best way to position it to buyers. Instead, there was little conversation after the paperwork was signed.

“Specialists used to be so excited,” he said, “but now they just slap an estimate on it. When you have historical work, it’s a form of art to sell it.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

The voices reshaping how Australians think about money — and why credibility matters more than reach.

6 min

The best financial advice many Australians are receiving right now is not coming from licensed advisers charging by the hour. It is coming through a phone screen, in the ten minutes between work and dinner, from creators who have built credibility the hard way: by being right, being transparent, and being specific in a space where vagueness has always been the easy default.

This is not a ranking by follower count. Follower count is a measure of distribution, not of quality. What follows is a ranking by substance — credentials, accuracy, community depth, and the quality of what an audience actually learns from following these accounts. The distinction matters, because the Australians acting on this content are making real financial decisions with real money.

1- Queenie Tan – Corporate Authorised Representative; Co-Founder & Director, Invest With Queenie & Billroo

There are finance influencers who talk about building wealth, and there are those who document it in real time with receipts. Queenie Tan belongs firmly in the second category. Starting from a $400-per-week income, Tan built her net worth past $1 million while publishing the actual numbers — income, savings rate, investment decisions — for an audience of more than 400,000 across platforms.

She is a Corporate Authorised Representative, co-founder of the personal finance app Billroo, and the author of a book that has become a practical reference for young Australians navigating ETFs, superannuation and property. What separates her from the crowded field of money educators is precision: she does not talk in principles when she can talk in percentages.

2- Alan Kohler – Editor-in-Chief, Eureka Report; Editor-in-Chief, InvestSMART Group; ABC News finance presenter, host of Inside Business.

If Queenie Tan represents the new wave of personal finance creators, Alan Kohler represents something the new wave will spend decades trying to build: institutional credibility that has survived multiple economic cycles. As Editor-in-Chief of the Eureka Report and InvestSMART Group, and a decades-long presence on ABC News, Kohler has spent more than thirty years making financial analysis accessible without dumbing it down.

His coverage of RBA decisions, market movements and economic policy is cited by podcasters, journalists and fund managers alike. He is not chasing virality. He does not need to.

3- Aleks Nikolic – Corporate lawyer; host, Big Swinging Stocks podcast

Most finance creators address the mechanics of money. Aleks Nikolic addresses the psychology — and that distinction explains why her following is as loyal as it is. Operating as Broke Girl Wealth across Instagram, TikTok and YouTube, Nikolic covers ETFs, crypto and investment strategy, but her real differentiator is a willingness to discuss the emotional architecture of financial decision-making.

Shame around debt. Fear around market volatility. The limiting beliefs that stop people acting on what they already know. In a space where confidence is routinely performed, her candour is a genuine competitive advantage.

4- Bryce Leske & Alec Renehan – Equity Mates Media

Equity Mates did not build a following. They built a media company. What began as a podcast by two friends learning to invest has grown into Australia’s most established investing media brand, covering ASX stocks, ETFs, global markets and fund manager interviews across podcast, social and YouTube.

The longevity is the credential. Equity Mates has operated through multiple market cycles, a global pandemic, and a generational shift in how Australians engage with investing — and its audience has grown through all of it. When the hosts speak, their listeners know they have been paying attention for years.

5- The Lazy CEO – CEO & Founder, Showpo; Shark Tank Australia investor

The metric that matters most on social media is not followers — it is engagement, because engagement signals trust. Jane Lu, known as The Lazy CEO, maintains an engagement rate of approximately 1.15 per cent on Instagram, which is exceptional for a finance account of his size. Her 242,000-plus followers are not passive consumers: they ask questions, share experiences and apply what they read.

Her content focuses on business finance and wealth building, and the active comment sections are the clearest possible evidence that her audience does not merely scroll past.

6- Tash Invests – Founder, Tash Lends; Forbes Australia 30 Under 30

Tash Invests built her following on a premise that sounds simple but is rarer in practice than it should be: she publishes the actual numbers. Not approximations or ranges or anonymised case studies — her salary, her savings rate, her portfolio value, her net worth, updated and on the record.

Having bought her first property at twenty-two and grown her documented net worth past $1 million, she has become the primary reference point for young Australians trying to understand what building wealth on a moderate income genuinely looks like. The specificity is the product.

7- David Scutt – APAC Market Analyst at StoneX Group

The authority of most finance social media content rests on research and reading. David Scutt‘s authority rests on having done the job. A former Treasury Dealer at Arab Bank and the Commonwealth Bank, former ASX Business Supervisor, and former Global Markets Editor at Business Insider Australia and anchor at ausbiz TV, Scutt now brings that direct market experience to his role as APAC Market Analyst at StoneX Group, rather than relying on secondary commentary.

When he discusses foreign exchange movements or ASX dynamics, it is not because he has read about them. It is because he has traded them.

8- Meddy Demars – Investing & crypto content creator

The gap Meddy Demars fills is specific and underserviced: connecting global macroeconomic events to the practical reality of Australian investors. When the US Federal Reserve adjusts interest rates, when inflation data moves, when commodity prices shift — most Australian finance content either ignores the local implications or translates them poorly.

Demars, operating across TikTok and Instagram from Sydney, does the translation well: explaining what global conditions mean for Australian stocks, savings rates and investment portfolios in terms that are accessible without being condescending.

9- Simran Kaur – Founder, Friends That Invest

Friends That Invest is arguably the most successful community-building exercise in Australian personal finance, and Simran Kaur is the reason why. The New Zealand-based creator — whose audience is predominantly Australian — built a podcast, a book and a social media presence around a single insight: that the personal finance world was not speaking to young women, and that the consequences of that gap were significant.

The measurable cultural shift that followed — women engaging with investing concepts in communities that had not previously existed — is the kind of impact that most financial literacy programmes aim for and rarely achieve.

10- Effie Zahos – Money Editor at 9News

Effie Zahos is one of Australia’s most recognised financial commentators, appearing regularly across 9News, A Current Affair, Today and Today Extra as 9News Money Editor. Her role puts everyday money questions, from mortgage rates to cost-of-living pressures, in front of a national broadcast audience.

Before television, she spent years as editor of Money magazine, building the editorial foundation for her current commentary. She is also Director and Money Commentator at InvestSMART, an ambassador for Canstar, and a published author, with her financial advice available in print as well as on screen.

That combination, decades of editorial experience, an active broadcast presence, and a body of published work, is what makes her commentary carry weight beyond any single platform or post.

By improving sluggish performance or replacing a broken screen, you can make your old iPhone feel new agai

From mud baths to herbal massages, Fiji’s heat rituals turned one winter escape into a soul-deep reset.