Americans in Their Prime Are Flooding Into the Job Market

Share of people between 25 and 54 working or seeking jobs rose this year to highest level since 2002

4 min

4 min

The core of the American labour force is back.

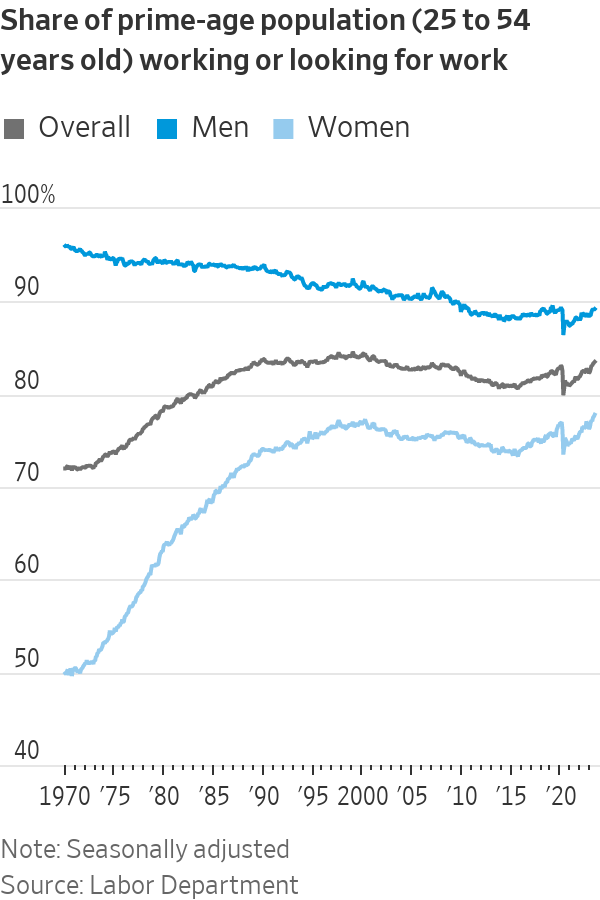

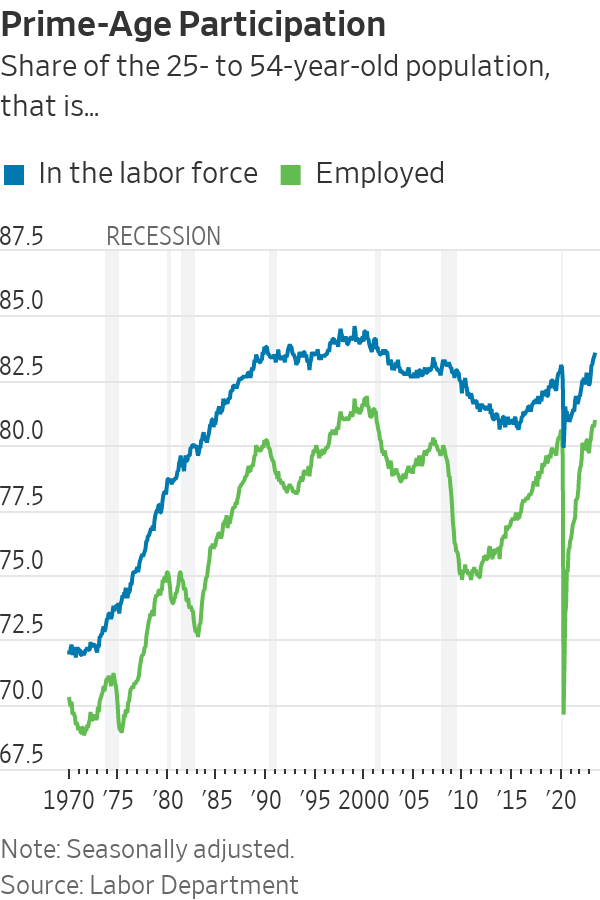

Americans between 25 and 54 years of age are either employed or looking for jobs at rates not seen in two decades, a trend helping to counter the exodus of older baby boomers from the workforce. Economists define that age range as in their prime working years—when most Americans are done with their formal education, aren’t ready to retire and tend to be most attached to the labor force.

In the first months of the pandemic, nearly four million prime-age workers left the labor market, pushing participation in early 2020 to the lowest level since 1983—before women had become as much of a force in the workplace. Prime-age workers now exceed pre pandemic levels by almost 2.2 million.

That growth is taking a little heat out of the job market and could help the Federal Reserve’s efforts to tamp down inflation by keeping wage growth in check.

Women lead the way

The resurgence of mid career workers is driven by women taking jobs.

The labor-force participation rate for prime-age women was the highest on record, 77.8% in June. That is well up from 73.5% in April 2020.

Men, however, tend to be employed at higher rates. The overall prime-age participation rate rose in June to 83.5%, the highest since 2002.

The big draw: a tight labor market. The unemployment rate has hovered near a half-century low for more than a year, and job openings outnumber the ranks of unemployed. Employers can’t be as choosy or selective, William Rodgers, vice president and director of the Institute for Economic Equity at the St. Louis Fed, said earlier this month.

Employers “are more apt to be willing to work with candidates—in this case it’s working with moms, or parents in general,” he said. “Tight labor markets can help to punish those who discriminate in hiring and compensation.”

Other factors are also at play. Women aren’t having as many children—there were about 3.66 million births in 2022, 655,000 fewer than the peak in 2007—so child-care responsibilities have decreased.

Julia Pollak, chief economist at ZipRecruiter, said it is possible for women’s participation to rise further if employers adopt or the government requires additional family-friendly policies. U.S. female participation lags behind that of other industrialised economies in part because of the cost of child care, which is subsidised elsewhere.

Rising wages lure workers, counter demographic shifts

Employers raised wages, offered employees more flexibility and improved benefits in recent years.

Average wage gains remain elevated this year and have recently surpassed inflation. And Americans are logging more hours of work from home than they did before the pandemic.

Employer recruitment efforts helped offset some broader demographic shifts, including an ageing population and rise in retirements.

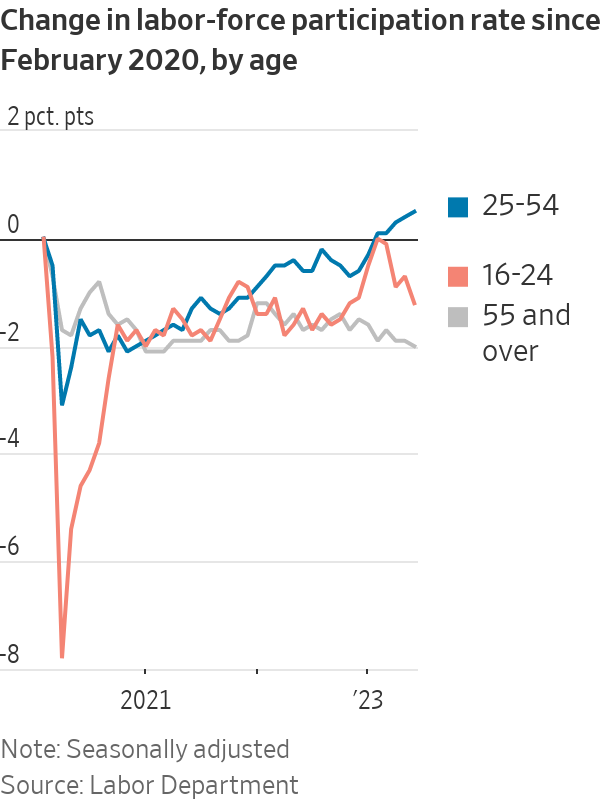

The share of the population age 55 and over in the labor force climbed steadily from the mid-1990s through the 2008 financial crisis and remained elevated for more than a decade. The Covid-19 pandemic pushed many out of the workforce, and some older workers haven’t returned, particularly those over 65.

Much of the decline in the overall participation rate was anticipated as baby boomers aged out of the workforce, but the rise in prime-age workers meant the drop wasn’t as steep.

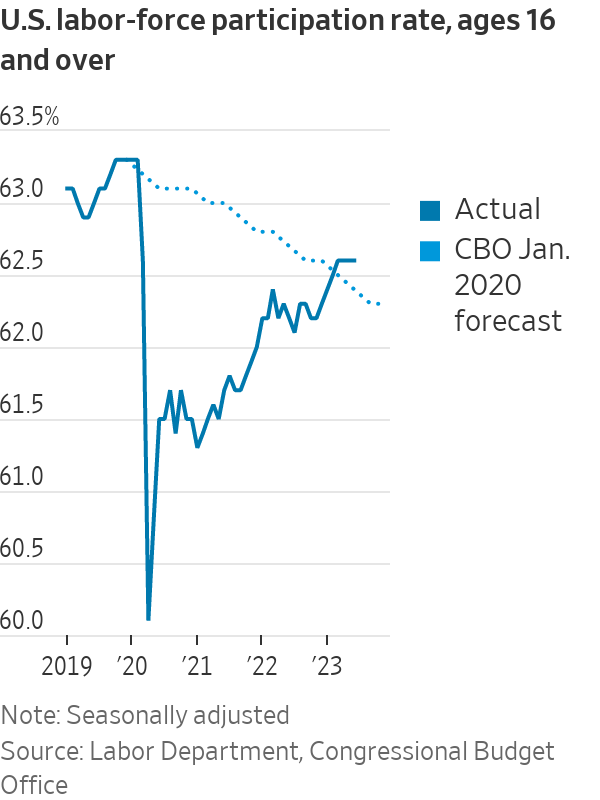

The Congressional Budget Office in January 2020, just before the pandemic hit, forecast the overall participation rate to deteriorate steadily through the 2020s, moving down to 62.4% in the second quarter of this year.

Instead, the rate was a couple of ticks higher in June at 62.6%, supported by prime-age workers.

“It seems like there is almost no cap on the supply of workers, only a speed limit on how fast we can bring them in,” Pollak said, referring to both rising prime-age participation and an influx of immigrants into the workforce.

Trends could turn if the economy cools

There are concerns that the Fed’s campaign to bring down inflation through higher interest rates will cause unemployment to rise too much and push some of the most vulnerable workers back to the sidelines.

The median forecast among Fed officials shows the unemployment rate rising to 4.1% by the end of this year and 4.5% next year from 3.6% in June, suggesting the economy will shed tens of thousands of jobs.

Labor-force participation tends to be cyclical, rising when the economy is strong and falling during downturns. A weaker labor market combined with structural barriers to employment could cap further gains.

With “current strength of labor demand set to fade, further progress from here will probably be more gradual,” Andrew Hunter, deputy chief U.S. economist at Capital Economics, said in a research note.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

This stylish family home combines a classic palette and finishes with a flexible floorplan

Just 55 minutes from Sydney, make this your creative getaway located in the majestic Hawkesbury region.

When will Berkshire Hathaway stop selling Bank of America stock?

3 minBerkshire began liquidating its big stake in the banking company in mid-July—and has already unloaded about 15% of its interest. The selling has been fairly aggressive and has totaled about $6 billion. (Berkshire still holds 883 million shares, an 11.3% interest worth $35 billion based on its most recent filing on Aug. 30.)

The selling has prompted speculation about when CEO Warren Buffett, who oversees Berkshire’s $300 billion equity portfolio, will stop. The sales have depressed Bank of America stock, which has underperformed peers since Berkshire began its sell program. The stock closed down 0.9% Thursday at $40.14.

It’s possible that Berkshire will stop selling when the stake drops to 700 million shares. Taxes and history would be the reasons why.

Berkshire accumulated its Bank of America stake in two stages—and at vastly different prices. Berkshire’s initial stake came in 2017 , when it swapped $5 billion of Bank of America preferred stock for 700 million shares of common stock via warrants it received as part of the original preferred investment in 2011.

Berkshire got a sweet deal in that 2011 transaction. At the time, Bank of America was looking for a Buffett imprimatur—and the bank’s stock price was weak and under $10 a share.

Berkshire paid about $7 a share for that initial stake of 700 million common shares. The rest of the Berkshire stake, more than 300 million shares, was mostly purchased in 2018 at around $30 a share.

With Bank of America stock currently trading around $40, Berkshire faces a high tax burden from selling shares from the original stake of 700 million shares, given the low cost basis, and a much lighter tax hit from unloading the rest. Berkshire is subject to corporate taxes—an estimated 25% including local taxes—on gains on any sales of stock. The tax bite is stark.

Berkshire might own $2 to $3 a share in taxes on sales of high-cost stock and $8 a share on low-cost stock purchased for $7 a share.

New York tax expert Robert Willens says corporations, like individuals, can specify the particular lots when they sell stock with multiple cost levels.

“If stock is held in the custody of a broker, an adequate identification is made if the taxpayer specifies to the broker having custody of the stock the particular stock to be sold and, within a reasonable time thereafter, confirmation of such specification is set forth in a written document from the broker,” Willens told Barron’s in an email.

He assumes that Berkshire will identify the high-cost Bank of America stock for the recent sales to minimize its tax liability.

If sellers don’t specify, they generally are subject to “first in, first out,” or FIFO, accounting, meaning that the stock bought first would be subject to any tax on gains.

Buffett tends to be tax-averse—and that may prompt him to keep the original stake of 700 million shares. He could also mull any loyalty he may feel toward Bank of America CEO Brian Moynihan , whom Buffett has praised in the past.

Another reason for Berkshire to hold Bank of America is that it’s the company’s only big equity holding among traditional banks after selling shares of U.S. Bancorp , Bank of New York Mellon , JPMorgan Chase , and Wells Fargo in recent years.

Buffett, however, often eliminates stock holdings after he begins selling them down, as he did with the other bank stocks. Berkshire does retain a smaller stake of about $3 billion in Citigroup.

There could be a new filing on sales of Bank of America stock by Berkshire on Thursday evening. It has been three business days since the last one.

Berkshire must file within two business days of any sales of Bank of America stock since it owns more than 10%. The conglomerate will need to get its stake under about 777 million shares, about 100 million below the current level, before it can avoid the two-day filing rule.

It should be said that taxes haven’t deterred Buffett from selling over half of Berkshire’s stake in Apple this year—an estimated $85 billion or more of stock. Barron’s has estimated that Berkshire may owe $15 billion on the bulk of the sales that occurred in the second quarter.

Berkshire now holds 400 million shares of Apple and Barron’s has argued that Buffett may be finished reducing the Apple stake at that round number, which is the same number of shares that Berkshire has held in Coca-Cola for more than two decades.

Buffett may like round numbers—and 700 million could be just the right figure for Bank of America.

This stylish family home combines a classic palette and finishes with a flexible floorplan

Just 55 minutes from Sydney, make this your creative getaway located in the majestic Hawkesbury region.