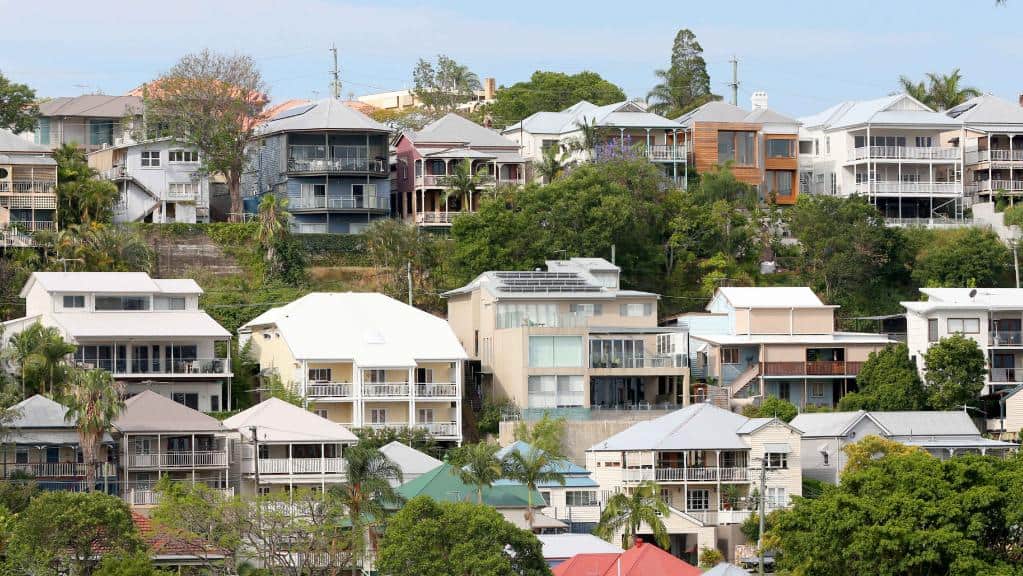

APRA Says House Prices Not Its Job

The prudential regulator has reminded the government of its focus.

< 1 min

< 1 min

The Australian Prudential Regulatory Association (APRA) has told the government its responsibility is financial stability and lending practices, not house prices which are on an unprecedented rise across our nation’s capitals.

The soaring housing prices, which has seen an increase in 2.1% growth in February alone, the fastest pace in almost 17 years, has seen calls for regulators to cool the market.

“It’s not our job to solve house prices and it’s not our job to solve house pricing affordability. The extent to which there is dynamic emerging of increased risk-taking by the community … at this stage it’s not evident,” APRA chairman Wayne Byres told a federal parliamentary committee on Monday.

When questioned at the live-streamed House Standing Committee on Economics hearing, whether the regulator was concerned about young people and first home buyers being priced out of the market Mr Byres reminded the government that the regulator’s focus was on lending practices and not housing.

“I think the bank has been very clear, and we have been very clear, in saying our job is not to set or seek to target house prices,” Mr Byres said.

Mr Byres acknowledged credit restrictions could have a knock-on effect on housing prices, however, reiterated APRA’s position.

“The last statement from the Council of Financial Regulators said quite clearly we are watching for a deterioration in lending standards and that’s not evident at this point,” Mr Byres said. “That is not to say it won’t emerge, but it’s not obvious at this point. We are watching with our fellow regulators.”

This stylish family home combines a classic palette and finishes with a flexible floorplan

Just 55 minutes from Sydney, make this your creative getaway located in the majestic Hawkesbury region.

Money worries are having a cascading effect on stress levels, conflict and even the rate of ageing

3 min

Worrying about the cost of living is causing accelerated ageing, household arguments and creating significant stress, according to new research. More than half of Australians say they have experienced personal setbacks due to financial strain over the past year. Almost 20 percent say that have suffered a stress-related illness, 33 percent have lost sleep and almost one in five are seeing signs of early ageing.

Household hostility is also rising, with 19 percent of Australians admitting they have argued with their partners about money, and a further one in 10 have argued with family and friends.

The Finder survey of 1,070 Australians reveals women are bearing the brunt of financial stress, with 62 percent reporting they have worried about money compared to 42 percent of men.

Younger Australians are struggling the most, with almost 7 in 10 Gen Z respondents reporting financial strain compared to 58 percent of Gen Xers and 24 percent of baby boomers.

The impact of cost-of-living pressures among different age groups and income levels is reflected in new data from the Australian Bureau of Statistics (ABS). The selected living cost indexes show employee households are under more strain from inflation, with the CPI measure for this population group at 6.5 percent today compared to the official overall CPI figure of just 3.6 percent.

The discrepancy is due to higher mortgage interest payments – which make up a higher proportion of expenditure for employee households — as well as an increase in primary and secondary school fees, and the indexation of tertiary education fees at the start of the year. The official CPI does not include mortgage payments, so the living cost indexes provide a more accurate picture of how rising interest rates are impacting households with mortgages today.

The inflation rate is much lower for older Australians, who have often paid off their mortgages. The inflation rate on living expenses for age pensioner households is below the official CPI level at 3.3 percent, and it’s only slightly higher at 3.4 percent for self-funded retirees.

Graham Cooke, head of consumer research at Finder, said that despite cooling inflation, Australians were still under significant financial pressure.

“This can be seen in Finder’s Cost of Living Pressure Gauge, which has been hovering in the extreme range for the past year and a half,” Mr Cooke said. The gauge returned a reading of 78 percent in March this year compared to 47 percent in March 2021, when inflation was 1.1 percent and the Reserve Bank’s official cash rate was 0.1 percent.

Interestingly, Australians’ cash savings are higher today than they were in 2021, likely reflecting stimulus payments received and saved during the pandemic. The Reserve Bank has cited pandemic savings as a factor in keeping mortgage arrears low despite much higher interest rates. The Finder research shows Australians have an average of $37,206 in cash savings today, up from $24,928 two years ago.

“Money concerns can cause problems in your everyday life and snowball quickly if you don’t get them under control,” Mr Cooke said. “Building financial resilience is as vital as ever as costs continue to rise. Pay close attention to where your money is going so you keep impulse spending to a minimum, and don’t overspend.”

Australians appear to be heeding this advice, with the latest ABS retail figures showing seven straight quarters of declining per capita spending. “Per capita volumes show retail turnover after the effects of inflation and population growth have been accounted for,” explained Ben Dorber, ABS head of retail statistics. “Following an unprecedented seven straight falls, it is very clear how much consumers have pulled back on spending in response to cost of living pressures over the past two years.”

Just 55 minutes from Sydney, make this your creative getaway located in the majestic Hawkesbury region.

Consumers are going to gravitate toward applications powered by the buzzy new technology, analyst Michael Wolf predicts