How Hello Kitty Took Over the World

Investors in Sanrio have made 10 times their money as the iconic Japanese brand expands digitally

2 min

2 min")

Hello Kitty is celebrating her 50th birthday this year. Sanrio , the Japanese company behind the iconic character, has much to cheer about too.

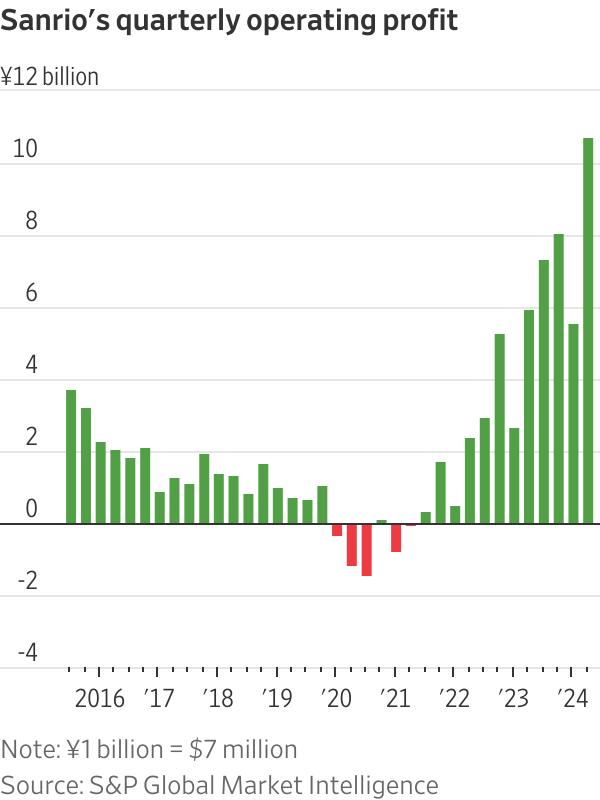

Sanrio’s share price is at a record high after surging 10-fold from its trough in 2020. The company is delivering record profits with strong revenue growth. Operating profit last quarter rose 80% from a year earlier.

Sanrio’s young chief executive, Tomokuni Tsuji —14 years younger than Hello Kitty—probably deserves some applause. He took over the helm from his grandfather in 2020. Sales and profit had been sliding for years when the pandemic arrived. Sanrio had created some of the best-known franchises around the world, but it wasn’t harnessing the full potential of its large portfolio of cute characters.

Tsuji has put younger management in place and finally expanded into the digital world. That includes marketing its characters through social media and other online platforms and ramping up its e-commerce business. It is also expanding its high-margin licensing business, with Sanrio’s characters now gracing products from microwave ovens to sneakers. The licensing business not only is more profitable but also allows more local designs and creates more contact points in overseas markets.

As a result, Sanrio’s business outside of Japan is booming, particularly in China and the U.S. Its profit contribution from abroad, including royalties payment from overseas subsidiaries to the parent company, nearly doubled year on year in the June quarter. Sanrio struck a deal with China’s e-commerce giant Alibaba in 2022 to license its characters in the country. But the U.S. is among its fastest-growing markets: Sales in the Americas grew 141% year on year last quarter. The younger generation is increasingly familiar with Sanrio’s characters given the company’s strong presence on social media.

And the company has also managed to diversify itself away from reliance on Hello Kitty. She has long been Sanrio’s most recognizable character, but the company has developed new characters and done a better job of promoting some existing ones. Hello Kitty accounted for around 30% of Sanrio’s gross profit in product sales and licensing in the fiscal year ended March, compared with 76% a decade earlier. Cinnamoroll, a puppy with white fluffy fur, was voted Sanrio’s top character in an online poll by the company.

The company is also using different types of media to market its characters. It has a Netflix show called “Aggretsuko,” which features an angry red panda struggling with office life, that has been airing for five seasons. A Hello Kitty movie with Warner Bros. is in the making.

Sanrio’s stock now trades at 34 times forward earnings, which isn’t cheap at face value. But if the company can manage to continue its overseas expansion with new characters, it could bring not just cuteness overload, but profit overload too.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

Limited to 630 units, Lamborghini’s latest Urus Capsule pushes personalisation further than ever, blending hybrid performance with over 70 bespoke design combinations.

BMW has unveiled the Neue Klasse in Munich, marking its biggest investment to date and a new era of electrification, digitalisation and sustainable design.