Kobe Bryant’s Lakers Jersey Could Fetch a Record $7 Million at Sotheby’s

2 min

2 min

A Los Angeles Lakers jersey regularly worn and signed by Kobe Bryant will be auctioned next month with a high estimate of US$7 million, making it the most valuable Bryant jersey to appear on the open market.

The late basketball star wore the gold jersey on Lakers media day on Oct. 1, 2007, and throughout the NBA Western Conference finals on May 9, 2008. During the 2007-08 season, he scored 645 points in the same jersey over 25 games, according to Sotheby’s, which is handling the auction. He was named league’s most valuable player that year, his only MVP season.

This is also the only gold jersey Bryant wore during the 2008 NBA playoffs, Sotheby’s said. He wore it again for his official MVP portrait that year.

“Sports artifacts with this type of long-term, heavy wear are a rarity in the collecting space, with many modern items worn for just a single game,” Brahm Wachter, Sotheby’s head of streetwear and modern collectables, said in a news release.

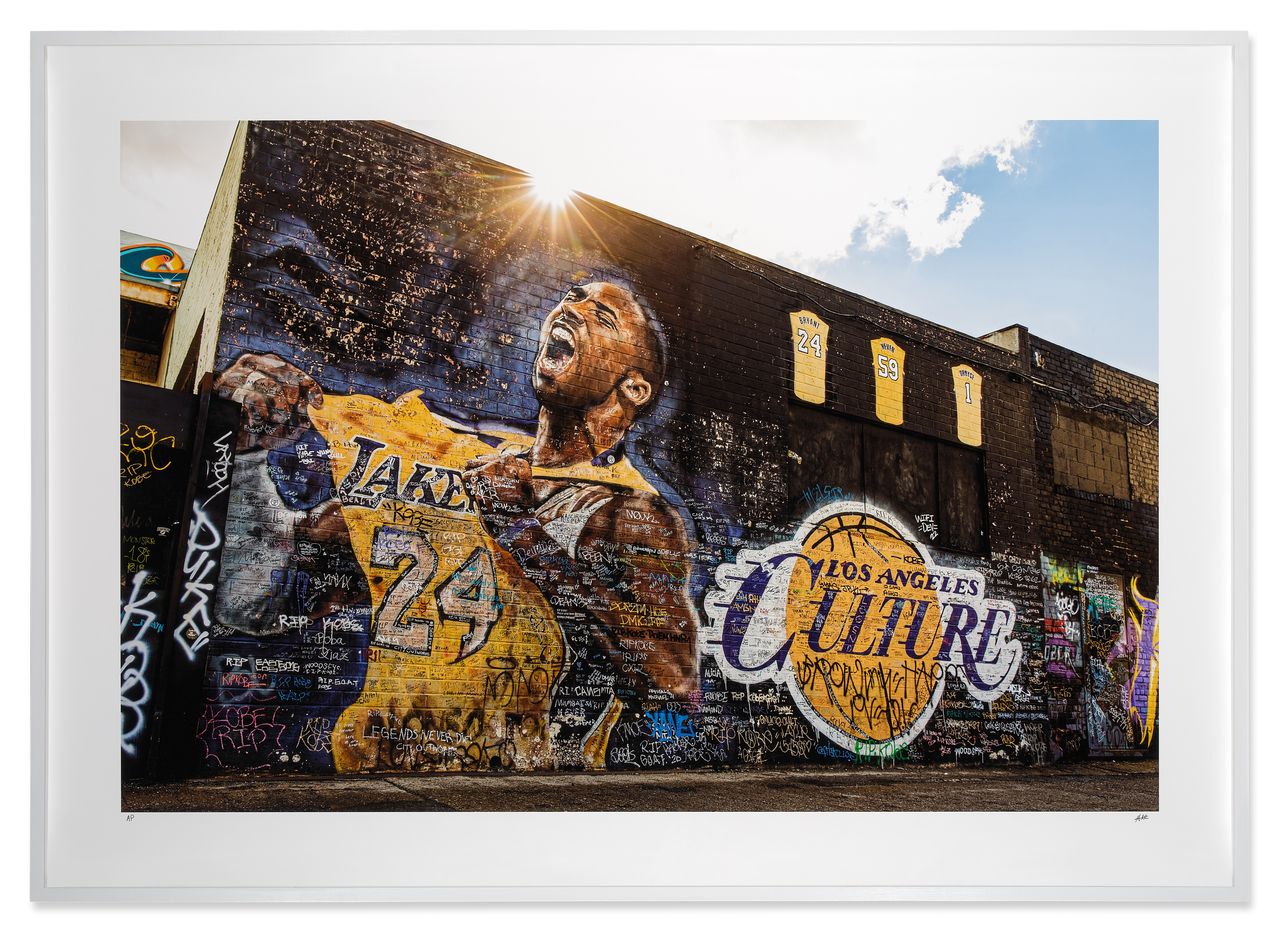

This jersey has been featured in murals and artworks depicting the basketball legend across the globe. There are more than 15 such murals in California alone, including the painting by artist Jonas Never located near the team’s arena in Los Angeles, according to Sotheby’s.

A shooting guard, Bryant spent his entire 20-year professional career with the Lakers. He appeared in 18 All-Star games, won two Finals MVP awards, and two gold medals on the 2008 and 2012 U.S. Olympic teams.

Bryant, along with his daughter Gianna and seven others, died in a helicopter crash in Calabasas, Calif., in 2020. He was 41.

The jersey will be sold at Sotheby’s online from Feb. 2-9, with bidding starting at US$5 million. It will be on public exhibition from Feb. 1-7 in Sotheby’s New York galleries.

The auction house declined to disclose the identity of the consignor. The jersey is offered with a collection of photographs of Bryant in this jersey taken by Greg Cohen, and a number of related items, including artwork, t-shirts, pins, books, and more.

The current record for any item of Kobe Bryant sports memorabilia is a game-worn and autographed jersey from his 1996-97 rookie season. It sold for US$3.7 million in 2021 at Goldin Auctions.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

Travellers are swapping traditional sightseeing for immersive experiences, with Africa emerging as a must-visit destination.

A haven for hedge-fund titans and Hollywood grandees, Greenwich is one of the world’s most expensive residential enclaves, where eye-watering prices meet unapologetic grandeur.