Best Stock-Fund Managers of 2022

In a brutal year for investing, a handful of stock pickers managed to post positive returns. The winner was up nearly 32%.

6 min

6 min

Well at least it wasn’t as dreadful as the Great Depression. Or even the financial crisis of 2008.

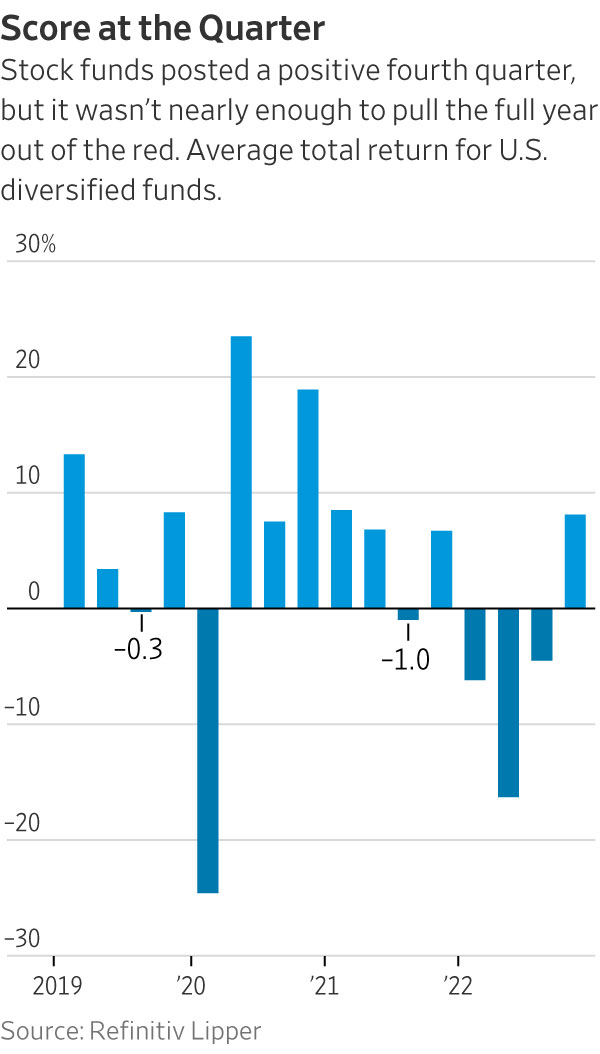

But for any mutual-fund manager trying to cope with the sea of red ink that flooded financial markets in 2022, that’s meagre consolation. In a year when soaring interest rates and sky-high inflation left the S&P 500 index with a 19% loss and triggered an even worse year for the bond market, an estimated $8.2 trillion of stock-market wealth in the U.S. simply evaporated.

Even most of those value- and income-focused mutual-fund managers who “outperformed” the broad index did so by confining their losses to the single digits—little comfort for investors.

Indeed, of the 1,410 actively managed mutual funds that met the criteria for inclusion in the Winners’ Circle, The Wall Street Journal’s quarterly survey of top-performing stock managers on a 12-month basis, a mere 40 wrapped up 2022 in positive territory. The average loss for the whole group, according to data provided by Morningstar Direct, was 18.2%.

To outperform in 2022 required a fund’s manager to have taken outsize positions in the energy sector—the only one of the 10 industries that make up the S&P 500 to record a gain in 2022. In fact, the magnitude of the rally in energy resulted in the sector coming within a whisker of doubling in its weight within that large-cap market index, hitting 5.23%.

And energy bets were what powered three Kinetics funds to top positions in the Winners’ Circle—not only the winning fund, but the runner-up and the No. 4 finisher.

“It seems as if we’re always a contrarian, but recently that has been working for us,” says James Davolos, a portfolio manager at Horizon Kinetics LLC, who serves on the investment committee for the three Kinetics funds. Between 30% and 60% of the assets of No. 1 fund Kinetics Small Cap Opportunities Fund (KSCOX), runner-up Kinetics Paradigm Fund (WWNPX) and No. 4 finisher Kinetics Market Opportunities Fund (KMKNX) were invested in energy-related holdings over the course of 2022, he says.

Kinetics Small Cap took home the crown with its 31.9% gain. The Paradigm fund gained 29.2%, and Market Opportunities gained nearly 15%.

Contest requirements

To qualify for inclusion in this Winners’ Circle survey, funds must be actively managed U.S.-stock funds with more than $50 million in assets and a record of three years or more, as well as meet a handful of other criteria. The survey excludes index and sector funds, funds that employ leverage strategies and most quantitative funds. The results are calculated by Morningstar Direct.

Important to note: These are stock funds that outperformed in specific market environments, and may have elements that make them unsuitable for some investors, ranging from their fee structure to their longer-term performance or volatility.

Mr. Davolos says he has no plans to abandon his highly concentrated and contrarian investment approach with the dawn of a new calendar year.

“The world isn’t going to quickly revert back to the way it was in 2018 or 2019,” he says. “We think we’re in the early stages of a transition to a five- or seven-year transition period. We were positioned for that in areas like energy and other hard assets that we thought would be more resilient. And we believe that most businesses will continue to face a difficult operating environment and a compression in their profit margins.”

That’s why Mr. Davolos and his team have designed the Kinetics portfolios to have hefty overweight positions in companies and industries that he believes will be able to demonstrate more-resilient profit margins. Energy royalty companies—and especially Texas Pacific Land Corp., which represented anywhere from 50.9% of assets in the Market Opportunities Fund to as much as 64.8% of the Paradigm fund’s holdings—will remain a focus, he says. Texas Pacific is one of the biggest landowners in Texas and funnels oil-and-gas royalties that it earns from those drilling on its land directly to investors.

But Mr. Davolos is also looking for opportunities to invest in other areas he believes will be equally robust in face of economic headwinds, whose stocks don’t reflect that potential.

One sector that he finds of particular interest is precious metals, and once again, he’s emphasising royalty income as a way to profit from what he sees as strong fundamentals for the sector with lower risk.

“Gold, in particular, is likely to do well in a period of draconian risk aversion and higher or rising interest rates, as people look for a store of value,” says Mr. Davolos. He also expects precious metals to respond positively to any geopolitical shocks or uncertainty, just as energy did in 2022. But he prefers to avoid exploration and production companies and the cyclicality and risk inherent in the profit cycle of these businesses, and instead looks to companies like Franco-Nevada Corp., another royalty play. “Streams of royalty income are more predictable and rewarding,” he insists.

While none of the top-performing Kinetics funds could be described as being diversified, Mr. Davolos also is keeping an eye open for opportunities to add other inflation-resistant, value-priced securities to these portfolios. For instance, noting that “government contracts are likely to be immune to inflation,” he has established and built on positions in CACI International Inc., a defence contractor that emphasises communications, cybersecurity and other technology services. He also likes Brookfield Asset Management as a way to indirectly profit from government spending on infrastructure, and has hung on to holdings in financial exchanges like CME Group Inc. and Intercontinental Exchange Inc. “Any company that provides an intermediary service—connecting two counterparties that are trying to manage their own risks—will remain critical” to the economy, he argues.

A faithful finish

Unsurprisingly, other top-performing managers in the 2022 year-end Winners’ Circle also beat the odds and triumphed by bucking conventional wisdom.

The year’s third-place finisher is one of the smallest funds in the survey. Schwartz Value Focused Fund (RCMFX) may have only $51.7 million in assets, but it turned in an impressive return for its investors, wrapping up the year with a 21.2% gain. And the fund is managed by Schwartz Investment Counsel in Plymouth, Mich., which oversees a universe of other portfolios, including Ave Maria Value Fund (AVEMX), the Catholic-values fund that ended the year with a 4.2% advance, putting it in 11th place in our survey.

Both funds are overseen by a team headed by George Schwartz, the founder, chairman and CEO of Schwartz Investment Counsel. He and son Tim, the firm’s chief investment officer, began adding energy stocks to Schwartz Value a few years ago, just as the pressure on pension funds and other mutual funds to divest their fossil-fuel holdings began to take effect.

“Our focus is on buying out-of-favour stocks when they are cheap, and when we believe they have a great recovery potential,” the elder Mr. Schwartz says. “When the energy sector had gotten so depressed it was ridiculous, we bought those stocks aggressively.” By the end of 2022, 41% of Schwartz Value’s assets were invested in an array of energy companies. “That decision has been a big boon for us,” he says.

Like Mr. Davolos, Mr. Schwartz is a fan of Texas Pacific Land, by far the fund’s single largest holding at 27.6% of fund assets. But he adopts a more, ahem, catholic (as in “all encompassing”) approach to energy investing, allocating capital to major global integrated producers and refiners like Chevron Corp., exploration-and-production companies such as Devon Energy Corp. and service companies like Schlumberger NV.

A Yeti fan

And he, too, is casting a (slightly) wider net. While hanging on to precious metals investments (Franco-Nevada and producer Barrick Gold) and what he sees as core value holdings in Berkshire Hathaway, last year Mr. Schwartz added new positions in an array of specialty manufacturing companies like A.O. Smith Corp. (water treatment and heating) and Yeti Holdings Inc. (drink coolers, drinkware and related gear). One of his largest new holdings is in RH, formerly known as Restoration Hardware, the specialty retailer of luxury furniture. “We like companies that are out of the mainstream,” he says, adding that RH shares now change hands for 15% more than the average price Schwartz Counsel paid to establish its position starting in September 2022.

Scott Barbee, manager of the No. 5 fund in the Winners’ Circle, Aegis Value Fund (AVALX), echoes his fellow outperformers in crediting the energy sector with his portfolio’s 2022 return of 10.5%.

“Back in the early stages of the pandemic, when investors were flocking to the big-name technology stocks, energy stood out like a sore thumb,” he says. Selling pressure from sustainable-investing funds and others trying to avoid fossil fuels “frightened everyone away from the sector.” But Mr. Barbee, who seeks out cyclically depressed businesses that he believes are poised for a rebound, opted to invest in the sector beginning in early 2021. “They were trading cheaply, they had long-lived asset bases, and their balance sheets are in amazing condition,” he says. The latter consideration became particularly important as interest rates began to soar last year; companies with lower debt levels remain insulated from this source of pressure.

By the end of 2022, Aegis Value had 37% of its assets invested in the fossil-fuels area, in holdings ranging from coal producer Hallador Energy Co., to International Petroleum Corp. and Akita Drilling Ltd.

“The tailwinds for this sector are likely to be with us for some time,” Mr. Barbee says. But he’s taking some of his energy holdings off the table, and redeploying that capital into other sectors. He added to the fund’s exposure to the metals mining industry (its largest position has been copper giant Amerigo Resources Ltd.) and boosted its stake in precious metals by investing in Centerra Gold Inc.—adding to a list of gold producers that already included Orezone Gold Corp. and Equinox Gold Corp. “This is another neglected corner of the market, and we believe our holdings will do well at current gold prices and phenomenally if gold goes higher” in response to inflation and interest-rate trends, he says.

None of the top-performing managers of 2022 voiced much optimism about the likelihood of seeing a broad market recovery in 2023.

“How much will be needed to bring inflation under control?” says Mr. Barbee, referring to the prospect of further interest-rate increases. “That’s why we emphasise companies with strong balance sheets, since they’re more likely to get through whatever we’ve got coming.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Millions of houses, thousands of jets, every NFL and NBA team—imagine the things a trillionaire could buy.

3 min

The initial public offering for SpaceX could make Elon Musk the world’s first trillionaire. Just how wealthy is the tech founder?

His fortune now stands at roughly $970 billion, mostly in stock, according to a Wall Street Journal analysis.

Accumulating that amount over his career averages out to $992 a second.

Musk’s wealth includes $538 billion for his pre-IPO stake in SpaceX, $167 billion for his stake in Tesla , and another $150 billion or so for stock options in those companies he could exercise just about any time, the Journal analysis found.

Then there is $5 billion apiece for The Boring Company, which drills tunnels, and Neuralink, the brain-implant firm he founded, and $104 billion in property, aircraft and other investments and assets as estimated by Altrata, a wealth-intelligence firm

He has made about $3.6 million an hour over 31 years

Musk is 54 years old and co-founded the first of his many U.S. tech- and engineering-oriented companies in 1995, 31 years ago. To amass $970 billion in that time meant accumulating roughly:

An American household earning the median U.S. income ($83,730 in 2024) would have to work more than 11 million years to make his wealth.

To be sure, the success of Tesla and SpaceX also has made billions of dollars for investors who bet on Musk and made millionaires of employees who got shares in the businesses.

Ingrid Robeyns, a philosopher and economist, has written that the wealth of the world’s richest has soared so much it is nearly incomprehensible for laypeople to grasp.

She recently estimated that Musk would make about $4.2 million an hour in his career, if he worked 70 hours a week without vacations until he is 75 years old.

Musk, of course, is known for sleeping on factory floors and rarely taking vacations. After buying Twitter, he has said, his work exploded to more than 120 hours a week from about 80 hours before.

Buy 2.4 million U.S. homes or 10,000 private jets

Most of Musk’s wealth is tied up in his companies. He famously said in 2020 that he would “own no house” and sold off several California properties, only to later buy homes in Texas.

Musk can borrow billions against his holdings in SpaceX and Tesla, but much of his wealth is on paper—not cash he can easily spend.

Here are some things a person with $970 billion could do with that amount of money:

$970 billion is bigger than the yearly output of most countries

Musk’s net worth eclipses the annual economic activity of more than 125 countries, including Norway, Thailand, Argentina and South Africa.

His self-made fortune, built on electric vehicles rocket ships and artificial-intelligence ambitions amounts to about 3% of U.S. gross domestic product today. On that basis, he easily surpasses John D. Rockefeller , the richest American who ever lived before Musk.

A century ago, Rockefeller rode the wave of industrialisation by building Standard Oil into a behemoth, wielding influence over railroads and pipelines. The monopoly was ultimately broken up by the federal government.

Rockefeller amassed a fortune of about $1.4 billion by 1937—roughly 1.5% of U.S. GDP at the time. Here is how that compares in terms of today’s economy:

This explanatory article may be periodically updated.

Sources: Altrata (Musk net worth excluding options; Bezos, Ellison and Zuckerberg net worth); Securities and Exchange Commission filings (Tesla and SpaceX stock options); Census via St. Louis Fed (2024 median U.S. annual household income, first-quarter 2026 median U.S. house sale price); Forbes (NFL and NBA team values); Liberty Jet (G700 operating costs); International Monetary Fund (2026 GDP by country); Harvard Business School case study (Rockefeller wealth) undefined Photos: Getty Images (Musk); Associated Press (Musk, Bezos, NBA, NFL); Reuters (Zuckerberg, Ellison); Bloomberg (homes, jet)

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.