Inflation takes a dip, while bananas and melons make a mash of prices

After appeals to cashed-up Australians to stop spending, there’s a little inflationary relief in sight

2 min

2 min

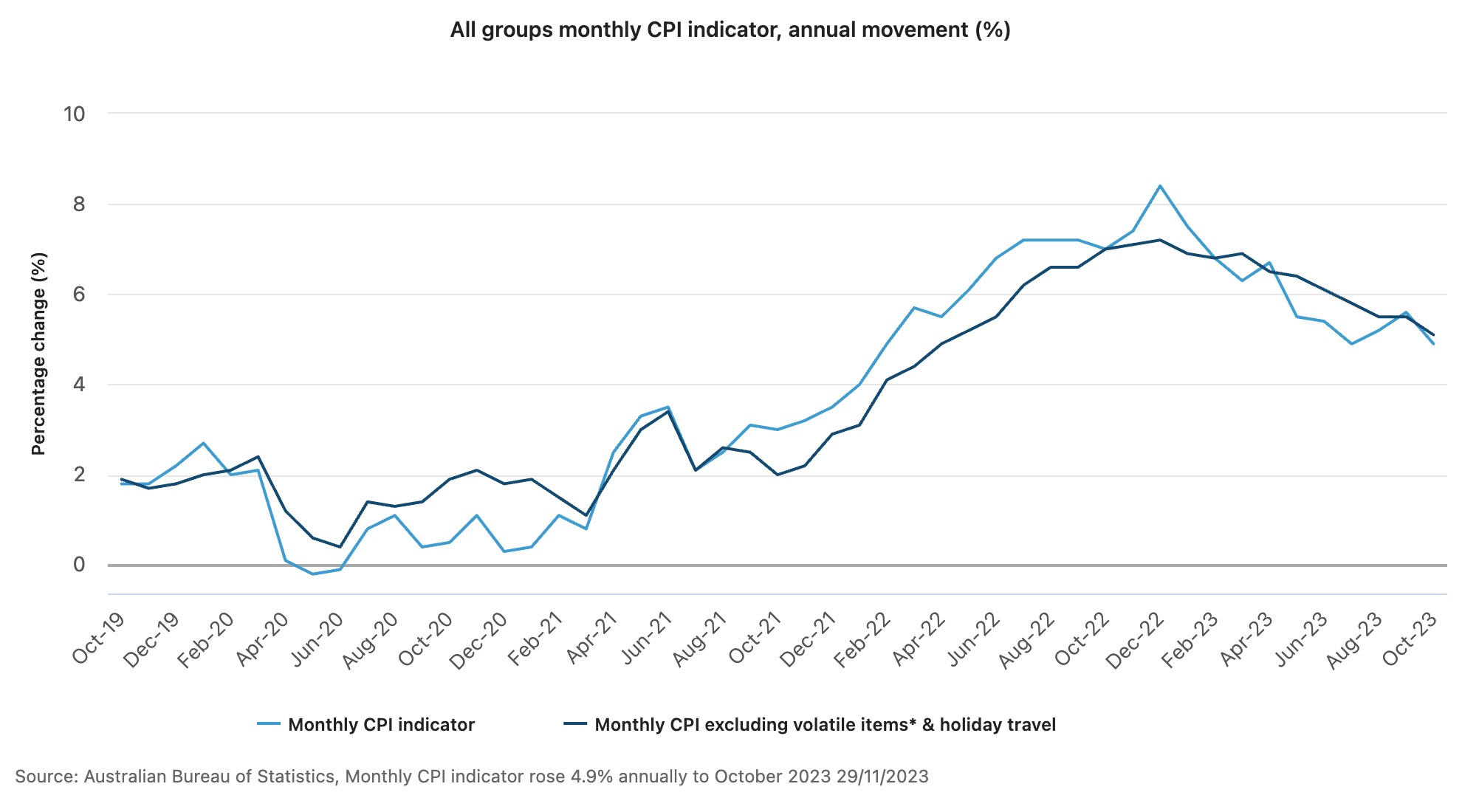

The rate of inflation in Australia has fallen to 4.9 percent, according to data from the Consumer Price Index. Inflation is down from 5.6 percent in September and a peak of 8.4 percent in December 2022.

The housing, transport and food and non-alcoholic beverages sectors were the strongest contributors to the October increase, which is consistent with trends shown in ABS data from September.

“CPI inflation is often impacted by items with volatile price changes like Automotive fuel, Fruit and vegetables, and Holiday travel,” said acting head of price statistics at the ABS, Leigh Merrington. “It can be helpful to exclude these items from the headline CPI to provide a view of underlying inflation.”

Food and non-alcoholic beverages rose from 4.7 percent in September to 5.3 percent in the 12 months to October, driven by the rising prices of melons and bananas.

In good news for would-be home builders, new dwelling prices rose 4.7 percent, the lowest annual rise since August 2021, as a result of easing material supply conditions.

While the ABS noted that electricity prices rose 10.1 percent in the year to October, Mr Merrington said it could have been worse, if not for the introduction of the Energy Bill Relief Fund.

“Electricity prices have risen 8.4 per cent since June 2023. Excluding the rebates, Electricity prices would have increased 18.8 per cent over this period,” Mr Merrington said.

The inflation figures come ahead of the final meeting for the year of the RBA Board next Tuesday. The board raised the cash rate by 25 basis points at the November meeting following an increase in the rate of inflation in September.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

From the Caribbean to Australia’s east coast, Oyster’s latest world rally promises a bluewater voyage designed for owners seeking ultimate sailing experiences.

Chinese carmaker GAC will expand its Australian electric vehicle line-up with the city-focused AION UT hatchback.