Is Germany’s Economic Model Truly Kaputt?

4 min

4 min")

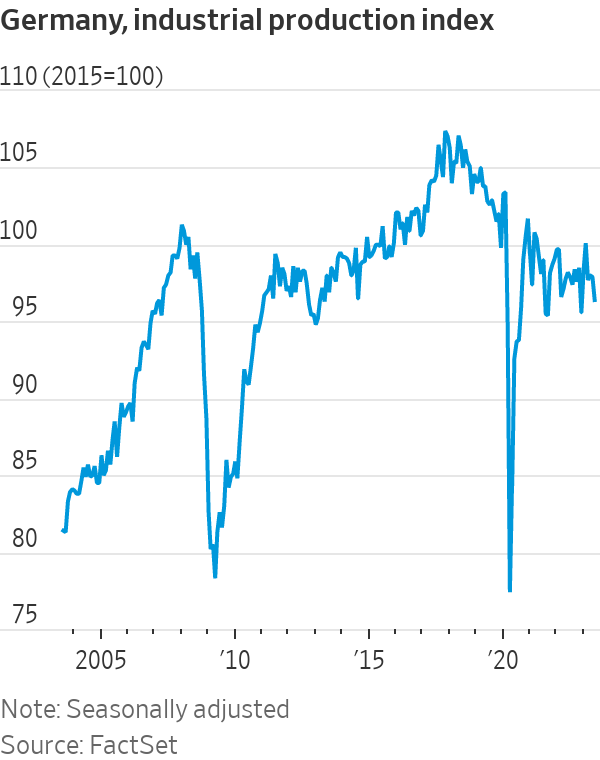

More than two decades after Germany was famously called “the sick man of the euro” by The Economist magazine, investors must wonder if the country’s industrial heart is once again critically weak. This week brought more dismal German economic data: Industrial production fell 1.5% in June from the previous month, worse than analysts expected. Though figures released on Friday showed a rise in exports, the volume of goods Germany sends abroad is still close to lows plumbed in the 2009 global financial crisis.

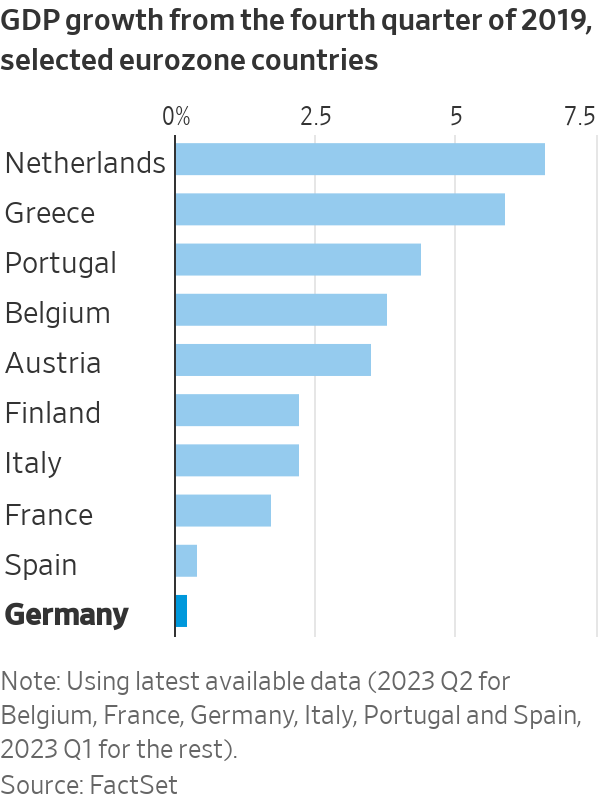

German gross domestic product has clocked three quarters of negative or zero growth , making the country the worst performer among major eurozone nations since 2019. Previously it was the top performer. How long this “slowcession” lasts is a crucial question for picking stocks in Europe. Despite the recent economic reversal, the DAX has been by far the best equity index in the eurozone over 20 years, returning almost 360%.

By comparison, investing in long-stagnant Italy yielded a paltry 140% return. German industrial output has been in decline since 2018, when global vehicle sales fell for the first time in almost a decade. A postpandemic rebalancing of spending toward services has made the situation worse. Growth in China, the fourth-largest market for German exporters, has slowed.

On Thursday, shares in Siemens —the largest industrial firm in Europe—fell 5% after it cited these two factors as the cause of a fall in orders during the second quarter. Some of the grit that has gotten into the German economic machine might be hard to dislodge . Chinese carmakers have turned from partners into fierce competitors as Volkswagen , BMW and Mercedes-Benz play catch-up in electric-vehicle technology.

It isn’t just China that is seeking to substitute imports for domestic products; the Biden administration is copying Beijing’s playbook. There is also energy. At the same time as German industry has lost Russia as its main source of cheap gas, Berlin has closed the country’s last three nuclear power plants. Angst has gripped German officials and executives in an echo of worries voiced at the start of the millennium, when unemployment surged and globalisation ravaged factories.

Back then, the response was a policy package that prioritised international competitiveness, incentivising the creation of low-pay “minijobs.” The government embraced fiscal austerity and nudged unions to push for wage restraint. The result was a 20-year decline in unemployment and a current-account surplus that reached an eye-watering 8% of GDP even as the U.S. ran huge deficits. Many economists praised German labor flexibility and fiscal austerity.

Conversely, critics pointed out that surpluses made most households worse off, and that Germany’s factory-job losses were just as large as America’s. Politics aside, it was largely a fortuitous jump in foreign demand that drove growth, allowing the nation to solidify gains in industries where it already had an advantage.

“Over the last 20 years, Germany always had an external sugar daddy: China, the eurozone and then the U.S.,” said Carsten Brzeski , chief economist at ING.

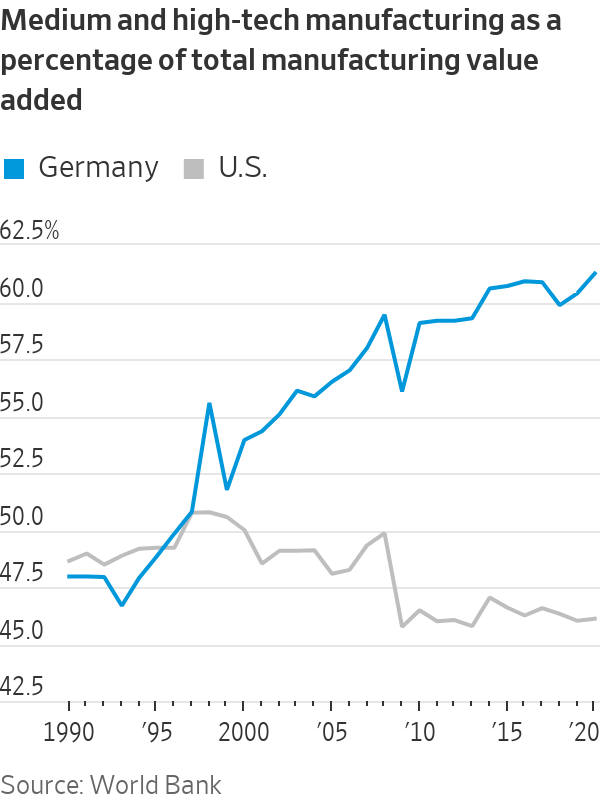

The flaw in this model was that it outsourced economic policy, leading to problematic dependencies on geopolitical rivals. It also fostered an excessive focus on old winners at the expense of new digital technologies and renewable energy. Bearish investors are right that it will take years to rectify these problems, particularly given the complexity of consensus-based German politics. Yet the German export-led model also got a lot right. As in China or South Korea, it channeled demand toward higher-productivity, higher-wage firms.

Unlike in the U.S., German manufacturing became more complex. That allowed the country’s industrial base to survive better than in other Western countries. In a world where nations are scrambling to reshore industries, Germany already has them. The readiest answer to its growth challenge isn’t to turn away from manufacturing but to double down by taking a page from Chinese and now U.S. industrial policy.

The German government is already doing this with semiconductors as part of the European Chips Act. Back in June, it signed off on 10 billion euros (around $11 billion) in subsidies for American chip maker Intel to build two plants, and earlier this week it committed €5 billion to help Taiwan’s TSMC set up a factory with local partners like Infineon.

A similar approach is needed to upgrade the country’s power generation and transmission and accelerate the transformation of carmakers and other industrial incumbents. Long-term energy guarantees could stem cost swings in the meantime. Given its political influence over the European Union, it seems hard to imagine that the bloc’s green-economy push could somehow leave Germany in a less dominant position . Historically, this is one patient that always leaves the hospital.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

Scotch whisky expert, luxury hospitality strategist and Keeper of the Quaich inductee Ross Blainey is bringing a new philosophy of luxury experiences to Citizen Kanebridge.

By improving sluggish performance or replacing a broken screen, you can make your old iPhone feel new agai