Luxury Brands Are in a Winner-Takes-All Phase

Hermès captured the lion’s share of growth in luxury-goods spending in the second quarter, while everyone else lagged behind

3 min

3 min

Louis Vuitton’s owner designed the medals for the Paris Olympic Games. It can’t be easy to see rival Hermès make off with gold in the second-quarter sales heat.

France’s three most powerful luxury-goods companies reported very mixed second-quarter results last week. On Tuesday, LVMH Moët Hennessy Louis Vuitton said sales in the three months through June rose by a disappointing 1% compared with the same period last year. Gucci owner Kering followed with an 11% fall for the quarter and issued a profit warning. Hermès left its competitors in the dust with a 13% increase in sales over the same period.

Hermès captured more than 100% of the incremental growth in the industry in the latest quarter. Luxury shoppers spent €440 million—equivalent to $477.6 million at current exchange rates—more in the French brand’s stores than they did in the same period of last year. They spent €400 million less on all other luxury brands combined, based on analysis by Bank of America.

This points to a double whammy for high-end brands, which face challenges at both ends of the consumer spectrum they serve.

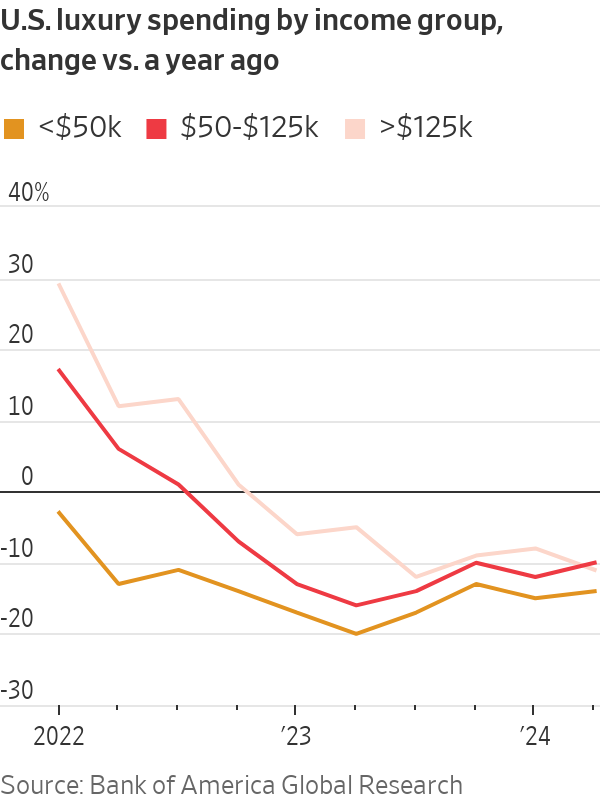

It has been clear for months that middle-class shoppers in the U.S. and China, the luxury industry’s two most important markets, have reined in their purchasing.

Chinese consumers are saving rather than spending because the value of their homes is falling. Lower-income and middle-income Americans who developed a taste for luxury during the pandemic have pulled back sharply as they have burned through excess savings.

Now, wealthy consumers, too, seem to be getting choosier about which brands they will and won’t buy. Hermès Chief Executive Axel Dumas said there is a “flight to quality” under way in the luxury industry. This shift is benefiting the Birkin handbag maker , which has a reputation for timeless designs.

Chinese buyers in particular are avoiding flashy and logo-heavy brands as worries about the country’s economy and real-estate challenges grow.

Jewellery sales are also holding up as shoppers look for goods that are more likely to hold their value than clothing or handbags. Cartier’s owner Richemont said its jewellery sales rose 4% in the quarter, although the company’s overall sales were weighed down by weak demand for its watch and fashion brands. Kering jewellery labels Boucheron and Pomellato were rare bright spots in its portfolio.

The outlook is harsh for brands such as Gucci and Burberry that are in turnaround mode. The latter issued a profit warning earlier this month and replaced its CEO in an admission that a years-long push to make the British trench-coat maker more exclusive had failed. Its shares have fallen to levels not seen since 2010.

Both brands face an uphill battle to lure shoppers. Neither Gucci nor Burberry is known for the classic designs now in vogue. The labels might also have exacerbated the slump, as the sharp price increases that luxury brands implemented in recent years have sidelined aspirational shoppers.

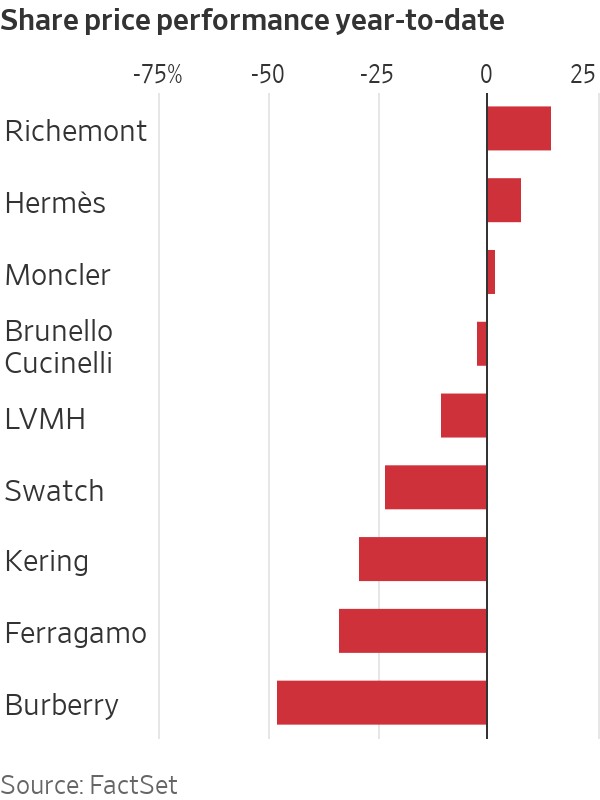

Luxury stocks are diverging. Shares in Richemont and Hermès have gained 15% and 8% respectively so far this year, with everyone else in the red.

Investors are taking their cue from wealthy shoppers: In troubled times, the most exclusive brands are the safest bet.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

The voices reshaping how Australians think about money — and why credibility matters more than reach.

6 min

The best financial advice many Australians are receiving right now is not coming from licensed advisers charging by the hour. It is coming through a phone screen, in the ten minutes between work and dinner, from creators who have built credibility the hard way: by being right, being transparent, and being specific in a space where vagueness has always been the easy default.

This is not a ranking by follower count. Follower count is a measure of distribution, not of quality. What follows is a ranking by substance — credentials, accuracy, community depth, and the quality of what an audience actually learns from following these accounts. The distinction matters, because the Australians acting on this content are making real financial decisions with real money.

1- Queenie Tan – Corporate Authorised Representative; Co-Founder & Director, Invest With Queenie & Billroo

There are finance influencers who talk about building wealth, and there are those who document it in real time with receipts. Queenie Tan belongs firmly in the second category. Starting from a $400-per-week income, Tan built her net worth past $1 million while publishing the actual numbers — income, savings rate, investment decisions — for an audience of more than 400,000 across platforms.

She is a Corporate Authorised Representative, co-founder of the personal finance app Billroo, and the author of a book that has become a practical reference for young Australians navigating ETFs, superannuation and property. What separates her from the crowded field of money educators is precision: she does not talk in principles when she can talk in percentages.

2- Alan Kohler – Editor-in-Chief, Eureka Report; Editor-in-Chief, InvestSMART Group; ABC News finance presenter, host of Inside Business.

If Queenie Tan represents the new wave of personal finance creators, Alan Kohler represents something the new wave will spend decades trying to build: institutional credibility that has survived multiple economic cycles. As Editor-in-Chief of the Eureka Report and InvestSMART Group, and a decades-long presence on ABC News, Kohler has spent more than thirty years making financial analysis accessible without dumbing it down.

His coverage of RBA decisions, market movements and economic policy is cited by podcasters, journalists and fund managers alike. He is not chasing virality. He does not need to.

3- Aleks Nikolic – Corporate lawyer; host, Big Swinging Stocks podcast

Most finance creators address the mechanics of money. Aleks Nikolic addresses the psychology — and that distinction explains why her following is as loyal as it is. Operating as Broke Girl Wealth across Instagram, TikTok and YouTube, Nikolic covers ETFs, crypto and investment strategy, but her real differentiator is a willingness to discuss the emotional architecture of financial decision-making.

Shame around debt. Fear around market volatility. The limiting beliefs that stop people acting on what they already know. In a space where confidence is routinely performed, her candour is a genuine competitive advantage.

4- Bryce Leske & Alec Renehan – Equity Mates Media

Equity Mates did not build a following. They built a media company. What began as a podcast by two friends learning to invest has grown into Australia’s most established investing media brand, covering ASX stocks, ETFs, global markets and fund manager interviews across podcast, social and YouTube.

The longevity is the credential. Equity Mates has operated through multiple market cycles, a global pandemic, and a generational shift in how Australians engage with investing — and its audience has grown through all of it. When the hosts speak, their listeners know they have been paying attention for years.

5- The Lazy CEO – CEO & Founder, Showpo; Shark Tank Australia investor

The metric that matters most on social media is not followers — it is engagement, because engagement signals trust. Jane Lu, known as The Lazy CEO, maintains an engagement rate of approximately 1.15 per cent on Instagram, which is exceptional for a finance account of his size. Her 242,000-plus followers are not passive consumers: they ask questions, share experiences and apply what they read.

Her content focuses on business finance and wealth building, and the active comment sections are the clearest possible evidence that her audience does not merely scroll past.

6- Tash Invests – Founder, Tash Lends; Forbes Australia 30 Under 30

Tash Invests built her following on a premise that sounds simple but is rarer in practice than it should be: she publishes the actual numbers. Not approximations or ranges or anonymised case studies — her salary, her savings rate, her portfolio value, her net worth, updated and on the record.

Having bought her first property at twenty-two and grown her documented net worth past $1 million, she has become the primary reference point for young Australians trying to understand what building wealth on a moderate income genuinely looks like. The specificity is the product.

7- David Scutt – APAC Market Analyst at StoneX Group

The authority of most finance social media content rests on research and reading. David Scutt‘s authority rests on having done the job. A former Treasury Dealer at Arab Bank and the Commonwealth Bank, former ASX Business Supervisor, and former Global Markets Editor at Business Insider Australia and anchor at ausbiz TV, Scutt now brings that direct market experience to his role as APAC Market Analyst at StoneX Group, rather than relying on secondary commentary.

When he discusses foreign exchange movements or ASX dynamics, it is not because he has read about them. It is because he has traded them.

8- Meddy Demars – Investing & crypto content creator

The gap Meddy Demars fills is specific and underserviced: connecting global macroeconomic events to the practical reality of Australian investors. When the US Federal Reserve adjusts interest rates, when inflation data moves, when commodity prices shift — most Australian finance content either ignores the local implications or translates them poorly.

Demars, operating across TikTok and Instagram from Sydney, does the translation well: explaining what global conditions mean for Australian stocks, savings rates and investment portfolios in terms that are accessible without being condescending.

9- Simran Kaur – Founder, Friends That Invest

Friends That Invest is arguably the most successful community-building exercise in Australian personal finance, and Simran Kaur is the reason why. The New Zealand-based creator — whose audience is predominantly Australian — built a podcast, a book and a social media presence around a single insight: that the personal finance world was not speaking to young women, and that the consequences of that gap were significant.

The measurable cultural shift that followed — women engaging with investing concepts in communities that had not previously existed — is the kind of impact that most financial literacy programmes aim for and rarely achieve.

10- Effie Zahos – Money Editor at 9News

Effie Zahos is one of Australia’s most recognised financial commentators, appearing regularly across 9News, A Current Affair, Today and Today Extra as 9News Money Editor. Her role puts everyday money questions, from mortgage rates to cost-of-living pressures, in front of a national broadcast audience.

Before television, she spent years as editor of Money magazine, building the editorial foundation for her current commentary. She is also Director and Money Commentator at InvestSMART, an ambassador for Canstar, and a published author, with her financial advice available in print as well as on screen.

That combination, decades of editorial experience, an active broadcast presence, and a body of published work, is what makes her commentary carry weight beyond any single platform or post.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

Hand-built in Melbourne and limited to just 10 cars a year, the Zeigler/Bailey Z/B 4.4 is reshaping what a modern collector car can be.