DOUBLE-DIGIT HOUSE PRICE GROWTH ARRIVES AHEAD OF EXPECTATIONS

Australia’s housing market defies forecasts as prices surge past pandemic-era benchmarks.

2 min

2 min

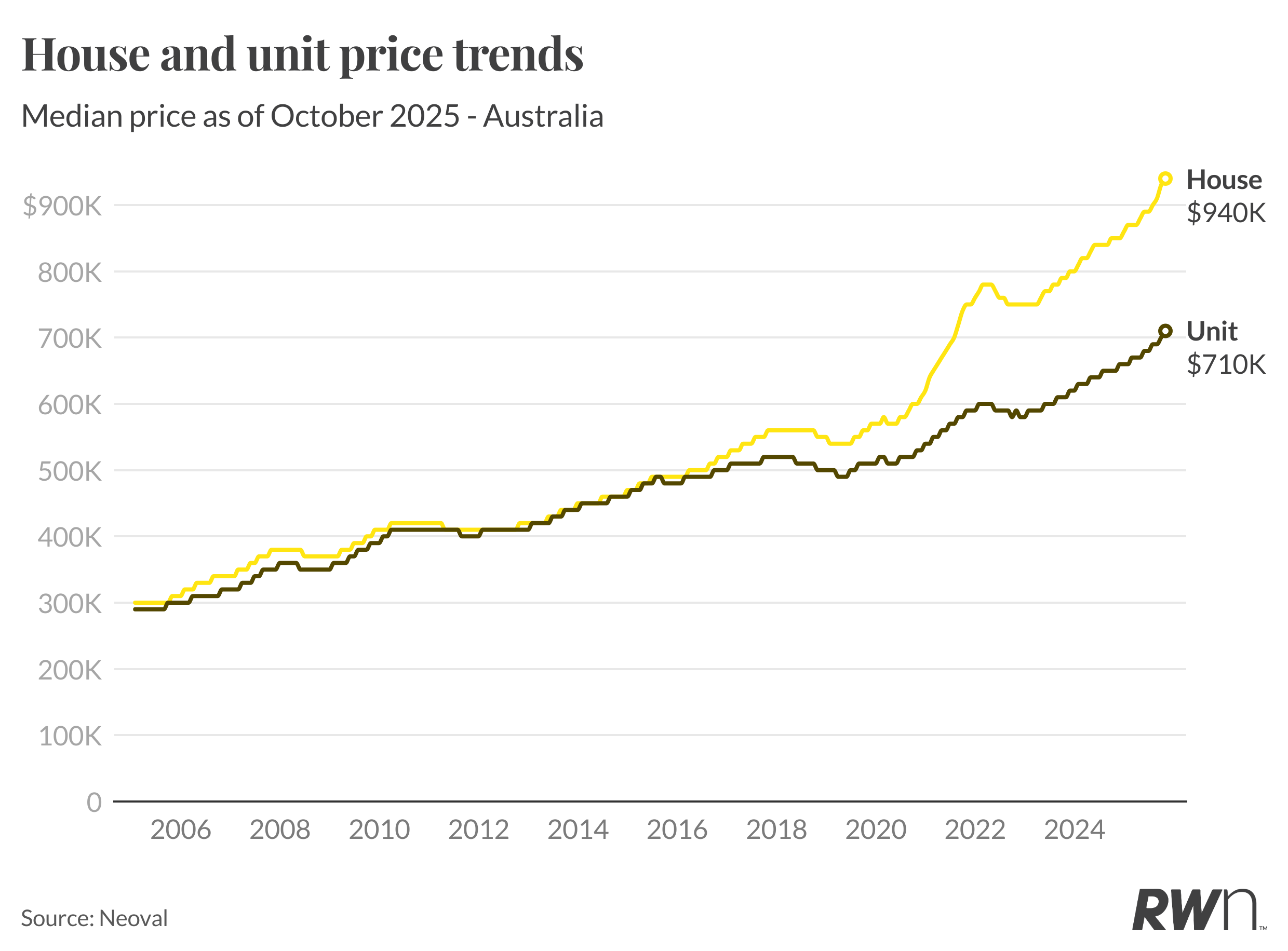

Australian house prices are surging again, delivering double-digit annual growth months ahead of schedule.

Nationally, the median house price climbed 1.1 per cent in October to $940,000, lifting annual growth to 10.6 per cent, the first double-digit increase since the 2021–22 property boom.

Market Resilience Surprises Analysts

The acceleration comes earlier than expected, according to Ray White Group Chief Economist Nerida Conisbee, who says the milestone was originally forecast for the end of the year.

“Stronger-than-expected October gains and continued tight supply across most markets have pushed growth ahead of schedule,” Conisbee said. “This shows how resilient demand has remained through spring.”

Perth (+14.8 per cent), Brisbane (+12.5 per cent) and Adelaide (+10.8 per cent) continue to lead the charge among capital cities, while Sydney (+8.6 per cent) and Melbourne (+6.5 per cent) show steady, consistent increases.

Regional Markets Extend Their Lead

Beyond the capitals, regional Australia is powering ahead, particularly in the resource states.

Regional Western Australia jumped 16.4 per cent year-on-year, and regional Queensland followed close behind at 14.5 per cent, as population growth and affordability continue to drive demand.

Units Outperform Houses

Unit prices rose even more sharply in October, up 1.4 per cent to $710,000, marking 9.2 per cent annual growth. Conisbee said affordability pressures, new first home buyer incentives, and a lack of available stock are pushing more buyers into the apartment market.

“Units are now seeing stronger monthly gains than houses, reflecting both affordability constraints and renewed first-home-buyer activity,” she said.

The biggest monthly jumps were in Perth (+1.6 per cent), Adelaide (+1.5 per cent), and Brisbane (+1.4 per cent). Melbourne’s unit market also firmed, up 1.6 per cent, as buyers returned to lower price brackets.

Spring Demand Defies Higher Listings

Despite an influx of spring listings, new stock has failed to match the intensity of buyer demand. Nationally, house prices have now risen every month since February, and unit prices every month since March.

“The pace of growth shows demand hasn’t been dampened by higher supply,” Conisbee said.

Outlook: Steady Growth Into 2026

The data comes as the Reserve Bank prepares for its Melbourne Cup Day meeting, where rates are expected to remain on hold at 3.6 per cent.

With inflation easing only gradually and unemployment sitting around 4.5 per cent, analysts expect monetary policy to stay steady for now.

Ray White’s forecast suggests 2025 will close with high single- to low double-digit annual growth nationally, with smaller capitals and regional areas tipped to outperform well into 2026.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

3 min

Ophora Tallawong has launched its final release of apartments, positioning itself as one of the last opportunities for buyers to secure a new Sydney home below $700,000.

The project, located in one of the city’s fastest-growing corridors, is offering rare buyer protections at a time when affordability is tightening and competition for quality stock is intensifying.

According to JLL’s Q2 2025 Apartment Market Overview, Sydney’s median apartment price has already climbed to $795,000, setting a record.

With interest rates now on a downward trend and supply still heavily constrained, experts warn that today’s price brackets may not exist next year.

Ronnie Rahme, Development Manager at KDMC, said buyers were responding to the combination of quality and value.

“You simply don’t see this level of finish at these price points anymore,” Rahme said. “That’s why demand has been so strong for this final release.”

Dr Andrew Wilson, Chief Economist at My Housing Market, says the economic drivers are clear. “High rents and higher prices continue to provide clear incentives for first-home buyers and investors chasing solid investment returns,” he told Kanebridge News.

“New government initiatives to support first-home buyers will also act to place upward pressure on prices.”

The bigger picture

JLL’s research reinforces that point. While over 15,700 apartments are expected to be delivered nationally this year, a 40% uplift on 2024, Sydney remains undersupplied, with demand continuing to outpace completions.

The report also notes that reductions in the RBA cash rate are expected to further fuel buyer activity, with constrained supply continuing to push prices higher into 2026.

With construction costs soaring, Government contributions climbing, and interest rates remaining high, projects are harder than ever to bring to market, putting upward pressure on newly completed apartments.

The pipeline of new supply is shrinking as developers delay or abandon projects that no longer stack up financially.

According to JLL’s overview, only 2,554 completions are forecast for Sydney this year – against annual demand exceeding 30,000 dwellings.

At the same time, population growth, rental demand, and first-home buyer incentives are intensifying competition for limited stock. The imbalance between constrained supply and resilient demand is leaving new apartments scarcer and more expensive across Sydney.

Ophora: Last Chance In Sydney’s northwest

Developed by KDMC and designed by Architex, the $50 million project has launched its final release, with limited availability of 81 brand-new residences from just $545,000 for a one-bedroom, or $695,000 for a two-bedroom, which is far below Sydney’s median and significantly cheaper than nearby competition.

The five-storey development at 37 Reis St, Tallawong, combines affordability with premium inclusions more often seen in luxury builds: ducted air-conditioning, timber floors, premium finishes, fridge cavities with water plumbing, video intercom systems, fibre internet, EV charging, landscaped gardens and a rooftop terrace with sweeping views.

It also comes with something almost unheard of at this price point, a 10-year Latent Defects Insurance (LDI) policy. Typically reserved for multimillion-dollar projects, LDI guarantees structural integrity for a decade and is only awarded to developers with a strong building track record.

SHC Insurance Brokers founder Stefan Hicks acknowledged the rarity of obtaining LDI, particularly for entry-level residential apartment complexes like Ophora.

“Gaining LDI is no mean feat. It’s offered selectively to developers and builders with a quality building history, and it requires both parties to employ an independent inspection service throughout construction,” he said.

“While this insurance is well-established around the world in about 40 countries, in Australia, we’re typically seeing high-end buildings covet LDI. The fact that Ophora has joined this exclusive list of quality-assured builds is a coup for entry-level home buyers.”

Raising the standard for affordable luxury

Rahme says the KDMC team wanted to set a new benchmark.

“Our mission with Ophora has always been clear: to raise the standard of what buyers should expect, regardless of budget,” he said.

“We’ve delivered a collection of apartments with finishes and features you’d usually only find in luxury projects, and we’ve backed it with one of the most stringent insurances available in the market. That gives buyers peace of mind that their investment is protected for the long term.

“People are walking through and realising you simply don’t see this level of quality at these price points anymore, as it’s effectively replacement cost in 2025.

“With rates coming down and limited competition, buyers and investors are moving quickly because they know the window won’t stay open. Investors, who have recently purchased at Ophora, have reported a strong rental demand, with minimum rental yields exceeding five per cent.”

Developments like Ophora, move-in ready, competitively priced and backed by rare structural protections (LDI), may represent the last chance for buyers to secure a sub-$700,000 apartment in Sydney.

View Ophora on cpmrealty.com.au

To arrange a private viewing or request more information, contact Sam Elbanna from CPM Realty: 0411 222 260

Australia’s market is on the move again, and not always where you’d expect. We’ve found the surprise suburbs where prices are climbing fastest.

By improving sluggish performance or replacing a broken screen, you can make your old iPhone feel new agai