A More Profitable Tesla Is Still a Pricey Ride

Surprise lift in automotive margins reverses damage from Robotaxi fallout, but valuation is now far above even AI stars

3 min

3 min")

Elon Musk thinks of Tesla as an AI company. He’d be seriously bummed if it were valued like one.

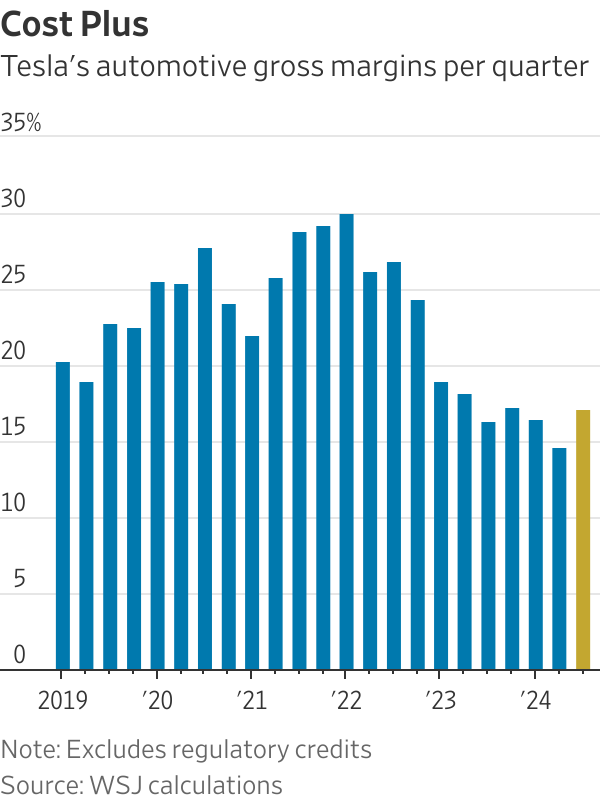

Tesla’s third-quarter results gave the EV maker’s stock price a strong boost on Thursday, recovering the ground lost following the company’s disappointing Robotaxi event earlier this month. The reaction wasn’t entirely unwarranted: Tesla managed to surprise Wall Street by reversing the steady decline its automotive gross margins have suffered over the past two years. Strong growth in sales and gross profits in the company’s energy generation and storage segment also helped. Tesla’s total operating profit came in at $2.7 billion for the quarter—37% above Wall Street’s consensus forecast, according to FactSet.

Still, Tesla’s overall growth is far below normal, or at least what has long been the company’s version of normal. Total automotive revenue rising 2% year over year in the third quarter comes after two consecutive quarters of declines. That is also a fraction of the 45% growth Tesla’s core business averaged on a quarterly basis from 2020 through 2023. The world’s largest EV maker can’t escape the gravity of a global auto-sales slowdown .

And even the profit boost might not be built to last. “Sustaining these margins in Q4, however, will be challenging, given the current economic environment,” said Tesla Chief Financial Officer Vaibhav Taneja on the company’s conference call on Wednesday.

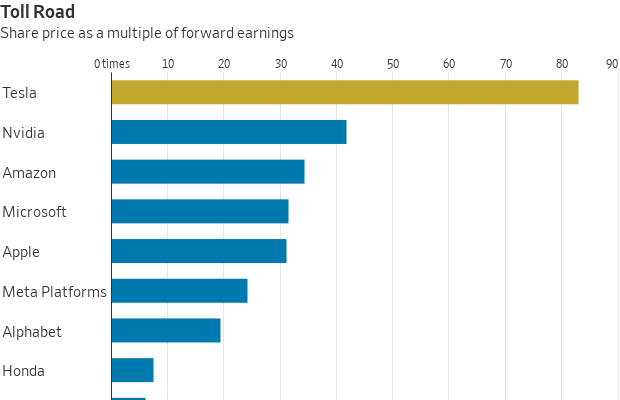

Analysts boosted their profit targets anyway. The consensus projection for Tesla’s per-share earnings over the next four quarters rose more than 5% following the company’s report. But even that doesn’t cover Tesla’s chunky valuation; Thursday’s jump of nearly 22% puts the stock price at around 83 times forward earnings. That is more than twice the multiple that megacap tech giants such as Apple , Microsoft and Amazon .com fetch. If Tesla were valued on par with Nvidia , whose chips Tesla is snapping up to power its ambitions in AI, autonomous driving and robotics, the stock price—and a good chunk of Musk’s net worth—would be be half its current level.

Hence, Tesla needs much, much more to go right than just a recovery in the global EV market. But its biggest ambitions are distant and by no means slam dunks. Musk reiterated his plan to have Robotaxis begin production in 2026 . The ultimate fate of that business, though, lies in the company’s ability to clear the necessary regulatory hurdles for self-driving cars in states like California—not to mention catching up to rivals such as Waymo that are already on the road.

“While compute capacity growth is a positive indicator that will support accelerated learning cycles, we remain cautious on Tesla’s system performance vs. peers given lack of driver-out regulatory approvals and limited detail on miles between engagement,” wrote Colin Rusch of Oppenheimer on Thursday.

The humanoid robot called Optimus is even more of a long shot—not that Musk qualifies it as such. “So I think it has a good chance of being the most valuable product ever made,” Musk said on Wednesday’s call.

Even some of Tesla’s near-term targets look ambitious. After scrapping its Model 2 project earlier this year, the company reiterated a plan to launch a “more affordable” car in the first half of next year, though details on that vehicle remain sparse. And Musk projected vehicle-sales growth of 20% to 30% next year—a sharp jump from the 13% pace analysts were projecting, according to FactSet.

“We struggle to handicap the unit growth, given the uncertain timing of volume production, a limited sense of how different the offerings will be relative to the current Model 3 and Y, and true delivered price,” wrote Toni Sacconaghi of Bernstein.

Tesla has to get an awful lot of rubber to meet the road.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

From Italy’s $93,000-a-night villas to a $20,000 Bowral château, a new global ranking showcases the priciest Airbnbs available in 2026.

International AI strategist Justin Kabbani will headline the Kanebridge Property Summit in Sydney on June 18, with tickets selling fast.