The U.S. and IMF Disagree About China. That’s a Problem.

The IMF doesn’t share U.S. view that China’s massive trade surpluses are hurting the world, and that tension is likely to grow

4 min

4 min

Eighty years ago world leaders meeting in Bretton Woods, N.H., created the International Monetary Fund to prevent the sorts of economic imbalances that had brought on the Great Depression.

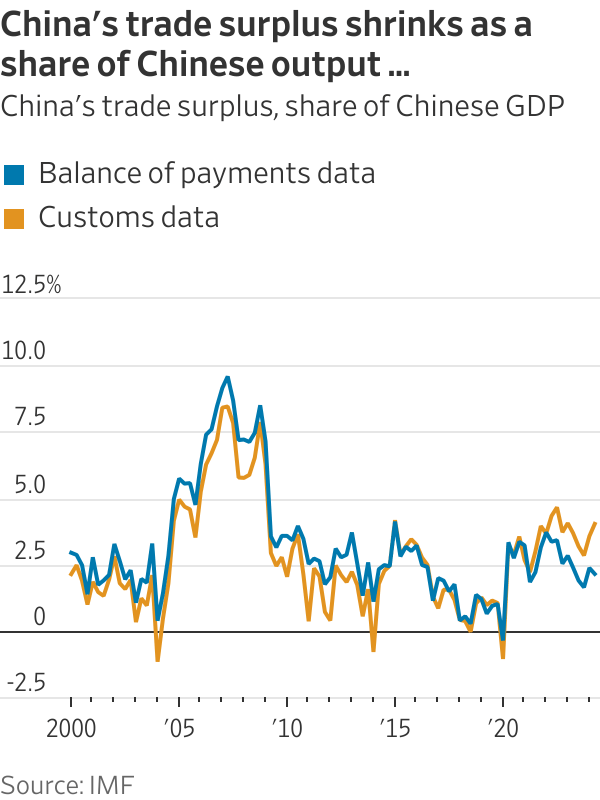

Today, imbalances once again threaten global harmony. China’s massive trade surplus is fuelling a backlash. The U.S. attributes those surpluses to China holding down consumption while subsidising manufacturing and exports, inflicting collateral damage on its trading partners. And it would like the IMF to say so.

The IMF, though, has steered a more neutral path. It has prodded Beijing to change its economic model while playing down any harm from that model for the world.

Decades ago, U.S. leaders thought bringing China into the postwar economic institutions such as the IMF and World Trade Organization would make Beijing more market-oriented and the world more stable. They now think the opposite. China has doubled down on an authoritarian, state-driven economic model that many in the West see as incompatible with their own.

The IMF, the world’s most influential international economic institution, may find itself torn between irreconcilable visions of the global economy, especially if former President Donald Trump is re-elected next month.

Trump has prioritised reducing the trade deficit, especially with China, through tariffs, an approach the IMF has criticised. Many of his advisers are deeply suspicious of both Beijing and international institutions. Project 2025, an agenda for a second Trump term that includes many Trump advisers as authors, has suggested the U.S. should leave the IMF, though there is no sign Trump agrees.

The U.S. has been upset about the growth in China’s trade surplus since it joined the World Trade Organization in 2001, wiping out U.S. factory jobs in what became known as the China shock .

China’s surpluses have since shrunk as a share of its gross domestic product. But because China’s economy is now so large, that surplus has grown as share of world GDP, to 0.7%. Other countries are alarmed at a growing flood of cheap manufacturing imports, dubbed “China Shock 2.0 .”

Jake Sullivan , President Biden’s national security adviser, said at the Brookings Institution Wednesday that China “is producing far more than domestic demand, dumping excess onto global markets at artificially low prices, driving manufacturers around the world out of business, and creating a chokehold on supply chains.”

Treasury Undersecretary Jay Shambaugh told me at a panel organised by the Atlantic Council two weeks ago that China is “already 30% of global manufacturing. You can’t grow at a massive rate when you start from 30% of the world without displacing not just us, but lots of countries.”

Pointing out such tensions is part of the IMF’s job, Shambaugh said at the event. While the IMF has said China’s industrial policies may be hurting its trading partners, “I would like to see them pay more attention…to the aggregate external imbalance.”

The IMF’s architects believed a breakdown in economic cooperation contributed to the Depression. Countries such as the U.S. that ran large trade surpluses felt no pressure to help those with deficits, like Britain. Depressed countries sought to limit imports and boost exports by devaluing their currencies or imposing tariffs, in effect seeking to export their unemployment.

To end such “beggar-thy-neighbour” policies, British economist John Maynard Keynes proposed that trade be conducted through a global bank and currency that would prevent big deficits and surpluses. Instead, at Bretton Woods, delegates agreed to peg their currencies to the dollar with the IMF overseeing periodic revaluations.

By the 1970s, inflation and growing trade deficits caused fixed exchange rates to collapse. Cross-border capital flows soared, enabling poor countries to borrow from western banks and investors. When they defaulted, the IMF had a new mission: helping them restructure their debts, usually on the condition of strict budget austerity. IMF, a popular joke ran, stood for “It’s Mostly Fiscal.”

Even today, while the IMF does still monitor trade deficits and surpluses, it rarely attributes those to cross-border influences, focusing instead on fiscal and other domestic factors.

In a blog post last month, IMF staff investigated the U.S. deficit and Chinese surplus and found little connection.

The U.S. deficit reflected strong government and household spending, while China’s surplus resulted from slumping property markets and domestic confidence. They “are mostly homegrown,” they wrote. In an implicit rebuke to the U.S., they wrote, “Worries that China’s external surpluses result from industrial policies reflect an incomplete view.”

This benign view of Chinese surpluses has drawn criticism. Brad Setser , a former U.S. Treasury official now at the Council on Foreign Relations, said the IMF has relied on data that understates the surplus.

Setser also raps the IMF’s advice to Beijing to let interest rates and the exchange rate fall while tightening fiscal policy—that is, raising taxes or cutting spending. That, he said, will weaken imports, boost exports and thus widen the trade surplus.

“Their analysis is all about how bad the fiscal situation is, with no real analysis of the balance of payments position,” Setser said.

Pierre-Olivier Gourinchas , the IMF’s chief economist, disagreed. He noted the IMF has consistently urged China to boost household consumption such as by strengthening the social safety net and shifting more of the tax burden from the high-consuming poor to the high-saving rich. He also noted that the IMF has argued for fiscal stimulus now and consolidation later.

Does the IMF’s opinion make a difference? Most countries—the big ones especially—will never need to borrow from the IMF and can thus ignore its advice. The IMF has long urged the U.S. to rein in its budget deficit, noting this contributes to its trade deficit, and the U.S. has just as long ignored it.

And yet when the IMF speaks, it does so with an authority and credibility that no private analyst or individual country commands.

China’s approach to boosting exports is “killing jobs elsewhere, and that’s something the IMF should call out,” said Martin Mühleisen , a former senior IMF official now at The Atlantic Council. “China doesn’t want bad publicity from the IMF, in part because the criticism would resonate in many countries.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A long-standing cultural cruise and a new expedition-style offering will soon operate side by side in French Polynesia.

The pandemic-fuelled love affair with casual footwear is fading, with Bank of America warning the downturn shows no sign of easing.

The pandemic-fuelled love affair with casual footwear is fading, with Bank of America warning the downturn shows no sign of easing.

2 minThe boom in casual footware ushered in by the pandemic has ended, a potential problem for companies such as Adidas that benefited from the shift to less formal clothing, Bank of America says.

The casual footwear business has been on the ropes since mid-2023 as people began returning to office.

Analyst Thierry Cota wrote that while most downcycles have lasted one to two years over the past two decades or so, the current one is different.

It “shows no sign of abating” and there is “no turning point in sight,” he said.

Adidas and Nike alone account for almost 60% of revenue in the casual footwear industry, Cota estimated, so the sector’s slower growth could be especially painful for them as opposed to brands that have a stronger performance-shoe segment. Adidas may just have it worse than Nike.

Cota downgraded Adidas stock to Underperform from Buy on Tuesday and slashed his target for the stock price to €160 (about $187) from €213. He doesn’t have a rating for Nike stock.

Shares of Adidas listed on the German stock exchange fell 4.5% Tuesday to €162.25. Nike stock was down 1.2%.

Adidas didn’t immediately respond to a request for comment.

Cota sees trouble for Adidas both in the short and long term.

Adidas’ lifestyle segment, which includes the Gazelles and Sambas brands, has been one of the company’s fastest-growing business, but there are signs growth is waning.

Lifestyle sales increased at a 10% annual pace in Adidas’ third quarter, down from 13% in the second quarter.

The analyst now predicts Adidas’ organic sales will grow by a 5% annual rate starting in 2027, down from his prior forecast of 7.5%.

The slower revenue growth will likewise weigh on profitability, Cota said, predicting that margins on earnings before interest and taxes will decline back toward the company’s long-term average after several quarters of outperforming. That could result in a cut to earnings per share.

Adidas stock had a rough 2025. Shares shed 33% in the past 12 months, weighed down by investor concerns over how tariffs, slowing demand, and increased competition would affect revenue growth.

Nike stock fell 9% throughout the period, reflecting both the company’s struggles with demand and optimism over a turnaround plan CEO Elliott Hill rolled out in late 2024.

Investors’ confidence has faded following Nike’s December earnings report, which suggested that a sustained recovery is still several quarters away. Just how many remains anyone’s guess.

But if Adidas’ challenges continue, as Cota believes they will, it could open up some space for Nike to claw back any market share it lost to its rival.

Investors should keep in mind, however, that the field has grown increasingly crowded in the past five years. Upstarts such as On Holding and Hoka also present a formidable challenge to the sector’s legacy brands.

Shares of On and Deckers Outdoor , Hoka’s parent company, fell 11% and 48%, respectively, in 2025, but analysts are upbeat about both companies’ fundamentals as the new year begins.

The battle of the sneakers is just getting started.

The pandemic-fuelled love affair with casual footwear is fading, with Bank of America warning the downturn shows no sign of easing.

From the shacks of yesterday to the sculptural sanctuaries of today, Australia’s coastal architecture has matured into a global benchmark for design.