There’s a China-Shaped Hole in the Global Economy

China’s low-consuming, high-investing economy guarantees conflict with other countries

4 min

4 min

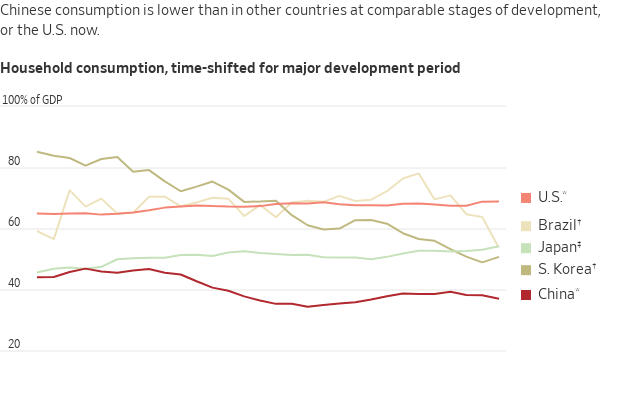

China’s economy is unusual. Whereas consumers contribute 50% to 75% of gross domestic product in other major economies, in China they account for 40%. Investment, such as in property, infrastructure and factories, and exports provide most of the rest.

Lately, that low consumption has become a headwind to China’s growth because property investment, once a major component of demand, has collapsed.

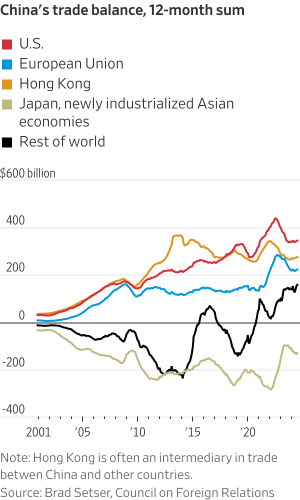

This isn’t just a problem for China; it’s a problem for the whole world. What Chinese companies can’t sell to Chinese consumers, they export. The result: an annual trade surplus in goods now of almost $900 billion, or 0.8% of global gross domestic product. That surplus effectively requires other countries to run trade deficits.

China’s surplus, long a sore spot in the U.S., increasingly is one elsewhere, too. While China’s 12-month trade balance with the U.S. has risen by $49 billion since 2019, it’s up $72 billion with the European Union, $74 billion with Japan and Asia’s newly industrialised economies, and about $240 billion with the rest of the world, according to data compiled by Brad Setser of the Council on Foreign Relations.

Logan Wright , head of China research at Rhodium Group, a U.S. research firm, said China accounts for just 13% of the world’s consumption but 28% of its investment. That investment only makes sense if China takes market share away from other countries, rendering their own manufacturing investment unviable, he said.

“China’s growth model is dependent at this point on a more confrontational approach with the rest of the world,” he said.

While many developing countries relied on investment and exports to fuel early growth, China is an outlier for how low its consumption is, and its sheer size. In a report, Rhodium estimates that if China’s consumption share equaled that of the European Union or Japan, its annual household spending would be $9 trillion instead of $6.7 trillion. That $2.3 trillion difference—roughly the GDP of Italy—is equal to a 2% hole in global demand.

The sources of this underconsumption are deeply embedded in both China’s fiscal systems and its policy choices.

Chinese incomes are highly unequal, and because the rich spend less of their income than the poor, this automatically depresses consumption. Rhodium cites data that says the top 10% of households had 69% of total savings, while a third had negative saving rates.

Other countries address such disparities by taxing the rich more heavily and boosting the spending power of lower and middle classes through cash transfers, and public health and education. China does much less of this. Just 8% of its tax revenue comes from personal income taxes, compared with 38% from value-added taxes, similar to sales taxes, which fall much more heavily on lower-income families, Rhodium estimates.

China also spends less on health and education than major market economies, forcing poor and middle-income families to spend more of their disposable income on both.

Meanwhile, suppressed wages and interest rates depress household income and spending while boosting the profits of state-owned enterprises. The limited taxing authority of local governments forces them to raise revenue by selling property for manufacturing and infrastructure, which further inflates investment.

A decade ago top Chinese policymakers shared Western economists’ perspective that, at the macro level, China needed to rebalance away from investment to consumption. In 2013, the ruling Communist Party said growth would henceforth rely on market forces and consumers.

President Xi Jinping ended up going in the opposite direction; consumption stayed weak while state control over the economy grew. He has replaced reformers with loyalists more preoccupied with sector-specific targets than overall growth.

The bedrock principle behind trade is comparative advantage: countries specialise in what they do best and then export it in exchange for imports. Xi rejects this principle. In pursuit of “independence and self-reliance,” he wants China to make as much and import as little as possible.

Officials in China boast that it is the “only country to produce in every single one of the United Nations’ industrial product categories,” notes Andrew Batson of Gavekal Dragonomics.

Even as China targets advanced products such as electric vehicles and semiconductors, it refuses to surrender market share in lower-value products: “Establish the new before breaking the old,” Xi has instructed his bureaucrats , my colleagues have reported.

As a result, Rhodium argues , “China provides fewer opportunities as an export market for emerging countries while competing head-on with them in the low-tech and mid-tech space.”

Countries that once saw China as a customer now see a competitor. “Many Chinese businesses are manufacturing intermediate goods, which we mainly export,” Rhee Chang-yong , the governor of the Bank of Korea, said last year. “The decadelong support from the Chinese economic boom has disappeared.”

Mexican Finance Minister Rogelio Ramírez de la O complained last month , “China sells to us but doesn’t buy from us and that’s not reciprocal trade.”

Ironically, foreign officials have tended to see the U.S. as the biggest threat to the world trade system, ever since President Donald Trump in 2018 imposed steep tariffs on China and narrower tariffs on other trading partners. He has promised to expand those tariffs if elected this fall.

And yet Trump’s tariffs should be seen as a reaction to China’s beggar-thy-neighbour economic model, one that has proved impervious to existing trade rules.

Still, no single country can fix the problem. Like a dike deflecting floodwaters, U.S. tariffs have diverted Chinese exports to other markets.

Those other countries are now taking action. Mexico, Chile, Indonesia and Turkey have all announced or said they are considering tariffs on China this year. This week Canada announced steep new tariffs on Chinese electric vehicles, steel and aluminum, aligning with those already announced by the U.S.

Yet the world thus far lacks a unified solution to Chinese underconsumption, because China refuses to accept that it’s a problem.

Xi has rejected fiscal support for households as “welfarism” that breeds laziness. In April, Treasury Secretary Janet Yellen complained that China’s “weak household consumption and business overinvestment” were threatening jobs in the U.S. The state news agency Xinhua called it a pretext for protectionism. Earlier this month the International Monetary Fund advised Beijing to spend 5.5% of GDP over four years buying up uncompleted homes. Beijing politely declined.

With China dug in, more friction is sure to follow, and an already fragile world trading system will be stressed to its breaking point.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

The voices reshaping how Australians think about money — and why credibility matters more than reach.

6 min

The best financial advice many Australians are receiving right now is not coming from licensed advisers charging by the hour. It is coming through a phone screen, in the ten minutes between work and dinner, from creators who have built credibility the hard way: by being right, being transparent, and being specific in a space where vagueness has always been the easy default.

This is not a ranking by follower count. Follower count is a measure of distribution, not of quality. What follows is a ranking by substance — credentials, accuracy, community depth, and the quality of what an audience actually learns from following these accounts. The distinction matters, because the Australians acting on this content are making real financial decisions with real money.

1- Queenie Tan – Corporate Authorised Representative; Co-Founder & Director, Invest With Queenie & Billroo

There are finance influencers who talk about building wealth, and there are those who document it in real time with receipts. Queenie Tan belongs firmly in the second category. Starting from a $400-per-week income, Tan built her net worth past $1 million while publishing the actual numbers — income, savings rate, investment decisions — for an audience of more than 400,000 across platforms.

She is a Corporate Authorised Representative, co-founder of the personal finance app Billroo, and the author of a book that has become a practical reference for young Australians navigating ETFs, superannuation and property. What separates her from the crowded field of money educators is precision: she does not talk in principles when she can talk in percentages.

2- Alan Kohler – Editor-in-Chief, Eureka Report; Editor-in-Chief, InvestSMART Group; ABC News finance presenter, host of Inside Business.

If Queenie Tan represents the new wave of personal finance creators, Alan Kohler represents something the new wave will spend decades trying to build: institutional credibility that has survived multiple economic cycles. As Editor-in-Chief of the Eureka Report and InvestSMART Group, and a decades-long presence on ABC News, Kohler has spent more than thirty years making financial analysis accessible without dumbing it down.

His coverage of RBA decisions, market movements and economic policy is cited by podcasters, journalists and fund managers alike. He is not chasing virality. He does not need to.

3- Aleks Nikolic – Corporate lawyer; host, Big Swinging Stocks podcast

Most finance creators address the mechanics of money. Aleks Nikolic addresses the psychology — and that distinction explains why her following is as loyal as it is. Operating as Broke Girl Wealth across Instagram, TikTok and YouTube, Nikolic covers ETFs, crypto and investment strategy, but her real differentiator is a willingness to discuss the emotional architecture of financial decision-making.

Shame around debt. Fear around market volatility. The limiting beliefs that stop people acting on what they already know. In a space where confidence is routinely performed, her candour is a genuine competitive advantage.

4- Bryce Leske & Alec Renehan – Equity Mates Media

Equity Mates did not build a following. They built a media company. What began as a podcast by two friends learning to invest has grown into Australia’s most established investing media brand, covering ASX stocks, ETFs, global markets and fund manager interviews across podcast, social and YouTube.

The longevity is the credential. Equity Mates has operated through multiple market cycles, a global pandemic, and a generational shift in how Australians engage with investing — and its audience has grown through all of it. When the hosts speak, their listeners know they have been paying attention for years.

5- The Lazy CEO – CEO & Founder, Showpo; Shark Tank Australia investor

The metric that matters most on social media is not followers — it is engagement, because engagement signals trust. Jane Lu, known as The Lazy CEO, maintains an engagement rate of approximately 1.15 per cent on Instagram, which is exceptional for a finance account of his size. Her 242,000-plus followers are not passive consumers: they ask questions, share experiences and apply what they read.

Her content focuses on business finance and wealth building, and the active comment sections are the clearest possible evidence that her audience does not merely scroll past.

6- Tash Invests – Founder, Tash Lends; Forbes Australia 30 Under 30

Tash Invests built her following on a premise that sounds simple but is rarer in practice than it should be: she publishes the actual numbers. Not approximations or ranges or anonymised case studies — her salary, her savings rate, her portfolio value, her net worth, updated and on the record.

Having bought her first property at twenty-two and grown her documented net worth past $1 million, she has become the primary reference point for young Australians trying to understand what building wealth on a moderate income genuinely looks like. The specificity is the product.

7- David Scutt – APAC Market Analyst at StoneX Group

The authority of most finance social media content rests on research and reading. David Scutt‘s authority rests on having done the job. A former Treasury Dealer at Arab Bank and the Commonwealth Bank, former ASX Business Supervisor, and former Global Markets Editor at Business Insider Australia and anchor at ausbiz TV, Scutt now brings that direct market experience to his role as APAC Market Analyst at StoneX Group, rather than relying on secondary commentary.

When he discusses foreign exchange movements or ASX dynamics, it is not because he has read about them. It is because he has traded them.

8- Meddy Demars – Investing & crypto content creator

The gap Meddy Demars fills is specific and underserviced: connecting global macroeconomic events to the practical reality of Australian investors. When the US Federal Reserve adjusts interest rates, when inflation data moves, when commodity prices shift — most Australian finance content either ignores the local implications or translates them poorly.

Demars, operating across TikTok and Instagram from Sydney, does the translation well: explaining what global conditions mean for Australian stocks, savings rates and investment portfolios in terms that are accessible without being condescending.

9- Simran Kaur – Founder, Friends That Invest

Friends That Invest is arguably the most successful community-building exercise in Australian personal finance, and Simran Kaur is the reason why. The New Zealand-based creator — whose audience is predominantly Australian — built a podcast, a book and a social media presence around a single insight: that the personal finance world was not speaking to young women, and that the consequences of that gap were significant.

The measurable cultural shift that followed — women engaging with investing concepts in communities that had not previously existed — is the kind of impact that most financial literacy programmes aim for and rarely achieve.

10- Effie Zahos – Money Editor at 9News

Effie Zahos is one of Australia’s most recognised financial commentators, appearing regularly across 9News, A Current Affair, Today and Today Extra as 9News Money Editor. Her role puts everyday money questions, from mortgage rates to cost-of-living pressures, in front of a national broadcast audience.

Before television, she spent years as editor of Money magazine, building the editorial foundation for her current commentary. She is also Director and Money Commentator at InvestSMART, an ambassador for Canstar, and a published author, with her financial advice available in print as well as on screen.

That combination, decades of editorial experience, an active broadcast presence, and a body of published work, is what makes her commentary carry weight beyond any single platform or post.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

A cluster of century-old warehouses beneath the Harbour Bridge has been transformed into a modern workplace hub, now home to more than 100 businesses.