A surge in for-sale listings tipped to dampen home price growth

The forecast slowdown comes on the back of sharp increases in home values

3 min

3 min")

The number of new for-sale listings has been stubbornly sluggish for much of the year, but there are growing signs would-be vendors are finally feeling confident to go to market.

New analysis indicates this surge in supply is likely to put the brakes on a renewed boom in property prices being seen across much of the country.

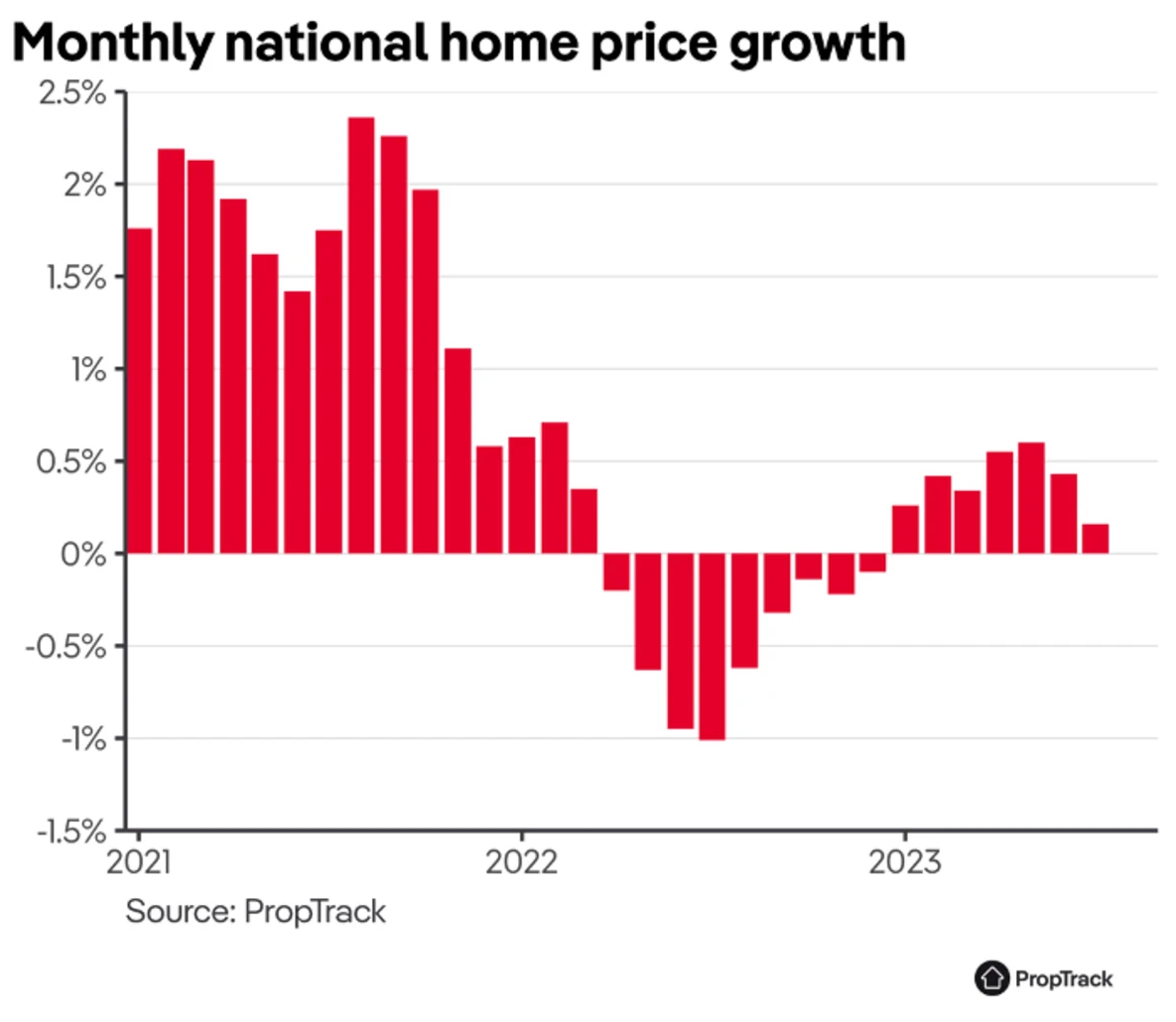

According to data from research firm CoreLogic, national home values rose 2.9 percent in the three months to July – the highest quarterly movement since January.

Across the capital cities, values were up 0.8 percent last month – down slightly from a 1.2 percent lift seen in June.

Prices are rising fastest in Sydney, with a whopping 4.5 percent jump in the three months to July.

Prices rose 4.2 percent in Brisbane in the quarter, while Adelaide and Perth each recorded a 3.2 per cent increase. Values in Melbourne were up two per cent.

“Home values are down 3.4 percent annually, but declines are quickly subsiding from an eight per cent drop in the year to March,” Eliza Owen, head of residential research at CoreLogic, observed.

Data shows the number of new listings nationally hit 33,616 in the four weeks to 30 July, trending slightly higher through the month, which she noted is unusual for this time of year.

“The flow of new listings added to the market has been rising since mid-June, in contrast to the usual seasonal trend where new vendor activity would be trending lower through the colder months.”

With more homes hitting the market ahead of the traditionally busy spring selling season, Paul Ryan, economist at data house PropTrack, said price growth could dampen in the months ahead.

“There have been some tentative signs that sellers are responding to continued strong buyer demand and higher prices by bringing more listings to market,” Mr Ryan said.

PropTrack modelling shows a low level of new listings could be responsible for as much as a quarter of the price growth seen this year, and the impact of low supply can be felt within a few months.

“This analysis suggests that a stronger flow of listings could weigh on home price growth later this year as the market gears up for the spring selling season,” Mr Ryan said.

“And importantly, it shows the impact on prices is likely to be felt quite quickly after any new listings are brought to market – within one to two months.”

Mr Ryan said property markets have “displayed a remarkable turnaround in 2023”.

“Home prices fell persistently over 2022, down 4.1 percent from April to December, during the sharpest episode of interest rate increases ever implemented by the Reserve Bank,” he said.

“But 2023 has seen national home prices increase each month, up 2.8 percent so far this year, despite continued increases in interest rates.”

One major factor for the rapid turnaround in price movements is the low supply of new listings hitting the market, he said. Buyer demand has remained strong.

“The flow of new listings over the first half of 2023 was around 15 percent below the level seen over the same period in 2022, which represents a significant decrease.

“By contrast, the total number of homes on the market has mostly drifted upward as homes take longer to sell compared to the strong market conditions in 2021.”

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

3 min

Ophora Tallawong has launched its final release of apartments, positioning itself as one of the last opportunities for buyers to secure a new Sydney home below $700,000.

The project, located in one of the city’s fastest-growing corridors, is offering rare buyer protections at a time when affordability is tightening and competition for quality stock is intensifying.

According to JLL’s Q2 2025 Apartment Market Overview, Sydney’s median apartment price has already climbed to $795,000, setting a record.

With interest rates now on a downward trend and supply still heavily constrained, experts warn that today’s price brackets may not exist next year.

Ronnie Rahme, Development Manager at KDMC, said buyers were responding to the combination of quality and value.

“You simply don’t see this level of finish at these price points anymore,” Rahme said. “That’s why demand has been so strong for this final release.”

Dr Andrew Wilson, Chief Economist at My Housing Market, says the economic drivers are clear. “High rents and higher prices continue to provide clear incentives for first-home buyers and investors chasing solid investment returns,” he told Kanebridge News.

“New government initiatives to support first-home buyers will also act to place upward pressure on prices.”

The bigger picture

JLL’s research reinforces that point. While over 15,700 apartments are expected to be delivered nationally this year, a 40% uplift on 2024, Sydney remains undersupplied, with demand continuing to outpace completions.

The report also notes that reductions in the RBA cash rate are expected to further fuel buyer activity, with constrained supply continuing to push prices higher into 2026.

With construction costs soaring, Government contributions climbing, and interest rates remaining high, projects are harder than ever to bring to market, putting upward pressure on newly completed apartments.

The pipeline of new supply is shrinking as developers delay or abandon projects that no longer stack up financially.

According to JLL’s overview, only 2,554 completions are forecast for Sydney this year – against annual demand exceeding 30,000 dwellings.

At the same time, population growth, rental demand, and first-home buyer incentives are intensifying competition for limited stock. The imbalance between constrained supply and resilient demand is leaving new apartments scarcer and more expensive across Sydney.

Ophora: Last Chance In Sydney’s northwest

Developed by KDMC and designed by Architex, the $50 million project has launched its final release, with limited availability of 81 brand-new residences from just $545,000 for a one-bedroom, or $695,000 for a two-bedroom, which is far below Sydney’s median and significantly cheaper than nearby competition.

The five-storey development at 37 Reis St, Tallawong, combines affordability with premium inclusions more often seen in luxury builds: ducted air-conditioning, timber floors, premium finishes, fridge cavities with water plumbing, video intercom systems, fibre internet, EV charging, landscaped gardens and a rooftop terrace with sweeping views.

It also comes with something almost unheard of at this price point, a 10-year Latent Defects Insurance (LDI) policy. Typically reserved for multimillion-dollar projects, LDI guarantees structural integrity for a decade and is only awarded to developers with a strong building track record.

SHC Insurance Brokers founder Stefan Hicks acknowledged the rarity of obtaining LDI, particularly for entry-level residential apartment complexes like Ophora.

“Gaining LDI is no mean feat. It’s offered selectively to developers and builders with a quality building history, and it requires both parties to employ an independent inspection service throughout construction,” he said.

“While this insurance is well-established around the world in about 40 countries, in Australia, we’re typically seeing high-end buildings covet LDI. The fact that Ophora has joined this exclusive list of quality-assured builds is a coup for entry-level home buyers.”

Raising the standard for affordable luxury

Rahme says the KDMC team wanted to set a new benchmark.

“Our mission with Ophora has always been clear: to raise the standard of what buyers should expect, regardless of budget,” he said.

“We’ve delivered a collection of apartments with finishes and features you’d usually only find in luxury projects, and we’ve backed it with one of the most stringent insurances available in the market. That gives buyers peace of mind that their investment is protected for the long term.

“People are walking through and realising you simply don’t see this level of quality at these price points anymore, as it’s effectively replacement cost in 2025.

“With rates coming down and limited competition, buyers and investors are moving quickly because they know the window won’t stay open. Investors, who have recently purchased at Ophora, have reported a strong rental demand, with minimum rental yields exceeding five per cent.”

Developments like Ophora, move-in ready, competitively priced and backed by rare structural protections (LDI), may represent the last chance for buyers to secure a sub-$700,000 apartment in Sydney.

View Ophora on cpmrealty.com.au

To arrange a private viewing or request more information, contact Sam Elbanna from CPM Realty: 0411 222 260

From citrus oils to warming spices, the classic G&T is being reimagined at home as a more thoughtful, seasonal ritual for modern entertaining.

Records keep falling in 2025 as harbourfront, beachfront and blue-chip estates crowd the top of the market.