China’s Growth Slows to Three-Decade Low Excluding Pandemic

A festering property-market meltdown offsets much of the benefit of economy’s post pandemic recovery

6 min

6 min

HONG KONG—China’s economic growth rate finished at one of the lowest levels in decades last year, underscoring the heavy toll that a property-sector collapse and weak consumer confidence have taken on the world’s second-largest economy despite the lifting of all Covid-19 restrictions.

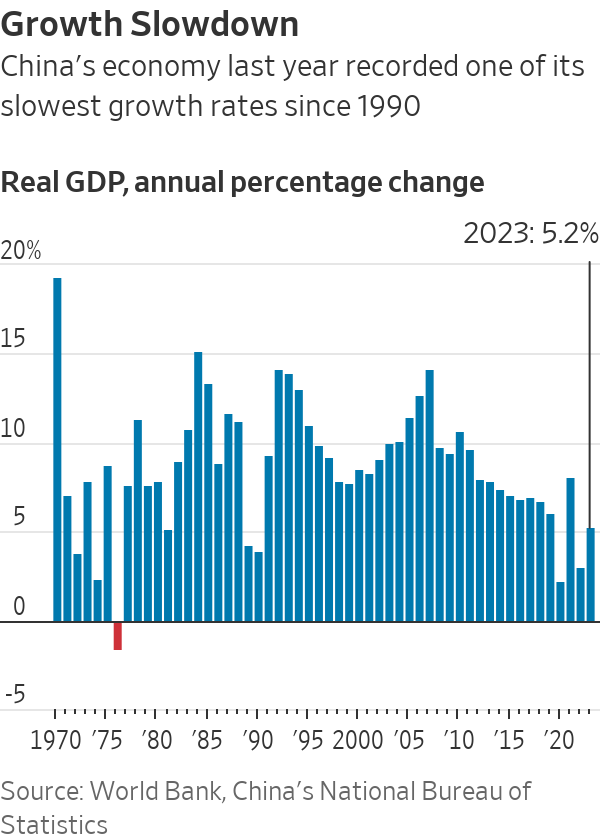

Gross domestic product in China expanded 5.2% in the fourth quarter and for the full year in 2023, according to data released by the National Bureau of Statistics on Wednesday. The reading confirmed a number uttered by Premier Li Qiang a day earlier at the World Economic Forum in Davos, Switzerland—an unusual disclosure of a high-profile data point by a senior leader before its formal release.

Apart from the three years that China was closed to the outside world during the pandemic, the country’s economy expanded in 2023 at the slowest annual rate since 1990, the year after the political turmoil of the student movement that was crushed around Beijing’s Tiananmen Square in June 1989.

In 2022, China’s economy grew 3%, while 2020—the initial year of Covid-19—saw growth of just 2.2%. This year’s outcome was flattered in part by comparison with the relatively low base of 2022, when harsh pandemic lockdowns swept the nation, crimping growth.

Last year’s 5.2% growth rate managed to top the government’s official target of around 5% growth, following a year of volatility and shifting expectations.

Maintaining growth at a similar pace this year may prove harder, given policymakers’ hesitance so far to launch any big-ticket stimulus packages. Forecasts for China’s growth rate this year among several global investment banks range from 4% to 4.9%. China is expected to announce any formal growth target at an annual legislative session set to take place in March.

In the near term, China has few obvious growth drivers. Export demand is softening as the global economy is projected to slow this year. Chinese families, hit by years of pandemic restrictions and receiving no direct financial support from the government, have turned cautious on spending amid a weak job market. Private businesses have been holding off on new investments while foreign investors are pulling funds out of the country.

The Chinese leadership’s determination to cultivate new engines of growth, in fields such as electric vehicles and renewable energy, is bearing fruit. Still, in the near term, it won’t likely be enough to make up for the shortfalls in job creation and overall growth rate from the rapid decline in its once-mighty real-estate sector.

In the longer run, China faces a daunting list of headwinds, including a population that is rapidly skewing older, high debt levels and a worsening external political environment that has seen relations with the U.S.-led West plummet.

Wednesday’s data release offered fresh signs of the dire state of the country’s demographics. Official statisticians said China’s population shrank by 2.08 million people last year, falling to 1.410 billion, after declining in 2022 for the first time in decades.

Economists are concerned that China may be falling into a vicious cycle in which falling prices and weak demand reinforce one another, as they did in Japan in the 1990s. Chinese policymakers’ reluctance to stimulate more forcefully has confounded many economists, though others have pointed to leader Xi Jinping’s ideologically-rooted reluctance to shower the economy with government money.

Instead, Chinese authorities have unleashed a barrage of smaller-bore measures, such as trimming key interest rates, cutting mortgage costs for home buyers and prodding banks to lend more to distressed property developers. Collectively, though, those measures have done little to reverse downward pressure on the economy. The government said in the fall that it would issue $137 billion in government debt, the biggest stimulus measure it has undertaken so far—though still not enough to reverse the downward momentum, economists say.

“I wonder if they are not realising how big the risk is if deflation pressure becomes entrenched,” says Alicia García-Herrero, chief Asia economist at investment bank Natixis.

Chinese stocks fell after the data was released. The CSI 300 index was down 1.4%, putting it on course to close at its lowest level in almost five years. Hong Kong’s Hang Seng Index, which includes the shares of many Chinese companies, was around 3.7% lower.

The country’s stock market is now in a multi-year slump, with foreign portfolio managers fleeing and individual investors in the country switching to safer assets. The poor state of the economy is a constant concern.

The past year had started off with a sense of buoyant optimism, as the abandonment of three years of stifling Covid-related restrictions spurred a revival of spending by consumers.

But the reopening momentum quickly lost steam after the first quarter, as global demand for Chinese-made exports—a key pillar of China’s economy throughout the pandemic years—began to wane. Persistent high youth unemployment and weak wage growth further weighed on average households’ fragile confidence.

In the fall, factory activity weakened again and consumer prices dropped into deflationary territory.

Throughout it all, a years long decline in Chinese home prices showed no sign of abating, further depriving revenue for debt-laden developers and eroding homeowners’ wealth and sense of financial security.

Looking ahead, economists have called on leaders in Beijing to step in forcefully to stabilise home prices and contain the risk of widening defaults among property developers.

“The key thing to watch in 2024 is if and when the central government would step in and take the main responsibility to stop the contagion,” said Larry Hu, chief China economist at Macquarie Group.

Whether Beijing can revive consumer confidence will be another key metric to watch this year.

In the central Chinese city of Wuhan, Bella Liu, a 32-year-old employee of a telecommunications firm, remembered 2023 as a year marked by plunging profits and frequent layoffs in her industry. After suffering a nearly 20% loss from her mutual fund investments, she is now parking more of her money in time deposits at her bank.

“In an era of slowing economic growth, I just feel lucky that I have a job,” Liu said.

Full-year economic data released by China on Wednesday showed retail sales, a key gauge of consumer spending, gained 7.4% in December and rose 7.2% for the full year compared with the respective year-earlier periods. Retail sales had fallen 0.2% for the full year in 2022.

The new data suggest that the economy is again beginning to rely more on domestic demand after counting on exports as the main pillar of growth during the pandemic years. Consumption was the largest contributor to overall growth in 2023. Still, it is unclear how much of a role it will play in driving the Chinese economy this year, in part because the release of pent-up pandemic demand has largely run its course, according to economists from Nomura.

Investment was also lacklustre in 2023. Fixed-asset investment growth slowed last year, rising 3.0% for the full year compared with a 5.1% expansion in 2022. Private-sector investment, too, remained weak, falling 0.4% in 2023 compared with a year earlier as policy uncertainty spooked entrepreneurs. Private-sector investment had risen 0.9% in 2022.

Over the course of 2023, Beijing rolled out measures aimed at reining in the technology sector, including the video game industry, while warning about foreign espionage and detaining employees of foreign firms operating in China.

Readings of the property sector offered more reason for caution. New home prices in China’s 70 major cities dropped at a faster clip toward the end of 2023.

Average new home prices in December fell 0.45% from November, and 0.89% when from a year earlier, according to calculations by The Wall Street Journal based on data released by the statistics bureau. The pace of both declines was worse than in November.

For the full year, property investment fell 9.6%, while new construction starts dropped 20.4% and home sales by value declined 6.0%.

The surveyed urban unemployment edged up to 5.1% in December, from 5% in November. Economists have cast doubt on the accuracy of official statistics on joblessness in large part because the survey leaves out the country’s nearly 300 million migrant workers.

In a surprise move, China released a revised youth unemployment figure for the first time since July, when it abruptly suspended the publication of the data series amid a run of fresh record-high readings up to 21.3%.

On Wednesday, China’s statistics bureau said that it would publish a new urban youth unemployment figure each month for people age 16 to 24 that excludes students. The reading was 14.9% in December.

The statistics bureau said that the new methodology offers a more refined and comprehensive picture that would “better reflect the employment situation” by only including graduates who were looking for work.

Still, the economy had pockets of strength, especially in dominating the global supply chain for renewable energy products such as solar panels and electric vehicles. Growth in industrial production rebounded to 4.6%, accelerating from a 3.6% increase the year before, Wednesday’s data show.

—Grace Zhu and Xiao Xiao in Beijing contributed to this article.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

3 min

Ophora Tallawong has launched its final release of apartments, positioning itself as one of the last opportunities for buyers to secure a new Sydney home below $700,000.

The project, located in one of the city’s fastest-growing corridors, is offering rare buyer protections at a time when affordability is tightening and competition for quality stock is intensifying.

According to JLL’s Q2 2025 Apartment Market Overview, Sydney’s median apartment price has already climbed to $795,000, setting a record.

With interest rates now on a downward trend and supply still heavily constrained, experts warn that today’s price brackets may not exist next year.

Ronnie Rahme, Development Manager at KDMC, said buyers were responding to the combination of quality and value.

“You simply don’t see this level of finish at these price points anymore,” Rahme said. “That’s why demand has been so strong for this final release.”

Dr Andrew Wilson, Chief Economist at My Housing Market, says the economic drivers are clear. “High rents and higher prices continue to provide clear incentives for first-home buyers and investors chasing solid investment returns,” he told Kanebridge News.

“New government initiatives to support first-home buyers will also act to place upward pressure on prices.”

The bigger picture

JLL’s research reinforces that point. While over 15,700 apartments are expected to be delivered nationally this year, a 40% uplift on 2024, Sydney remains undersupplied, with demand continuing to outpace completions.

The report also notes that reductions in the RBA cash rate are expected to further fuel buyer activity, with constrained supply continuing to push prices higher into 2026.

With construction costs soaring, Government contributions climbing, and interest rates remaining high, projects are harder than ever to bring to market, putting upward pressure on newly completed apartments.

The pipeline of new supply is shrinking as developers delay or abandon projects that no longer stack up financially.

According to JLL’s overview, only 2,554 completions are forecast for Sydney this year – against annual demand exceeding 30,000 dwellings.

At the same time, population growth, rental demand, and first-home buyer incentives are intensifying competition for limited stock. The imbalance between constrained supply and resilient demand is leaving new apartments scarcer and more expensive across Sydney.

Ophora: Last Chance In Sydney’s northwest

Developed by KDMC and designed by Architex, the $50 million project has launched its final release, with limited availability of 81 brand-new residences from just $545,000 for a one-bedroom, or $695,000 for a two-bedroom, which is far below Sydney’s median and significantly cheaper than nearby competition.

The five-storey development at 37 Reis St, Tallawong, combines affordability with premium inclusions more often seen in luxury builds: ducted air-conditioning, timber floors, premium finishes, fridge cavities with water plumbing, video intercom systems, fibre internet, EV charging, landscaped gardens and a rooftop terrace with sweeping views.

It also comes with something almost unheard of at this price point, a 10-year Latent Defects Insurance (LDI) policy. Typically reserved for multimillion-dollar projects, LDI guarantees structural integrity for a decade and is only awarded to developers with a strong building track record.

SHC Insurance Brokers founder Stefan Hicks acknowledged the rarity of obtaining LDI, particularly for entry-level residential apartment complexes like Ophora.

“Gaining LDI is no mean feat. It’s offered selectively to developers and builders with a quality building history, and it requires both parties to employ an independent inspection service throughout construction,” he said.

“While this insurance is well-established around the world in about 40 countries, in Australia, we’re typically seeing high-end buildings covet LDI. The fact that Ophora has joined this exclusive list of quality-assured builds is a coup for entry-level home buyers.”

Raising the standard for affordable luxury

Rahme says the KDMC team wanted to set a new benchmark.

“Our mission with Ophora has always been clear: to raise the standard of what buyers should expect, regardless of budget,” he said.

“We’ve delivered a collection of apartments with finishes and features you’d usually only find in luxury projects, and we’ve backed it with one of the most stringent insurances available in the market. That gives buyers peace of mind that their investment is protected for the long term.

“People are walking through and realising you simply don’t see this level of quality at these price points anymore, as it’s effectively replacement cost in 2025.

“With rates coming down and limited competition, buyers and investors are moving quickly because they know the window won’t stay open. Investors, who have recently purchased at Ophora, have reported a strong rental demand, with minimum rental yields exceeding five per cent.”

Developments like Ophora, move-in ready, competitively priced and backed by rare structural protections (LDI), may represent the last chance for buyers to secure a sub-$700,000 apartment in Sydney.

View Ophora on cpmrealty.com.au

To arrange a private viewing or request more information, contact Sam Elbanna from CPM Realty: 0411 222 260

Formula 1 may be the world’s most glamorous sport, but for Oscar Piastri, it’s also one of the most lucrative. At just 24, Australia’s highest-paid athlete is earning more than US$40 million a year.

Australia’s housing market defies forecasts as prices surge past pandemic-era benchmarks.